Tax Computation Process for Nonresident Alien

1. INTRODUCTION

This article addresses the process and statutes governing the calculation of taxable income for a nonresident alien. It also shows what elections may or may not be made at each step. For the purpose of this article, a national of the United States (meaning anyone born in the COUNTRY United States*) is considered a nonresident alien in the context of the IRC, which results in the filing of a 1040 NR form pursuant to the following:

USPI thru Changing YOUR status to DOMESTIC, FTSIG

https://ftsig.org/how-you-volunteer/uspi-thru-domestic-status/

American nationals can surrender that default status of being a “nonresident alien” ONLY by making some form of election, meaning consent. That election is usually done IMPLIEDLY rather than EXPLICITLY, so that it is invisible to those making it in most cases. Watch out!

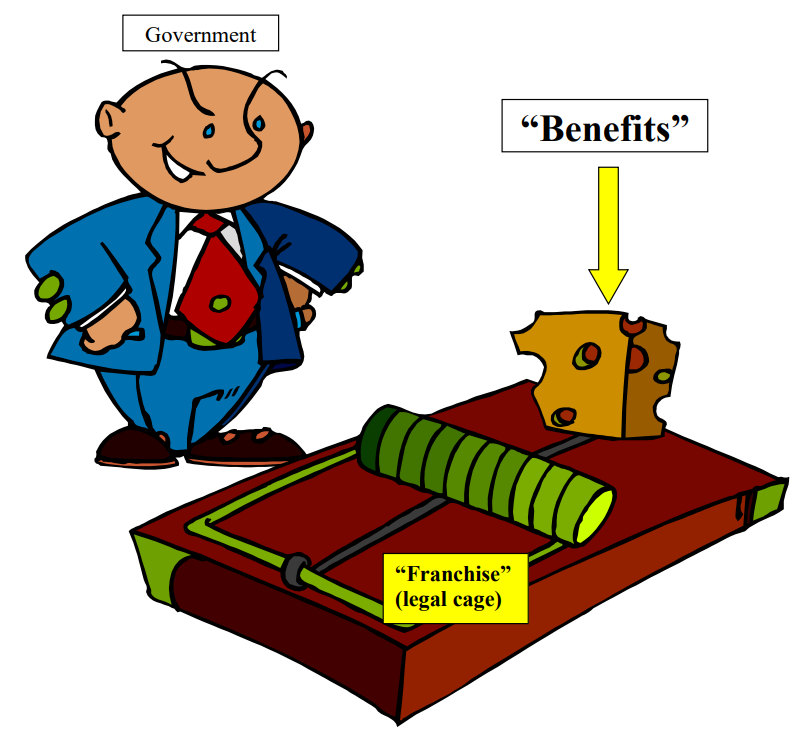

The process of LAWFULLY avoiding income taxation or government regulation in general requires that you avoid ANY and ALL PRIVILEGES. And by “PRIVILEGE” we mean United States Property Interest (USPI) government property interest. This is because a “franchise” is legally defined as “a privilege in the HANDS of a subject”. You thus BECOME a “subject” by asking for the privilege and putting it “in your hands”, meaning in your possession or control:

“Is it a franchise? A franchise is said to be a right reserved to the people by the constitution, as the elective franchise. Again, it is said to be a privilege conferred by grant from government, and vested in one or more individuals, as a public office. Corporations, or bodies politic are the most usual franchises known to our laws. In England they are very numerous, and are defined to be royal privileges in the hands of a subject. An information will lie in many cases growing out of these grants, especially where corporations are concerned, as by the statute of 9 Anne, ch. 20, and in which the public have an interest. In 1 Strange R. ( The King v. Sir William Louther,) it was held that an information of this kind did not lie in the case of private rights, where no franchise of the crown has been invaded.

If this is so–if in England a privilege existing in a subject, which the king alone could grant, constitutes it a franchise–in this country, under our institutions, a privilege or immunity of a public nature, which could not be exercised without a legislative grant, would also be a franchise.”

[People v. Ridgley, 21 Ill. 65, 1859 WL 6687, 11 Peck 65 (Ill., 1859)]

Pursuit of every type of United States Property Interest (USPI) requires an election, whether conscious or not, to pursue the property. Some of these elections are hidden so you don’t know you are making them. It’s a TRAP, folks! Watch OUT!

The process of hiding these elections is done by obfuscating IRS pubs. The result is that you CONSENT INVISIBLY. Below is a description of how to avoid ALL privileges in a tax return filing to give you an idea of what privileges are involved:

How to Reject All Privileges in a Tax Return Filing, FTSIG

https://ftsig.org/how-to-reject-all-privileges-in-a-tax-return-filing/

2. TABLE

| # | Statute | Description | Elections |

| 1 | I.R.C. §61 | Calculate “gross income” | If amount is “gross receipts”, you must be one of the following: 1. An alien not protected by the constitution because of federal preemption or 2. Someone who ELECTED “U.S. person” status while abroad under I.R.C. §911 or 3. Those who ignorantly, needlessly, and recklessly DONATED their earnings while situated stateside by filing a 1040 instead of 1040-NR and making a “U.S. person” election in the process. Otherwise, it would be an unconstitutional direct tax among those standing on land protected by the constitution. Click here for details. There is no liability statute, so everyone is a volunteer other than withholding agents on aliens in I.R.C. §1461. |

| 2 | I.R.C. §861/862 | Apportion “gross income” to sources Within and Without the “United States” | NA |

| 3 | I.R.C. §872 | Exclude sources WITHOUT the “United States” | NA |

| 4 | I.R.C. §864 I.R.C. §871(b) | Assess/Elect Effectively connected income. ONLY enter ECI on 1040NR if: 1. Students in exchange program. 26 C.F.R. §1.871-9. 2. You elect to treat real property income as effectively connected under FIRPTA under I.R.C. §871(d). 26 C.F.R. §1.871-10. 3. Exceptions cited in I.R.C. §864(c)(6)-(8). The most important of these is “deferred compensation” originally connected with a “trade or business” in I.R.C. §864(c)(7)(B). | Voluntary in MOST but not ALL cases for American Nationals. See Form #05.056, Section 12. Cases where your consent is NOT required are what we call “incidental” cases of “trade or business” that result from PRIOR elections you previously made, such as partnerships or government retirement accrued as deferred compensation while serving where the constitution does NOT apply. |

| 5 | I.R.C. §873 I.R.C. §162 | Apply deductions to ECI, but only if you HAVE MANDATORY ECI in step 4 without election. | This makes you an “individual” and “person” per I.R.C. §873. We think it’s the one in I.R.C. §7701(a)(1) and NOT the one in I.R.C. §6671(b) and I.R.C. §7343. |

| 6 | I.R.C. §871(a) | If you are an alien ONLY, fill out Schedule NEC. | If you fill this out as a “national”, you UNLAWFULLY elected privileged “alien” status. A U.S. national MAY NOT elect to be treated as a “resident alien” under I.R.C. §6013(g) and (h). Only an alien NRA may elect to be treated as a “resident alien.” See I.R.C. §7701(b)(4)(B). |

| 7 | I.R.C. §871(b) | If a “U.S. national” under 8 U.S.C. §1101(a)(22) and 22 C.F.R. §51.1 and no ECI or “alien” election, enter all zeros on 1040NR form. No liability under I.R.C. §871(a) or I.R.C. §871(b). No requirement to file Sch. NEC. YOU’RE FREE AS A BIRD! | If you don’t do this, you elected to DONATE your earnings to Uncle needlessly. |

3. NOTES

- See the following two resources for determining “gross income” and to understand the main position of this filing:

1.1. PROOF OF FACTS: Payments to me as a U.S. national are “excluded” from “Gross Income” under I.R.C. 872, FTSIG

https://ftsig.org/proof-of-facts-my-earnings-as-a-u-s-national-are-excluded-from-gross-income-under-i-r-c-872/

1.2. IRS Publication 525: Taxable and Nontaxable Income

https://www.irs.gov/publications/p525 - Table row 4 in the previous section: deferred compensation might include government retirement as described in:

Policy Document: Retirement and Pensions, Form #08.028

https://sedm.org/Forms/08-PolicyDocs/RetirementAndPensions.pdf - ECI=Effectively Connected Income. Entered on the 1040NR form pursuant to I.R.C. §864. See:

The Truth About “Effectively Connecting”, Form #05.056

https://sedm.org/Forms/05-MemLaw/EffectivelyConnected.pdf - For a series of AI questions about this subject, see:

Microsoft Copilot: Tax Computation Process for Nonresident Aliens, FTSIG

https://ftsig.org/microsoft-copilot-tax-computation-process-for-nonresident-aliens/ - Schedule NEC only applies to privileged aliens BECAUSE:

5.1. Top half of form computes income ONLY based on tax treaty benefits available ONLY to aliens and never U.S. nationals.

5.2. Bottom half of the form is only for capital gains on real estate by aliens in I.R.C. §871(a)(2).

5.3. Since tax is on GROSS receipts in I.R.C. §871(a)(1), and constitution forbids direct taxes on gross receipts for those protected by it, it can only apply to nonresidents not protected by the constitution who are therefore ABROAD or in a federal territory. See:

Microsoft Copilot: Is the income tax a DIRECT tax or an INDIRECT tax?, FTSIG

https://ftsig.org/microsoft-copilot-is-the-income-tax-a-direct-tax-or-an-indirect-tax/

5.4. 26 C.F.R. §1.871-1(a) does NOT identify “nationals” as nonresident aliens so they are excluded. But they ARE EXPRESSLY included in I.R.C. §873(a) ONLY when they take DEDUCTIONS against ECI. - There are TWO main types of elections:

6.1. “Effectively connecting” under I.R.C. §864, which is voluntary for American Nationals. I.R.C. §864(c)(8) requires that if a nonresident alien is partner in a U.S. person partnership, they must effectively connect. This also produces a “person” or “Individual” election, as pointed out in item 5 of the above table.

6.2. Alien status election as a U.S. national. This is done by filling out the Schedule NEC.

We can find NO statutory authority for such an election so it is unlawful. The IRS pubs are COMPLETELY silent on these for good reason. - There is LOTS of deception by the IRS surrounding whether and HOW a U.S. national becomes a “nonresident alien”. See:

Microsoft Copilot: IRS Deception About who are “nonresident aliens”, FTSIG

https://ftsig.org/microsoft-copilot-irs-deception-about-who-are-nonresident-aliens/ - Because of the deliberate deception described in the previous item, doubts MUST be resolved in YOUR favor and not the GOVERNMENT’S favor per the following:

PROOF OF FACTS: Ambiguous tax statutes are to be construed against the government, FTSIG

https://ftsig.org/proof-of-facts-ambiguous-tax-statutes-are-to-be-construed-against-the-government/ - For an EXAMPLE of how to apply these concepts to a tax filing, see:

1040-NR Attachment, Form #09.077

https://sedm.org/Forms/09-Procs/1040NR-Attachment.pdf - The ONLY affect the Sixteenth Amendment had on the above process is:

10.1. It removed taxes on personal property within the jurisdiction of the United States (i.e. the Congress) from the apportionment requirement for direct taxes identified in Pollock v. Farmers’ Loan & Trust Co., 158 U.S. 601, 618, 15 S.Ct. 912, 39 L.Ed. 1108 (1895).

10.2. It made the “source” irrelevant (“whatever SOURCE derived”), meaning the TYPE of PRIVATE property is irrelevant that is the subject of the ALREADY lawful INDIRECT excise taxation process. It did NOT eliminate the constitutional prohibition against DIRECT taxes outside the United States subject matter jurisdiction.

More on the above at:

Journey to Sixteenth Amendment, Fed Reserve, FTSIG

https://ftsig.org/history/journey-to-16a-fed-reserve-nnot/

4. CONCLUSIONS

The term “source” in the Sixteenth Amendment means the type of private property subject to the indirect excise taxation, according to the courts.

The world, on the other hand, wants you to falsely believe that “source” in the Sixteenth Amendment refers to a GEOGRAPHY but it DOES NOT. Most types of property, in fact, are INTANGIBLE and HAVE no real geography! Thus, they are NOT susceptible to being WITHIN or WITHOUT ANY specific geography. This includes MOST of what is listed in I.R.C. §861 and I.R.C. §862. The laws of taxation, for instance, authorize income taxation of INTANGIBLES at the DOMICILE of the owner, not the LOCATION of the property! See:

PROOF OF FACTS: Taxation of Intangibles is at the domicile of the owner by default, FTSIG

https://ftsig.org/proof-of-facts-taxation-of-intangibles-is-at-the-domicile-of-the-owner/

The covetous government, by exploiting your legal ignorance manufactured in the PUBLIC FOOL SYSTEM, wants you to falsely believe that I.R.C. §861 and I.R.C. §862 are strictly geographical, but in fact they BOTH relate to United States Property Interest (USPI) that is INVISIBLE to most people.

- WITHIN the “United States” means USPI situated in the 50 states and D.C., but regarded as within United StatesG through federal preemption (the individual component jurisdictions become irrelevant).

- WITHOUT United StatesG refers to a USPI situated anywhere in the world OUTSIDE United StatesG (I.e., in U.S. territories, possessions, and from within foreign nation-states).

It’s like one source of water—the water well. But then that source is split at the faucet between a hot source and a cold source. The source that matters is the water well, meaning domesticS USPI. But the person at the sink THINKS there’s just a hot source and a cold source. The source argument presented EVERYWHERE in the IRC and regs is either hot or cold—within or without United StatesG. The water well—is the unspoken, self-evident truth that is the overarching theme of the IRC. It’s NEVER explicitly stated—only implicitly understood.

When the Sixteenth Amendment says “from whatever source derived”, we know there is only one source—the domesticS USPI source. But that USPI can come from two geographical sources—within or without United StatesG. DomesticS USPI is the ORIGIN of their authority to tax. In other words, if they want to take your property or force you to pay something, they have to provide CONSIDERATION required by the Fifth Amendment takings clause:

“It is only where some right or privilege [which are GOVERNMENT PROPERTY] is conferred by the government or municipality upon the owner, which he can use in connection with his property, or by means of which the use of his property is rendered more valuable to him, or he thereby enjoys an advantage over others, that the compensation to be received by him becomes a legitimate matter of regulation [AND by implication taxation]. Submission to the regulation of compensation in such cases is an implied condition of the grant, and the State, in exercising its power of prescribing the compensation, only determines the conditions upon which its concession shall be enjoyed. When the privilege ends, the power of regulation [and taxation] ceases.”

[Munn v. Illinois, 94 U.S. 113, 146-147 (1877);

SOURCE: https://scholar.google.com/scholar_case?case=6419197193322400931 ]

“A person is ordinarily not required to pay for benefits which were thrust upon him with no opportunity to refuse them. The fact that he is enriched is not enough, if he cannot avoid the enrichment.” Wade, Restitution for Benefits Conferred Without Request, 19 Vand. L. Rev. at 1198 (1966).

[Siskron v. Temel-Peck Enterprises, 26 N.C.App. 387, 390 (N.C. Ct. App. 1975)]

“Quilibet potest renunciare juri pro se inducto. Any one may renounce a law [including a CIVIL FRANCHISE statute] introduced for his own benefit.”

[Bouvier’s Maxims of Law, 1856]

“As was said in Wisconsin v. J. C. Penney Co., 311 U.S. 435, 444 (1940), “[t]he simple but controlling question is whether the state has given anything for which it can ask return.”

[Colonial Pipeline Co v Traigle, 421 U.S. 100, 109 (1975); SOURCE: https://scholar.google.com/scholar_case?case=16559630216409245512]

If they didn’t do it this way, we would end up LITERALLY with a MAFIA government who could charge you anything they want no matter how much they provide in return. We put it this way in our 1040NR attachment:

An offer of privileges I am legally unable to refuse or a prior acceptance I can’t revoke is little more than a criminal mafia enterprise and slavery disguised as government benevolence. Alex De Tocqueville called this “soft tyranny”. Remember the Godfather movie?: “An offer you can’t refuse.”

If no USPI is involved, you can’t earn income from EITHER within or without United StatesG per I.R.C. §861 and I.R.C. §862 respectively.

By doing this, IRS MISLEADs the reader to believe that the tax is simply on “income” (GROSS receipts and NOT profit) wherever it comes from GEOGRAPHICALLY. That’s why they published I.R.C. §861 and I.R.C. §862–to obfuscate the TRUE SOURCE of their authority—USPI. USPI is the one and only original source of jurisdiction—the domesticS source. And they have jurisdiction over that property wherever it is physically located under Article 4, Section 3, Clause 2 of the Constitution as a type of SUBJECT MATTER jurisdiction rather than EXCLUSIVE jurisdiction. The tax is NON-GEOGRAPHICAL, so long as USPI is involved:

“It was held that the grant of this power was a general one without limitation as to place, and consequently extended to all places over which the government [USPI] extends; and that it extended to the District of Columbia as a constituent part of the United States.”

[Downes v. Bidwell, 182 U.S. 244, 260 (1901);

SOURCE: https://scholar.google.com/scholar_case?case=9926302819023946834]

Government, after all, is JUST a collection of PUBLIC/COMMUNITY PROPERTY. A trust was created to MANAGE that property called the Constitution. The “corpus” of that trust is the community property of the states. That trust creates a CORPORATION called “government”, which the courts call the BODY CORPORATE. All property is held or managed by that corporation on behalf of the Constitutional trust. Offices WITHIN that corporation are a legislative creation of that corporation and thus PROPERTY of that corporation. Those offices include CIVIL statutory “taxpayer”, “U.S. person”, “person”, “individual”, “citizen of the United StatesG“, etc.

Can you imagine if they didn’t obfuscate domesticS with a two-layer geographical category? Everyone would simply avoid the government nexus if they knew. The geographical categories lead folks to believe resistance is futile.