Civil Status (Association + Domicile)

1. Introduction

Association=Political citizen* under Fourteenth Amendment or 8 U.S.C. §1401-1408.

Domicile = voluntary local MUNICIPAL allegiance in a specific county or political subdivision.

Called a CIVIL/DOMICILED Citizen**+D on this site.

The law of England, and of almost all civilized countries, ascribes to each individual at his birth two distinct legal states or conditions,-one by virtue of which he becomes the subject of some particular country, binding him by the tie of natural allegiance, and which may be called his political status; another by virtue of which he has ascribed to him the character of a citizen of some particular country, and as such is possessed of certain municipal rights, and subject to certain obligations, which latter character is the civil status or condition of the individual, and may be quite different from his political status.

[United States v. Wong Kim Ark, 169 U.S. 649, 656 (1898)]

“He evidently used the word “citizen,” not as equivalent to “subject,” but rather to “inhabitant;””

[United States v. Wong Kim Ark, 169 U.S. 649, 657 (1898)]

“[C]ivil status is universally governed by the single principle of domicil, [or] domicilium, the criterion established by international law for the purpose of determining civil status, and the basis on which “the personal rights of the party . . . must depend;”

[United States v. Wong Kim Ark, 169 U.S. 649, 656-57 (1898)]

“Domicile is the place where one has his true, fixed, permanent home and principal establishment and to which, whenever he is absent, he has the intention of returning.”

2. Domicile

Domicile is a judicial invention not found in the constitution. We prove that below:

Copilot: Origin of domicile and authority of courts to use it, FTSIG-judges COMPELLING domicile

https://ftsig.org/copilot-origin-of-domicile-and-authority-of-courts-to-use-it/

Domicile is abused by corrupt judges to recruit you into economic and legal servitude to the OPTIONAL civil statutory law. Here is an example of that:

The obligation of one domiciled within a state to pay taxes there, arises from unilateral action of the state government in the exercise of the most plenary of sovereign powers, that to raise revenue to defray the expenses of government and to distribute its burdens equably among those who enjoy its benefits. Hence, domicile in itself establishes a basis for taxation. Enjoyment of the privileges of residence within the state, and the attendant right to invoke the protection of its laws, are inseparable from the responsibility for sharing the costs of government. See Fidelity & Columbia Trust Co. v. Louisville, 245 U.S. 54, 58; Maguire v. Trefry, 253 U.S. 12, 14, 17; Kirtland v. Hotchkiss, 100 U.S. 491, 498; Shaffer v. Carter, 252 U.S. 37, 50. The Federal Constitution imposes on the states no particular modes of taxation, and apart from the specific grant to the federal government of the exclusive 280*280 power to levy certain limited classes of taxes and to regulate interstate and foreign commerce, it leaves the states unrestricted in their power to tax those domiciled within them, so long as the tax imposed is upon property within the state or on privileges enjoyed there, and is not so palpably arbitrary or unreasonable as to infringe the Fourteenth Amendment. Kirtland v. Hotchkiss, supra.

Taxation at the place of domicile of tangibles located elsewhere has been thought to be beyond the jurisdiction of the state, Union Refrigerator Transit Co. v. Kentucky, 199 U.S. 194; Frick v. Pennsylvania, 268 U.S. 473, 488-489; but considerations applicable to ownership of physical objects located outside the taxing jurisdiction, which have led to that conclusion, are obviously inapplicable to the taxation of intangibles at the place of domicile or of privileges which may be enjoyed there. See Foreign Held Bond Case, 15 Wall. 300, 319; Frick v. Pennsylvania, supra, p. 494. And the taxation of both by the state of the domicile has been uniformly upheld. Kirtland v. Hotchkiss, supra; Fidelity & Columbia Trust Co. v. Louisville, supra; Blodgett v. Silberman, 277 U.S. 1; Maguire v. Trefry, supra; compare Farmers Loan & Trust Co. v. Minnesota, 280 U.S. 204; First National Bank v. Maine, 284 U.S. 312.

[Lawrence v. State Tax Commission, 286 U.S. 276 (1932); SOURCE: https://scholar.google.com/scholar_case?case=10241277000101996613]

The civil statutory law, in turn, is a Private Membership Association that is optional and proprietary. You don’t have to join it an no one can force you to. We prove this in:

Why Domicile and Becoming a “Taxpayer” Require Your Consent, Form #05.002

https://sedm.org/Forms/05-MemLaw/Domicile.pdf

Notice in the above case the phrase “among those who enjoy its benefits.” You have a common law right to REFUSE all benefits, and thus RETAIN your private capacity and ONLY common law and criminal law protections.

“A person is ordinarily not required to pay for benefits which were thrust upon him with no opportunity to refuse them. The fact that he is enriched is not enough, if he cannot avoid the enrichment.” Wade, Restitution for Benefits Conferred Without Request, 19 Vand. L. Rev. at 1198 (1966). [Siskron v. Temel-Peck Enterprises, 26 N.C.App. 387, 390 (N.C. Ct. App. 1975)]

“Quilibet potest renunciare juri pro se inducto. Any one may renounce a law [including a CIVIL FRANCHISE statute] introduced for his own benefit.”

[Bouvier’s Maxims of Law, 1856;

SOURCE: https://famguardian.org/Publications/BouvierMaximsOfLaw/BouviersMaxims.htm]

“The power of taxation, indispensable to the existence of every civilized government, is exercised upon the assumption of an equivalent rendered to the taxpayer in the protection of his person and property, in adding to the value of such property, or in the creation and maintenance of public conveniences in which he shares, such, for instance, as roads, bridges, sidewalks, pavements, and schools for the education of his children. If the taxing power be in no position to render these services, or otherwise to benefit the person or property taxed, and such property be wholly within the taxing power of another State, to which it may be said to owe an allegiance and to which it looks for protection, the taxation of such property within the domicil of the owner partakes rather of the nature of an extortion than a tax, and has been repeatedly held by this court to be beyond the power of the legislature and a taking of property without due process of law. Railroad Company v. Jackson, 7 Wall. 262; State Tax on Foreign-held Bonds, 15 Wall. 300; Tappan v. Merchants’ National Bank, 19 Wall. 490, 499; Delaware &c. R.R. Co. v. Pennsylvania, 198 U.S. 341, 358. In Chicago &c. R.R. Co. v. Chicago, 166 U.S. 226, it was held, after full consideration, that the taking of private property 203*203 without compensation was a denial of due process within the Fourteenth Amendment. See also Davidson v. New Orleans, 96 U.S. 97, 102; Missouri Pacific Railway v. Nebraska, 164 U.S. 403, 417; Mount Hope Cemetery v. Boston, 158 Massachusetts, 509, 519.”

[Union Refrigerator Transit Company v. Kentucky, 199 U.S. 194, 202-203 (1905);

SOURCE: https://scholar.google.com/scholar_case?case=14163786757633929654]

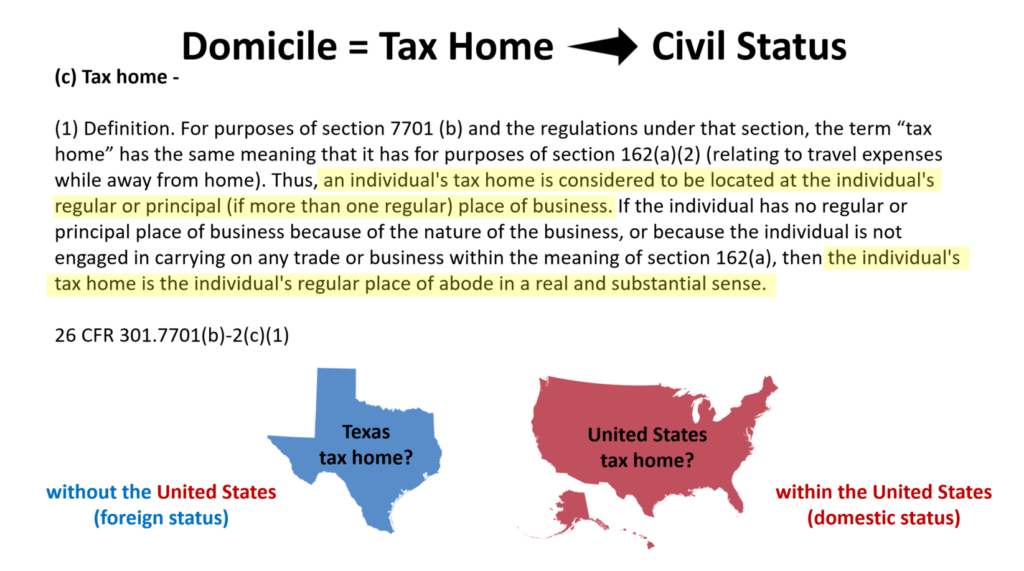

3. Tax Home

4. Foreign country

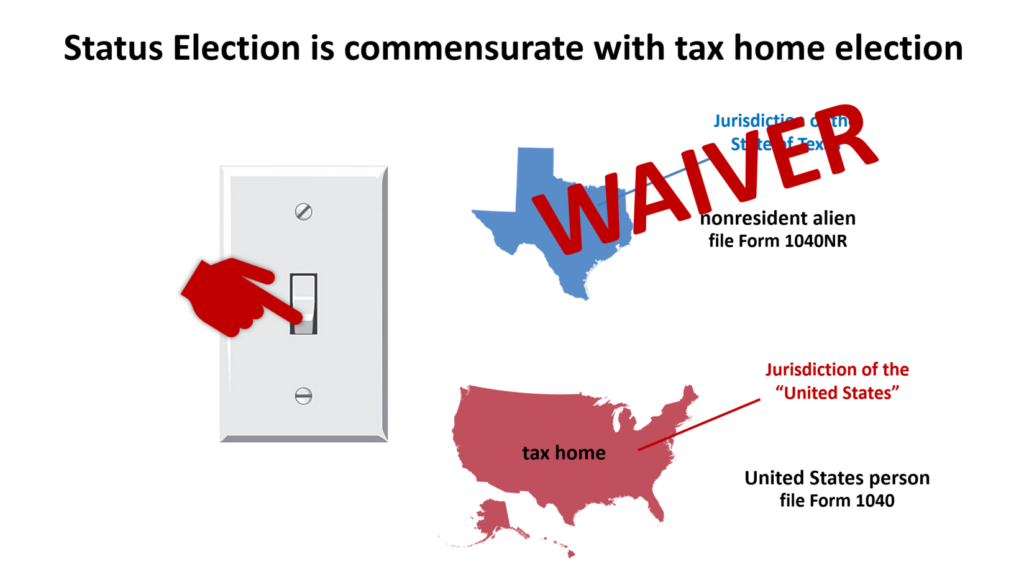

The 50 states are CIVILLY and LEGISLATIVELY foreign with respect to the national government, PROVIDED we properly aver our status as a “nonresident alien” and file the CORRECT 1040NR tax return as an American national born within a constitutional state and residing there:

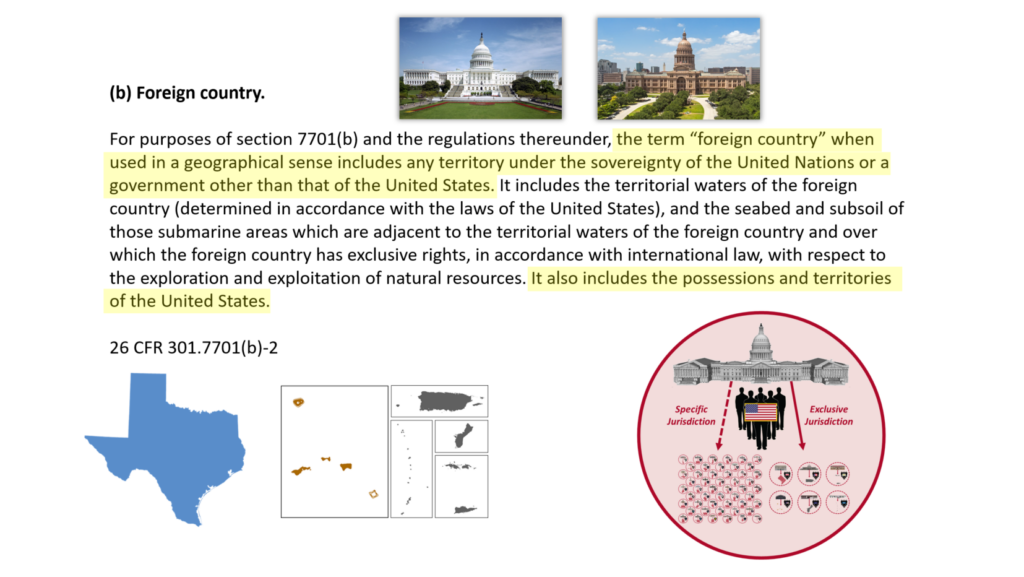

(b) Foreign country.

For purposes of section 7701(b) and the regulations thereunder, the term “foreign country” when used in a geographical sense includes any territory under the sovereignty of the United Nations or a government other than that of the United States. It includes the territorial waters of the foreign country (determined in accordance with the laws of the United States), and the seabed and subsoil of those submarine areas which are adjacent to the territorial waters of the foreign country and over which the foreign country has exclusive rights, in accordance with international law, with respect to the exploration and exploitation of natural resources. It also includes the possessions and territories of the United States.

[26 C.F.R. §301.7701(b)-2]

Note the phrase above “when used in a geographical sense includes any territory under the sovereignty of the United Nations or a government other than that of the United States.” States of the Union fit in this category.

Foreign Laws:“The laws of a foreign country or sister state. In conflicts of law, the legal principles of jurisprudence which are part of the law of a sister state or nation. Foreign laws are additions to our own laws, and in that respect are called ‘jus receptum’.”

[Black’s Law Dictionary, 6th Edition, p. 647]

Foreign Laws:“The laws of a foreign country or sister state. In conflicts of law, the legal principles of jurisprudence which are part of the law of a sister state or nation. Foreign laws are additions to our own laws, and in that respect are called ‘jus receptum’.”

[Black’s Law Dictionary, 6th Edition, p. 647]

foreign: not being within the jurisdiction of a political unit (as a state)

esp

: being from or in a state other than the one in which a matter is being consideredExample: a foreign company doing business in South Carolina

Example: a foreign executor submitting to the jurisdiction of this court

Example: a foreign judgment

(compare domestic)

[Merriam-Webster’s Dictionary of Law ©1996]

5. Why States of the Union are included in the definition of “foreign country” for nonresident alien U.S. nationals

The use of the word “includes” in the definition of “foreign country” in 26 C.F.R. §301.7701(b)-2(b) definition of “foreign country” implies a CLASS of items in the definition per 26 U.S.C. §7701(c) which doesn’t list all the members of the parent class. The reason states of the Union they are not explicitly mentioned is as members of the class identified as “government other than that of the United States.” is fear of exposing the voluntary nature of the income tax in I.R.C. Subtitle A and entirely collapsing income tax enforcement in states of the Union, even though the Unconstitutional Conditions Doctrine mandates this collapse:

Copilot: Unconstitutional Conditions Doctrine applied to Federal and State Income Taxation, FTSIG

https://ftsig.org/copilot-unconstitutional-conditions-doctrine-applied-to-federal-and-state-income-taxation/

There is no liability statute that makes I.R.C. Subtitle A income tax mandatory for anyone other than withholding agents on aliens in 26 U.S.C. §1461. Therefore, everyone other than aliens are volunteers. They had to do it this way or else slavery and involuntary servitude, human trafficking, and peonage would be the inevitable result as explained below:

Proof that Involuntary Income Taxes on Your Labor are Slavery, Form #05.055

https://sedm.org/Forms/05-MemLaw/ProofIncomeTaxLaborSlavery.pdf

There are several paths to volunteer, and the civil public capacity you choose when filing (“U.S. person” or “Nonresident alien”) determine the obligations resulting from volunteering. Once you volunteer, you adopt a public capacityPUB and become surety for it. That voluntary surety transitions you from “foreign” and PRIVATE to “domestic” and PUBLIC.

Dangerous Promises

6 My son, if you become surety for your friend,

If you have shaken hands in pledge for a stranger [or a LEGISLATIVELY FOREIGN government],

2 You are snared by the words of your mouth;

You are taken by the words of your mouth.

3 So do this, my son, and deliver yourself;

For you have come into the hand of your friend:

Go and humble yourself;

Plead with your friend.

4 Give no sleep to your eyes,

Nor slumber to your eyelids.

5 Deliver yourself like a gazelle from the hand of the hunter,

And like a bird from the hand of the fowler.[Prov. 6:1-5, Bible, NKJV]

WATCH OUT!

6. Further Reading on this subject

- “Sovereign”=”Foreign”-Family Guardian Fellowship

https://famguardian.org/Subjects/Freedom/Sovereignty/Sovereign=Foreign.htm - Why Domicile and Becoming a “Taxpayer” Require Your Consent, Form #05.002

https://sedm.org/Forms/05-MemLaw/Domicile.pdf - Why Domicile and Becoming a “Taxpayer” Require Your Consent, Family Guardian Fellowship

https://famguardian.org/Subjects/Taxes/Remedies/DomicileBasisForTaxation.htm - Why Statutory Civil Law is Law for Government and not Private Persons, Form #05.037

https://sedm.org/Forms/05-MemLaw/StatLawGovt.pdf - Copilot: Origin of domicile and authority of courts to use it, FTSIG-judges COMPELLING domicile

https://ftsig.org/copilot-origin-of-domicile-and-authority-of-courts-to-use-it/