Constitutional taxation provisions 1:8:1, 1:9:4, 1:2:3

1. Introduction

[Adapted from: Direct and Indirect Taxes; National Constitution Center; https://constitutioncenter.org/the-constitution/articles/article-i/clauses/757]

The Constitution permits three classes of taxation:

- Direct taxes, which must be apportioned among the states in proportion to their populations;

- “Indirect taxes,” specifically duties, imposts, and excises, which must be uniform throughout the country; and

- Income taxes on humans (as opposed to businesses or other entities), which may apply to income “derived from a source”.

Taxing jurisdiction originates in the U.S. Constitution as follows:

Article 1. The Legislative Branch

Section 8. Powers of Congress

Clause 1. Power to Tax and Spend [Indirect/Excise taxes]

The Congress shall have Power to lay and collect Taxes, Duties, Imposts and Excises, to pay the Debts and provide for the common Defence and general Welfare of the United States; but all Duties, Imposts and Excises shall be uniform throughout the United States.

Article 1. The Legislative Branch

Section 9. Powers Denied to Congress

Clause 4. Taxes [Direct Taxes]

No Capitation, or other direct, Tax shall be laid, unless in Proportion to the Census or Enumeration herein before directed to be taken.

Article 1. The Legislative Branch

Section 2. The House of Representatives

Clause 3. Apportionment of Seats In the House [Method of apportioning Direct Taxes]

[Representatives and direct Taxes shall be apportioned among the several States which may be included within this Union, according to their respective Numbers, which shall be determined by adding to the whole Number of free Persons, including those bound to Service for a Term of Years, and excluding Indians not taxed, three fifths of all other Persons]. 343 The actual Enumeration shall be made within three Years after the first Meeting of the Congress of the United States, and within every subsequent Term of ten Years, in such Manner as they shall by Law direct. The Number of Representatives shall not exceed one for every thirty Thousand, but each State shall have at Least one Representative; and until such enumeration shall be made, the State of New Hampshire shall be entitled to chuse three, Massachusetts eight, Rhode Island and Providence Plantations one, Connecticut, five, New York six, New Jersey four, Pennsylvania eight, Delaware one, Maryland six, Virginia ten, North Carolina five, South Carolina five, and Georgia three.

What Congress very deliberately DID NOT inform you of in the above are the main limitations upon income taxes:

- The United StatesP consists mainly of American nationals (“nationals of the United States” under 8 U.S.C. §1101(a)(22) and 22 C.F.R. §51.1) standing on land protected by the Constitution geographically INTERNAL to the United StatesP.

- Geographically INTERNAL taxes under Article 1, Section 8, Clause 1 are primarily upon:

2.1. Aliens engaging in FOREIGN COMMERCE with the United StatesP. This is called a “SOVEREIGN POWER” and it does not require consent of the aliens subject to tax, because they are not standing on land protected by the constitution. Article 1, Section 8, Clause 3.

2.2. “U.S. person” FICTIONS (corporations) voluntarily engaged in on excise taxable privileges. Article 1, Section 8, Clause 1. This includes taxation of FEDERAL corporate privileges in the original constitution. Flint v. Stone Tracy, 220 U.S. 107 (1911) is an example of this. - Excise taxable privileges in 2.2 above were subsequently expanded to include Individuals (humans) and businesses who make a “domestic election” with the Social Security Act in 1935 in the case of territorial parties but not people in states of the Union (Form #06.001). Judicial FIAT in violation of the separation of powers ADDED human beings in states of the Union under the presumption of comity/consent was the authority for this expansion.

- Limitations upon Direct Taxes in Article 1, Section 9, Clause 4 and Article 1, Section 2, Clause 3 apply to American nationals standing on land protected by the Constitution.

4.1. They DO NOT apply to aliens abroad not standing on said land.

4.2. The MAIN characteristic of such a tax is that it DOES NOT involve a privilege AND constitutes a tax on “gross receipts”.

4.3. It is a tax upon PRIVATE propertyPRI, not GOVERNMENT/PUBLIC propertyPUB such as privileged franchise offices the government legislatively creates. - If they tax American nationals (“nationals of the United States” under 8 U.S.C. §1101(a)(22) and 22 C.F.R. §51.1) standing on land protected by the Constitution geographically INTERNAL to the United StatesP, the tax must respect the laws of property established by the Constitution and must be connected to a voluntary, excise taxable, privileged activity that is AVOIDABLE.

Property View of Income Taxation Course, Form #12.046

https://sedm.org/LibertyU/PropertyViewOfIncomeTax.pdf - In compliance with the above, we invented the symbology United StatesG, which is synonymous with:

6.1. The geographical area covered by the United States of America mentioned in the Constitution consisting of the area subject to the exclusive jurisdiction of the states mentioned in the Constitution . . .AND

6.2. A consensual, voluntary excise taxable activity conducted on said physical soil.

The above symbology is described in the Introduction->Writing Conventions on this Website Menu at:

https://ftsig.org/introduction/writing-conventions-on-this-website/ - A tax which respects the laws of property:

7.1. Is called a PROPRIETARY POWER. That power is not a SOVEREIGNPUB POWER. It is, however, sometimes confused with a SOVEREIGNPRI POWER through judicial equivocation to disguise the origin of the INTERNAL taxing power of American nationals and challenges to it.

7.2. MUST involve GOVERNMENT/PUBLIC propertyPUB called a “privilege” so that government has the power to tax and regulate the USE of said propertyPUB and privileges under Article 4, Section 3, Clause 2.

For a description of the above concepts, see:

HOW TO: How to distinguish “sovereign power” from “proprietary power” in the context of taxation, FTSIG

https://ftsig.org/how-to-how-to-distinguish-sovereign-power-from-proprietary-power-in-the-context-of-taxation/

You might ask WHY did they hide the above facts or make them VAGUE? The answer is that it would make the tax too easy to avoid if they were revealed unambiguously. They had to leave enough uncertainty baked into the constitution to:

- Create the appearance of judicial discretion.

- Offer an avenue for equivocation for judges to expand their jurisdiction that Thomas Jefferson warned they would do. See:

Writing Conventions on this Website, Section 11, FTSIG

https://ftsig.org/introduction/writing-conventions-on-this-website/#11._Mapping - Create the appearance that the tax is INVOLUNTARY and that everyone has to pay it.

- Make the income tax more difficult to avoid by hiding the PRIVILEGE subject to the tax.

- Obscure the requirement for consent mentioned in the Declaration of Independence that MUST be behind EVERY lawful de jure CIVIL activity of government, INCLUDING taxation.

It is a well-known fact that the first important income tax case heard by the U.S. Supreme Court, Hylton v. United States, 3 U.S. 171 (1798) was fabricated by people inside the government to implement precisely the above goals.

The above malicious tactics are what we call “sophistry”. For a list of the main methods of sophistry that create the appearance see:

HOW TO: Catalog of Deception Techniques, Third Rail Avoidance Tactics, and Defenses, FTSIG

https://ftsig.org/how-to-catalog-of-deception-techniques-third-rail-avoidance-tactics-and-defenses/

2. A Brief History of U.S. Tax Law

Much discussion preceding the Constitution, divided taxes into the direct and indirect categories; however and the Constitution adopted that precise distinction by using the word “direct” in Article 1, Section 9, Clause 4 above and the word “excise” to refer to indirect taxes in Article 1, Section 8, Clause 1 above. See, e.g., The Federalist No. 36 (Alexander Hamilton). Supreme Court decisions such as the License Tax Cases (1867) have also routinely used the direct/indirect dichotomy. As early as 1796, in Hylton v. United States, the Supreme Court wrestled with the direct/indirect dichotomy. As the Court explained in that case, direct taxes must be apportioned while indirect taxes—duties, imposts, and excises—must be uniform; and any other tax (if possible) must be uniform. The Court held a tax on “carriages” to be indirect because it applied to the use of the carriage rather than to the propertyPRI itself, an arguably nuanced distinction.

In 1895, the Supreme Court held a general income tax unconstitutional as an unapportioned direct tax, distinguishing it from a tax on business or employment income, which the Court described as a permissible excise (an indirect tax). Pollock v. Farmers’ Loan & Trust Co. (1895). In contrast, the Court held, in 1911, that a tax on corporate income was constitutional as a uniform excise—a type of indirect tax. Flint v. Stone Tracy Co. (1911). The Court reasoned that the original income tax applied directly to humans, while the corporate income tax applied through the corporate entity: humans might suffer the tax through higher prices or lower profits, but they would do so indirectly. In 1913, the Sixteenth Amendment authorized an unapportioned tax on income “derived from a source.” By “derived” is meant that the profit can originate in propertyPRI, but that the gain in the propertyPRI is not a tax on the property itself. The country adopted the Amendment to reverse the 1895 Pollock decision. Many later decisions have wrestled with the “derived” requirement. The best description requires income to constitute “an accession to wealth, clearly realized, over which the taxpayer has complete dominion.” Commissioner v. Glenshaw Glass (1955).

Although some writers describe the direct/indirect and apportionment/uniformity requirements as antiquated, the dichotomies have at least some modern significance. To grasp that significance, one needs to understand the underlying terms.

3. What is a Direct Tax?

The term “direct tax” appears in the Constitution. Therefore, it is a constitutional term, not an economic term and this means that Congress has no power to define it. It must be interpreted but not defined by the Courts because the Federal Government’s taxing authority is affected by its meaning. Courts can’t define it either because the power to define is a legislative function that courts may not engage in without violating the separation of powers. Senator Cummins explains a similar scenario with the meaning of “commerce,” in the Constitution:

In 1789, I believe, the people of this country gave Congress the power to regulate commerce among the States. It is not within the power of Congress to say what commerce is. “Commerce” may mean a very different thing now as compared with what it meant in 1789. It has broadened with the times; the instrumentalities have changed with the course of years; but Congress cannot make a thing commerce. The court must declare whether a particular regulation is a regulation of commerce and in so declaring it defines for the time being what commerce is.

[1913 Congressional Record, Vol L, Part 4, pg. 3844]

“Commerce” appears in the Constitution and so Congress cannot define it. “Direct tax” appears in the Constitution and so Congress cannot define it. Additionally, after the Sixteenth Amendment, “income” also appears in the Constitution and so Congress cannot define that either. Congress cannot make a thing commerce. Congress cannot make a thing a direct tax and Congress cannot make a thing income.

David A. Wells, who helped President Lincoln establish a system of internal revenue during the Civil War, wrote an extensive multi-part treatise on taxation in which he describes the Supreme Court’s need to define “direct tax” legally. He said that the Court:

has felt compelled by the language of the Federal Constitution to assign to the term “direct,” as applicable to taxation, a “legal” rather than economic definition

[Principles of Taxation, Popular Science Monthly. June 1897]

Here again we are reminded that when discussing constitutional taxation, we are dealing with terms like direct tax, income and principal that have “legal” meanings rather economic meanings. In 1880, the Supreme Court provided its legal definition:

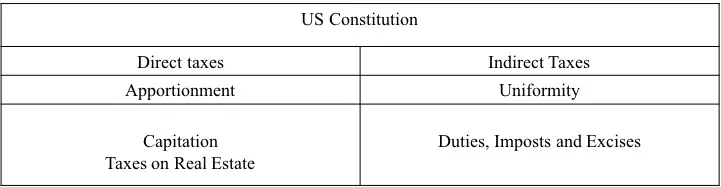

Our conclusions are, that direct taxes, within the meaning of the Constitution, are only capitation taxes, as expressed in that instrument, and taxes on real estate

[Springer v. United States, 102 U.S. 586, 602 (1880);

SOURCE: https://scholar.google.com/scholar_case?case=3081110958181951212]

In 1880, the constitutional meaning of “direct tax” was limited to capitations and taxes on real estate and the tax structure looked like this:

4. What is an Excise Tax?

A direct tax is a tax on OWNERSHIP of PRIVATE propertyPRI, but an excise is a tax on an activity, an event, or a privilege that involves the USE of PUBLIC propertyPUB or privileges. The Supreme Court describes an excise as a tax:

Excises are “taxes laid upon the manufacture, sale or consumption of commodities within the country, upon licenses to pursue certain occupations, and upon corporate privileges.” Cooley, Const. Lim., 7th ed., 680.

[Flint v. Stone Tracey Co., 220 US 107, 151 (1911);

SOURCE: https://scholar.google.com/scholar_case?case=17853944152368373401]

Additionally, the Court describes an excise as:

A tax laid upon the happening of an event, as distinguished from its tangible fruits, is an indirect tax which Congress, in respect of some events not necessary now to be described more definitely, undoubtedly may impose.

[Tyler v. United States, 281 U.S. 497 (1930);

SOURCE: https://scholar.google.com/scholar_case?case=5652898273033007430]

Congress has always had the authority to institute indirect excise taxes on specific USES of propertyPUB but not on the OWNERSHIP of the PRIVATE propertyPRI itself. This was clarified in the following case:

“While taxes levied upon or collected from persons because of their general ownership of property may be taken to be direct, Pollock v. Farmers’ Loan & Trust Co., 157 U.S. 429, 15 S. Ct. 673; Id., 158 U.S. 601, 15 S. Ct. 912, this court has consistently held, almost from the foundation of the government, that a tax imposed upon a particular use of property or the exercise of a single power over property incidental to ownership, is an excise which need not be apportioned, and it is enough for present purposes that this tax is of the latter class. Hylton v. United States, supra; cf. Veazie Bank v. Fenno, 8 Wall. 533; Thomas v. United States, 192 U.S. 363, 370, 24 S. Ct. 305; Billings v. United States, 232 U.S. 261, 34 S. Ct. 421; Nicol v. Ames, supra; Patton v. Brady, 184 U.S. 608, 22 S. Ct. 493; McCray v. United States, 195 U.S. 27, 24 S. Ct. 769, 1 Ann. Cas. 561; Scholey v. Rew, 23 Wall. 331; Knowlton v. Moore, supra. See, also, Flint v. Stone Tracy Co., 220 U.S. 107, 31 S. Ct. 342, Ann. Cas. 1912B, 1312; Spreckels Sugar Refining Co. v. McClain, 192 U.S. 397, 24 S. Ct. 376; Stratton’s Independence v. Howbert, 231 U.S. 399, 34 S. Ct. 136; Doyle v. Mitchell Brothers Co ., 247 U.S. 179, 183, 38 S. Ct. 467; Stanton v. Baltic Mining Co.,240 U.S. 103, 114, 36 S. Ct. 278.

It is a tax laid only upon the exercise of a single one of those powers incident to ownership, the power to give the property owned to another. Under this statute all the other rights and powers which collectively constitute [280 U.S. 124, 137] property or ownership may be fully enjoyed free of the tax. So far as the constitutional power to tax is concerned, it would be difficult to state any intelligible distinction, founded either in reason or upon practical considerations of weight, between a tax upon the exercise of the power to give property inter vivos and the disposition of it by legacy, upheld in Knowlton v. Moore, supra, the succession tax in Scholey v. Rew, supra, the tax upon the manufacture and sale of colored oleomargarine in McCray v. United States, supra, the tax upon sales of grain upon an exchange in Nicol v. Ames, supra, the tax upon sales of shares of stock in Thomas v. United States, supra, the tax upon the use of foreign built yachts in Billings v. United States, supra, the tax upon the use of carriages in Hylton v. United States, supra; compare Veazie Bank v. Fenno, supra, 545 of 8 Wall.; Thomas v. United States, supra, 370 of 192 U. S ., 24 S. Ct. 305.

It is true that in each of these cases the tax was imposed upon the exercise of one of the numerous rights of property, but each is clearly distinguishable from a tax which falls upon the owner merely because he is owner, regardless of the use of disposition made of his property. See Billings v. United States, supra; cf. Pierce v. United States, 232 U.S. 290, 34 S. Ct. 427. The persistence of this distinction and the justification for it rest upon the historic fact that taxes of this type were not understood to be direct taxes when the Constitution was adopted and, as well, upon the reluctance of this court to enlarge by construction, limitations upon the sovereign power of taxation by article 1, 8, so vital to the maintenance of the national government. Nicol v. Ames, supra, 514, 515 of 173 U. S., 19, S. Ct. 522.”

Specific USES of property subject to excise taxation include:

1. The Power to Give Property:

This refers to the act of transferring ownership of property to another person, such as through gifts (inter vivos) or inheritance.

2. The Power to Use Property:

Examples include the use of carriages (as in Hylton v. United States) and foreign-built yachts (as in Billings v. United States).

3. The Power to Manufacture and Sell Products from Property:

For instance, the manufacture and sale of oleomargarine (McCray v. United States).

4. The Power to Sell Property:

This could include transactions like the sale of grain on an exchange (Nicol v. Ames) or sales of shares of stock (Thomas v. United States).

5. The Power to Dispose of Property by Legacy:

This relates to bequeathing property in a will (Knowlton v. Moore, Scholey v. Rew).

6. The Power to Hold and Use Property Without Taxation:

The court contrasts this with taxes levied merely on general ownership, which are considered direct taxes.

All excise taxes authorized by the constitution are indirect and thus AVOIDABLE.

“Excises are taxes laid upon the manufacture, sale or consumption of commodities within the country, upon licenses to pursue certain occupations and upon corporate privileges…the requirement to pay such taxes involves the exercise of [220 U.S. 107, 152] privileges, and the element of absolute and unavoidable demand is lacking…

…It is therefore well settled by the decisions of this court that when the sovereign authority has exercised the right to tax a legitimate subject of taxation as an exercise of a franchise or privilege, it is no objection that the measure of taxation is found in the income produced in part from property which of itself considered is nontaxable…

Conceding the power of Congress to tax the business activities of private corporations.. the tax must be measured by some standard…”

If the income tax is an excise, then the subject of the tax must be an event involving the USE of PUBLIC propertyPUB in some form in connection with the transaction, such as:

- A legislatively created civil status (CIVIL IDENTITY) that is propertyPUB of its creator, the government. This includes “U.S. person” (acquired by filing a 1040), “employee” (acquired by filling out a W-4), “person” (acquired by an effectively connected election in 26 U.S.C. §864(b)), “taxpayer”, etc.

- A franchise mark, such as a Social Security Number or Taxpayer Identification Number. See:

About SSNs and TINs on Government Forms and Correspondence, Form #05.012

https://sedm.org/Forms/05-MemLaw/AboutSSNsAndTINs.pdf - Deductions under 26 U.S.C. §162 that produce a net DECREASE in amount of tax owed. Note that deductions attached to earnings that are not taxable but were DONATED to the “trade or business” franchise by merely writing them on the tax return are not REAL decreases in liability.

- Any kind of subsidy or benefit that remains public propertyPUB of the government unless and until the tax is paid, making the remainder into PRIVATE propertyPRI.

- Government identification cards, which say on them that they are propertyPUB of the government which must be returned upon request. Look at your passport, military ID, or driver license if you don’t believe us.

All of the above things together constitute “consideration”. All of the above things are “created or organized” by Congress and make all those who use them “domestic” and WITHIN the U.S. Inc federal corporation. Congress MUST provide “consideration” or “benefit” to the property protected in order to lawfully procure the RIGHT to tax or regulate, in fact.

Subject to these individual exceptions, the rule is that in classifying property for taxation some benefit to the property taxed is a controlling consideration, and a plain abuse of this power will sometimes justify a judicial interference. Norwood v. Baker, 172 U.S. 269. It is often said protection and payment of taxes are correlative obligations.

[Union Refrigerator Transit Co. v. Kentucky, 199 U.S. 194, 204 (1905); SOURCE: https://scholar.google.com/scholar_case?case=14163786757633929654]

It is only where some right or privilege is conferred by the government or municipality upon the owner, which he can use in connection with his property, or by means of which the use of his property is rendered more valuable to him, or he thereby enjoys an advantage over others, that the compensation to be received by him becomes a legitimate matter of regulation [or, by implication, taxation]. Submission to the regulation of compensation in such cases is an implied condition 147*147 of the grant, and the State, in exercising its power of prescribing the compensation, only determines the conditions upon which its concession shall be enjoyed. When the privilege ends, the power of regulation ceases.

[Munn v. Illinois, 94 U.S. 113, 146-147 (1877);

SOURCE: https://scholar.google.com/scholar_case?case=6419197193322400931]

Notice the word “concession” above. Government is SELLING their services and renting their PROPERTYPUB for a fee called “taxes”. The PUBLIC civil status and the PRIVILEGES that attach to it are the PROPERTYPUB being rented. FURTHER, you as the owner of the protected PRIVATE property must formally ASK for the consideration or “benefit” by filling out a government form. They can’t make you pay for PROTECTION that you DO NOT WANT! That would make them a mafia who collects “protection money” or “extortion money”.

If the taxing power be in no position to render these services, or otherwise to benefit the person or property taxed, and such property be wholly within the taxing power of another State, to which it may be said to owe an allegiance and to which it looks for protection, the taxation of such property within the domicil of the owner partakes rather of the nature of an extortion than a tax, and has been repeatedly held by this court to be beyond the power of the legislature and a taking of property without due process of law. Railroad Company v. Jackson, 7 Wall. 262; State Tax on Foreign-held Bonds, 15 Wall. 300; Tappan v. Merchants’ National Bank, 19 Wall. 490, 499; Delaware &c. R.R. Co. v. Pennsylvania, 198 U.S. 341, 358. In Chicago &c. R.R. Co. v. Chicago, 166 U.S. 226, it was held, after full consideration, that the taking of private property 203*203 without compensation was a denial of due process within the Fourteenth Amendment. See also Davidson v. New Orleans, 96 U.S. 97, 102; Missouri Pacific Railway v. Nebraska, 164 U.S. 403, 417; Mount Hope Cemetery v. Boston, 158 Massachusetts, 509, 519.

[Union Refrigerator Transit Co. v. Kentucky, 199 U.S. 194, 202-203 (1905); SOURCE: https://scholar.google.com/scholar_case?case=14163786757633929654]

The income tax is not a tax on wagesPRI, salariesPRI, tips or commissionsPRI, income, or gross income as PRIVATE propertyPRI, which are tangible fruits in the form of money and all constitute private propertyPRI when earned by a human being operating in a private capacity. BUT, when these forms of property are instead earned by an office or status legislatively created and therefore owned by Congress, such as “employee” (26 U.S.C. §3402), “U.S. person” (26 U.S.C. §7701(a)(30)), or “person” (26 U.S.C. §6671(b) and 7343), they become public propertyPUB subject to excise taxation and the EVENT taxed is the use of public propertyPUB in connection with otherwise private commerce. The public propertyPUB subject to tax is the CIVIL STATUSPUB itself. The tax is avoidable by avoiding the privilege and the PUBLIC civil statusPUB that it attaches to. In all cases we are aware of, you have to VOLUNTEER for the civil statusPUB that the tax attaches to. That’s why “U.S. person” is voluntary and those who don’t volunteer are called “nonresident aliens”. If you want to make SURE you don’t acquire these statusesPUB inadvertently, simply define all terms on any form you send the government as NOT including the civil statutory context and only applying to the constitutional and private context. Thus, they cannot impute “purposeful availment” under the Minimum Contacts Doctrine of the U.S. Supreme Court that would cause a surrender of sovereign immunity and consent to be taxed and regulated.

Because of the Sixteenth Amendment, Congress may, once again, tax income with uniformity (i.e. without apportionment), but the tax must obey the rules for uniformity and be in the form of an indirect tax. The Courts can no longer place a tax on income in the category of direct taxation by considering the source (of capital). The Court provided a complete review and analysis of what is and is not a direct tax in the 2012 Obamacare decision when the Petitioners argued that the penalty was a direct tax that must be apportioned:

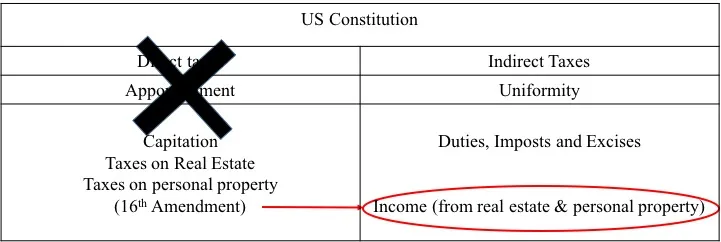

That narrow view of what a direct tax might be persisted for a century. In 1880, for example, we explained that “direct taxes,” within the meaning of the Constitution, are only capitation taxes, as expressed in that instrument, and taxes on real estate.” Springer, supra, at 602. In 1895, we expanded our interpretation to include taxes on personal property[PRI] and income from personal property[PRI], in the course of striking down aspects of the federal income tax.Pollock v. Farmers’ Loan & Trust Co., 158 U.S. 601, 618 (1895). That result was overturned by the Sixteenth Amendment, although we continued to consider taxes on personal property to be direct taxes. See Eisner v. Macomber, 252 U.S. 189–219 (1920).

[National Federation of Independent Businesses v. Sebelius, 567 U.S. 519, 598 (2012);

SOURCE: https://scholar.google.com/scholar_case?case=12815172896965834886]

The Chief Justice is explaining how the Constitution’s definition of “direct tax” changed over the years. The 16th Amendment merely modifies the Constitution’s definition of “direct tax,” it does not alter the Constitution’s rules for taxation. When analyzing the Obamacare penalty to determine if it qualified as a “direct tax,” the Chief Justice reasoned:

A tax on going without health insurance does not fall within any recognized category of direct tax. It is not a capitation. Capitations are taxes paid by every person, “without regard to property, profession, or any other circumstance.” … The payment is also plainly not a tax on the ownership of land or personal property. The shared responsibility payment is thus not a direct tax that must be apportioned among the several States.

[National Federation of Independent Businesses v. Sebelius, 567 U.S. 519, 574 (2012);

SOURCE: https://scholar.google.com/scholar_case?case=12815172896965834886]

Did the reader notice that a tax on “income” is not a recognized category of “direct tax”? After the Sixteenth Amendment, taxes on personal propertyPRI are still considered “direct taxes,” but taxes on income are not “direct taxes.” As of 2012, the three recognized categories of “direct tax are:” A capitation, a tax on real estate and a tax on personal propertyPRI (including money). The DC Circuit said much the same thing in Murphy v. IRS:

Only three taxes are definitely known to be direct: (1) a capitation, U.S. Const. art. I, § 9, (2) a tax upon real property, and (3) a tax upon personal property.

[Murphy v. IRS 493 F.3d. 170,179 (2007);

SOURCE: https://scholar.google.com/scholar_case?case=606795644459520694]

The Sixteenth Amendment modified the constitutional definition of “direct tax,” it did not amend the Constitution’s rules for taxation. After the amendment, all direct taxes still require apportionment and all indirect taxes require uniformity. The question has always been, is a tax on income included within the constitutional definition of a “direct tax” or not? In Springer v. United States the Supreme Court said the tax on income is not a “direct tax,” but an excise. In Pollock the Supreme Court reversed itself and concluded that the tax on income is a “direct tax.” The Sixteenth Amendment overruled the Supreme Court and says that the tax on income is not a “direct tax.”

5. The Subject of the Tax

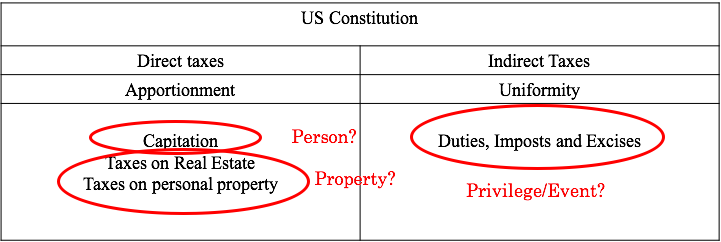

A tax must have a subject meaning the thing being taxed. A tax imposed on a car means that the car is the subject of the tax. A tax imposed on money means that money is the subject of the tax. The subject of a tax may also be an activity a privilege or an event. One must identify the subject of the tax before it is possible to identify the tax as a “direct tax” or a duty, impost or excise. In our system, the subject of a tax is limited to the items shown below:

The subject of a tax may be a personPUB, propertyPUB or some kind of event or privilege. Money is property and must be taxed as property. A tax on OWNERSHIP of private property is a recognized category of direct tax that must be apportioned. This is where the analysis should stop.

However, the analysis does not stop there because Congress wants to tax PRIVATE propertyPRI in the form of money, but the apportionment requirement prevents the Federal Government from directly meddling with the propertyPRI of American nationals. Apportionment is hard and so Congress would rather tax money as propertyPUB by the rule of uniformity because it is easy. To tax money by uniformity, Congress must devise a way to tax money by changing who the OWNER is from PRIVATE to PUBLIC without you knowing it and thus making the tax indirect. They can tax their own offices as their propertyPUB and all the propertyPUB attached to said offices by the SSN/TIN franchise mark. To achieve this objective, Congress applies the four ways to tax money described in Doyle:

Whatever difficulty there may be about a precise and scientific definition of “income,” it imports, as used here, something entirely distinct from principal or capital either as a subject of taxation or as a measure of the tax.

[Doyle v. Mitchell Bros., 247 U.S. 179, 185 (1918);

SOURCE: https://scholar.google.com/scholar_case?case=1447070231071484109]

Income and principal are the two categories of money and each category can be taxed in two different ways: As the subject of the tax or as the measure of the tax. Thus, the four ways to tax money are:

- Income as the subject of the tax: A direct tax on money that requires apportionment.

- Income as the measure of the tax: An indirect tax on money that requires uniformity.

- Principal as the subject of the tax: A direct tax on money that requires apportionment.

- Principal as the measure of the tax: An indirect tax on money that requires uniformity.

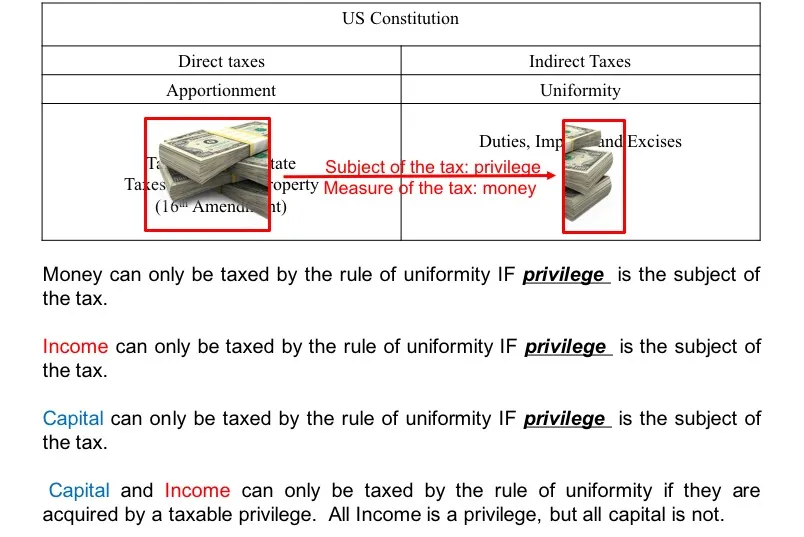

Introducing “the measure of the tax.” The measure of the tax is a legal invention to evade the apportionment requirement for taxing money. The Supreme Court has recognized the distinction when money is used as the subject of the tax (direct tax) and when money is used as the measure of the tax (indirect tax). If money is the subject of the tax, the tax falls on propertyPRI and is a direct tax that requires apportionment. If money is the measure of the tax, then something else is used as the subject of the tax and the tax is an indirect tax that requires uniformity.

In order to get around the apportionment requirement for taxing money, Congress has invented the idea of taxing privilege as the subject of the tax and using money as the measure of the tax in order to determine how much privilege one must pay for. Congress must target the money by taxing something else, which is what indirect means. Taxing privilege is the mechanism by which an indirect tax on money is constitutional.

If a person has $100,000 in income and Congress imposes a tax on the $100,000, meaning on the money itself, then it is a tax on propertyPRI and must be apportioned.

However, if Congress says the $100,000 was acquired by a privilege and taxes the privilege and uses the money as the measure of the tax to determine how much the privilege will cost, it is an indirect tax that can be collected by uniformity. How can a privilege be taxed? What does that even mean? The only way to tax a privilege, activity or an event is to assign it a dollar value. And this is why the “measure of the tax” was invented by American lawyers:

The money is the real target of the tax, but the money is being targeted indirectly instead of directly. Congress targets the money by taxing voluntary POSITIONS or STATUSES, which is what indirect means. The amount of tax that the POSITION or STATUS then pays is exactly the same. This is just legal mumbo-jumbo to get around the apportionment requirement for taxing money. However, now it is necessary to split hairs to determine which money can be taxed as a privilege and which money cannot.

Without privilege, money can only be taxed as PRIVATE propertyPRI, by the rule of apportionment. Not all money can be taxed as a privilege (all income can, but all capital cannot). The Courts have accepted this innovation as illustrated by these examples:

Congress in exercising the right to tax a legitimate subject of taxation as a franchise or privilege, was not debarred by the Constitution from measuring the taxation by the total income, although derived in part from property which, considered by itself, was not taxable.

[Stratton’s Independence v. Howbert, 231 U.S. 399, 416-417(1913);

SOURCE: https://scholar.google.com/scholar_case?case=11971357151204259952]

They are based on two principles: 1. An inheritance tax is not one on property, but one on the succession. 2. The right to take property by devise or descent is the creature of the law, and not a natural right – a privilege, and therefore the authority which confers it may impose conditions upon it.

[Knowlton v. Moore, 178 U.S. 41, 55 (1900);

SOURCE: https://scholar.google.com/scholar_case?case=16237964956954109764]

It is this distinctive privilege which is the subject of taxation, not the mere buying or selling or handling of goods.

While a direct tax may be void if it reaches nontaxable property, the measure of an excise tax on privilege may be the income from all property, although part of it may be from that which is nontaxable.

But this argument confuses the measure of the tax upon the privilege with direct taxation of the state or thing taxed.

[Flint v. Stone Tracy Co., 220 U.S. 107, 162 (1911);

SOURCE: https://scholar.google.com/scholar_case?case=17853944152368373401]

These authorities establish that Congress taxes privileges and that the mumbo-jumbo has become venerated legal precedent. This fact may be a surprise to some. The tax on income uses privilege as the subject of the tax and income as the measure of the tax and this is how a tax on income is imposed indirectly using the rule of uniformity.

After the Sixteenth Amendment, a tax on income is collected “without apportionment,” which means it must be collected with uniformity. Therefore, a tax on income must conform to the Constitution’s rule for uniformity and must be a duty, an impost or an excise or, in other words, an indirect tax. Knowlton v. Moore (178 US 41, 1900) confirms that uniformity is imposed “only on duties, imposts and excises” – not direct taxes:

Thus, the qualification of uniformity is imposed not upon all taxes which the Constitution authorizes, but only on duties, imposts and excises.

In order for the tax on income to conform to the Constitution’s rule for uniformity, it must be enacted as an indirect tax and thus, money cannot be the subject of the tax. A privilege, an activity or an event must be the subject of the tax because it provides the indirection that is needed for the tax to qualify for the rule of uniformity. Congress targets the money by taxing privilege. This explains why income must be the measure of the tax, and not the subject of the tax. This concept further explained by former legislative draftsman for Treasury Department, F. Morse Hubbard in the 1943 Congressional Record:

So the amendment made it possible to bring investment income within the scope of a general income-tax law, but did not change the character of the tax. It is still fundamentally an excise or duty with respect to the privilege of carrying on any activity or owning any property which produces income.

The income tax is, therefore, not a tax on income as such. It is an excise tax with respect to certain activities and privileges which is measured by reference to the income which they produce. The income is not the subject of the tax: it is the basis for determining the amount of tax.

[1943 Congressional Record Vol 89, Part 2 pg. 2580]

The admission that “The income tax is, therefore, not a tax on income as such,” is evidence that a word game is being played. Mr. Hubbard means that the income tax does not tax money. If the income tax doesn’t tax income, then what does it tax? It taxes “privilege” and uses income as the measure of the tax and this is being done specifically to evade the apportionment requirement for taxing money.

Congress may tax incomes either with apportionment of without apportionment at its own discretion, it simply must follow the rules for each tax. An income tax collected with apportionment is a direct tax; an income tax collected without apportionment is an indirect tax. The Sixteenth Amendment did not strip from Congress the power to tax income by apportionment if it chooses. The Amendment says, “Congress shall have power to lay and collect taxes on incomes…without apportionment” and like any power granted to Congress, it may choose to exercise that power or choose not to exercise it. Congress is not required to tax income without apportionment.

To exercise the Authority of the Sixteenth Amendment and tax income “without apportionment,” Congress must tax the privileges and activities that produce income and not the money. From its inception in 1861, the Income Tax has never been conceived as a tax on the moneyPRI itself. The tax is on the privileges or activities that produce incomePUB, which allows it to be taxed by uniformity and not apportionment. The activities that produce income are investment activities. The activities that produce capital are employment activities. United States is the only country in the world where this legal legerdemain is required to tax property because the apportionment requirement is designed to protect an American national’s propertyPRI from direct federal taxation.

6. The First Income Tax

Congress passed its first income tax in 1861 because of the extra revenue needed for the Civil War. In 1880, the decision in Springer cited above decided that the tax on income was an indirect tax: “The duty which the internal revenue acts provided should be assessed, collected and paid upon gains, profits, and income was an excise or duty and not a direct tax, within the meaning of the Constitution.” The tax was allowed to lapse soon after the war ended but was revived in 1894.

It wasn’t long after the new tax was enacted that it was challenged. But this time the Supreme Court, in Pollock v. Farmer’s Loan and Trust (1895), decided that the income tax was a direct tax and must be collected by the rule of apportionment.

The Court said that if the source from which the income is derived must be taxed by apportionment, then the income derived from the source also must be taxed by the rule of apportionment. This was the origin of the “source” argument that was abolished by the Sixteenth Amendment. The Court’s two primary holdings are:

Our conclusions may, therefore, be summed up as follows:

First. We adhere to the opinion already announced, that, taxes on real estate being indisputably direct taxes, taxes on the rents or income of real estate are equally direct taxes.

Second. We are of opinion that taxes on personal property, or on the income of personal property, are likewise direct taxes.

[Pollock v. Farmer’s Loan and Trust, 158 U.S. 601, 637 (1895);

SOURCE: https://scholar.google.com/scholar_case?case=14112562519763534846]

Income is derived from capital. Real estate and personal property are the two generic sources of capital from which income is derived. Income is either derived from rents and gains from real estate or it is derived from investing personal property (money) into any type of investment. While capital may take many forms, in the context of income tax, capital in the form of money (personal property) is the focus here. Real estate and money are both forms of property. During the congressional debates on the income tax, Senator Williams noted:

Money is as much property as is anything else, and when a man earns $20,000 in money during a year he has got that much in property

[Congressional Record, Vol L, Part 4 pg. 3838]

When people get paid for labor, they receive property in the form of money as also noted by Senator Williams:

[S]o that the man whose property consists in dollars which he earns in a year is the least taxed of all men.

[Congressional Record, Vol L, Part 4 pg. 3839]

The reference to “personal property” in the decision means money. “Invested personal propertyPRI” means money (capital) invested to produce income, which includes investments of all kinds. One does not invest a house into something so a house is not the kind of personal propertyPRI to which the decision refers. In the context of income tax, personal propertyPRI is the capital that is invested to produce income and together with real estate identify the two sources of capital discussed in Pollock. In Pollock, the Court reasoned:

. . .it is evident that the income from realty formed a vital part of the scheme for taxation embodied therein. If that be stricken out, and also the income from all invested personal property, bonds, stocks, investments of all kinds, it is obvious that by far the largest part of the anticipated revenue would be eliminated, and this would leave the burden of the tax to be borne by professions, trades, employments, or vocations, and in that way what was intended as a tax on capital would remain in substance a tax on occupations and labor. We cannot believe that such was the intention of Congress

[Pollock v. Farmer’s Loan and Trust, 158 U.S. 601, 636-637 (1895);

SOURCE: https://scholar.google.com/scholar_case?case=14112562519763534846]

Real estate was already recognized as a direct tax and the Court concluded that the tax on income from real estate was also a direct tax. After Pollock, the definition of “direct tax” was expanded when the Court ruled, “Second. We are of opinion that taxes on personal property, or on the income of personal property, are likewise direct taxes.” In 1895, personal property and income (from real estate and personal property) were all added to the legal definition of “direct tax”:

After Pollock, a tax on investment earnings became a “direct tax” and could not be taxed by Congress unless it went through the rule of apportionment. This angered many because all this idle wealth, as it was described, could not be used to support the government. In his dissent, Justice Harlan stated:

Why do I say that the decision just rendered impairs or menaces the national authority? The reason is so apparent that it need only be stated. In its practical operation, this decision withdraws from national taxation not only all incomes derived from real estate, but tangible personal property, “invested, personal property, bonds, stocks, investments of all kinds,” and the income that may be derived from such property. This results from the fact that, by the decision of the court, all such personal property and all incomes from real estate and personal property, are placed beyond national taxation otherwise than by apportionment among the States on the basis simply of population. No such apportionment can possibly be made without doing gross injustice to the many for the benefit of the favored few in particular States.

[Pollock v. Farmer’s Loan and Trust, 158 U.S. 601, 671 (1895);

SOURCE: https://scholar.google.com/scholar_case?case=14112562519763534846]

To reverse this decision, and restore investment earnings to the category of indirect taxes so they can be taxed “without apportionment,” the Sixteenth Amendment was ratified:

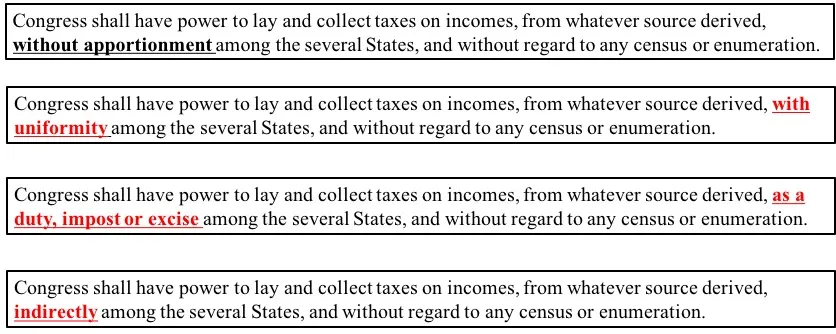

The Congress shall have power to lay and collect taxes on incomes, from whatever source derived, without apportionment among the several states, and without regard to any census or enumeration

[Sixteenth Amendment, US Constitution;

SOURCE: https://law.justia.com/constitution/us/amendment-16/]

The Sixteenth Amendment applies only to the income (profit), not the capital or personal property from which the income is derived.

- The Supreme Court said, “Hey, the tax on income is a direct tax and must be taxed with apportionment.”

- The Sixteenth Amendment responded, “Oh no it’s not. The tax on income can be collected without apportionment, because it is not a direct tax.”

For those who understand logical reasoning, the Amendment is written using the contrapositive:

- Original Constitutional Proposition: If the tax is direct, the tax is apportioned.

- Contrapositive: If the tax is not apportioned, the tax is not direct

If the Income Tax is collected without apportionment, then the Income Tax is not a direct tax. The Sixteenth Amendment did not change the rules. The tax structure is a logical construct with only two choices: “P” and “not P;” so not one means the other. “Not direct” means “indirect.” “Not indirect” means “direct.” “Without apportionment” means “with uniformity.” If the income tax is collected without apportionment, then it must be collected with uniformity. If the income taxed is collected with uniformity, then the tax must conform to all the rules for uniformity. The tax must be enacted as an indirect tax, meaning a duty, an impost or an excise.

“Without apportionment” can only mean “with uniformity” and therefore, all four of these are logically equivalent statements:

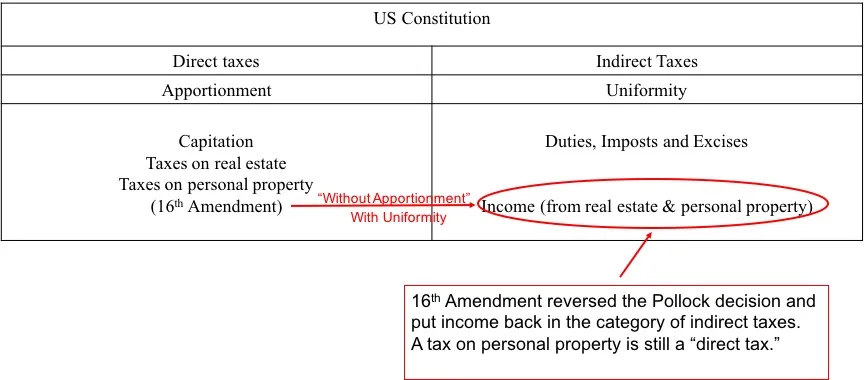

The Sixteenth Amendment reversed the Pollock decision by modifying the constitutional definition of “direct tax” to exclude income. The tax on personal propertyPRI is still a “direct tax.” After the Sixteenth Amendment and as of 2012, the tax structure looks like this:

In order to be collected by the constitutional rule of uniformity, the tax on income, from both real estate and personal propertyPRI, must be one of the many excise taxes in the Internal Revenue Code, which is an indirect tax. The Supreme Court unequivocally confirms this analysis in the following decision:

The Sixteenth Amendment conferred no new power of taxation, but simply prohibited the previous complete and plenary power of income taxation possessed by Congress from the beginning from being taken out of the category of indirect taxation to which it inherently belonged, and being placed in the category of direct taxation subject to apportionment by a consideration of the sources from which the income was derived.

[Stanton v. Baltic Mining Co., 240 U.S. 103, 112-113 (1916);

SOURCE: https://scholar.google.com/scholar_case?case=726253341774342162]

7. Direct Tax/Apportionment

A direct tax applies to land or directly to humans “without regard to property, profession, or any other circumstance.” Hylton v. United States (1796); see also NFIB v. Sebelius (2012). Such a tax must be apportioned. At the time of the Constitutional Convention, states with large amounts of land, as well as those with large populations, feared heavier taxes on their land and populations, including slaves, as compared to smaller and less populous states. The apportionment requirement, which also governs representation in the House of Representatives, became the compromise. See Article I, Section 2.

To be apportioned, a tax must be the same amount per person in every state, a very difficult burden to satisfy. For example, a dollar-per-acre tax would fail unless every state had the same acreage per capita. As a result, federal land taxes do not exist. States, unhampered by apportionment, routinely impose real property taxes. In contrast, a dollar-per-human tax (also known as a capitation) would be constitutional, as it would be the same amount per capita in every state. The United States, however, has never imposed such a tax, arguably the only form that a direct tax could constitutionally take. In 2012, the Supreme Court considered whether the “shared responsibility payment” for lacking health insurance in the Affordable Care Act was a direct tax, and held that it was not: while applying directly to humans, it varies depending on whether they have health insurance, an “other circumstance.” NFIB v. Sebelius. Quoting Hylton, the Court held the required payment to be non-direct, and citing Pollock, concluded that the payment is not an income tax.

The current income tax is implemented as a privilege tax upon government/public propertyPUB paid or rendered to the recipient MEASURED by its value. As such, the tax is an excise/indirect tax that is subject to the requirement for either apportionment or uniformity.

8. Indirect Tax/Uniformity

Duties, imposts, and excises must be uniform. See Article I, Section 8, Clause 1. As “indirect” taxes, they do not apply directly to humans. For example, a duty applies to the act of importing property. Although the ultimate purchaser suffers the tax, the incidence (or burden of the tax) is thought to fall primarily on the importer, and therefore it is considered to be indirect. Excises commonly apply to tires, telephone charges, gambling, employment, and corporate income. In each case, humans may ultimately suffer the tax through higher prices or lower wages, but the incidence is viewed as indirect through the seller, employer, or entity.

Unlike apportionment, uniformity does not require each person to pay the same amount; instead, it requires the same rate structure to exist nationally. For example, Congress may tax truck tires differently than bicycle tires; but however it taxes truck tires, the specific truck tire rates must be the same in every state. As such, it is a geographic requirement. Steward Machine Co. v. Davis (1937); Flint v. Stone Tracy Co. (1911); Knowlton v. Moore (1900). The Supreme Court has never struck down an indirect tax as failing uniformity, although it has considered the issue several times. Uniformity analysis is not easily reducible to black-letter rules; nevertheless, some such rules emerge:

- Taxes may vary by an object’s value or the taxpayer’s income so long as the rates are uniform. They may even apply to objects or transactions found only in some states, such as snow tires in the north or beach umbrellas in coastal states. Edye v. Robertson (Head Money Cases) (1884).

- Tax rates may vary if based on physical, such as coastlines and frigid conditions; however, such variations necessitate a particularly close examination. For instance, in United States v. Ptasynski(1983), the Court distinguished arctic oil from oil produced elsewhere. It upheld a tax on income derived from oil pumped above the Arctic Circle. Rates may also vary because of isolated problems or “diverse conditions.” Florida v. Mellon (1927). How isolated or diverse the problem or condition must be is unclear.

Although Congress cannot impose a property tax directly on personal propertyPRI—such as cars, furniture, stocks or bonds—as opposed to land—, it has two fairly easy work-arounds for such taxes. NFIB v. Sebelius (2012). Since 1796, the Supreme Court has viewed a tax on the use of personal property as an indirect tax subject to uniformity rather than to apportionment. Hylton v. United States (1796) (Chase, J.). As a result, it could easily style a tax on automobiles as a tax on the use of the item and thus avoid apportionment. Indeed, because the number of cars (or any other personal item) is unlikely ever to be the same per capita in every state, without the Hylton decision, a federal personal property tax would be impossible because it could never satisfy apportionment. Although Congress does not often impose direct taxes on personal property, Congress routinely imposes similar taxes on the purchase of personal property such as tires and gasoline, styling them as excises subject merely to uniformity. Significantly, it could impose a nationwide automobile or telephone usage tax.

Until 1913, a tax on either personal or real propertyPRI income was effectively forbidden because such taxes were considered direct and not easily apportioned. Pollock v. Farmers’ Loan & Trust Co. (1895). The Sixteenth Amendment resolved this by replacing the income tax apportionment requirement with a new requirement that a tax on income need not be apportioned so long as the tax is imposed on income “derived from a source”—a serious, but different restriction.

In 2012, the Supreme Court narrowly read the direct tax definition in relation to the Affordable Care Act (ACA). The Court held the ACA penalty on persons without minimum health insurance to be a tax; however, the Court also held it not to be “any kind of direct tax.” NFIB v. Sebelius (2012). In so doing, the Court made two critical points. First, by citing Pollock favorably, the Court removed any argument that the “penalty” was supportable as an income tax subject to the “derived” test. That was important because the “tax” is, in part, a function of a person’s income. Without the Sixteenth Amendment as a possible foundation, the tax/penalty must satisfy either apportionment or uniformity. Second, the Court relied on the often-quoted 1796 Hylton language: a direct tax is one imposed “without regard to property, profession, or any other circumstance.” Finding the lack of health insurance an “other circumstance,” the Court found that the mandate to purchase insurance was not a direct tax, and it rejected apportionment as applying to the ACA.

Interestingly, the Court quoted Justice Chase out of context. Chase actually said: “I am inclined to think, but of this I do not give a judicial opinion, that the direct taxes contemplated by the Constitution are only two, to wit, a capitation or poll tax simply, without regard to property, profession, or any other circumstances, and the tax on land.” Hylton v. United States (1796) (Chase, J.). The NFIB Court thus omitted Chase’s independent clause and quoted only the dependent clause, which he described as not his “judicial opinion”; however, it labeled the quotation as “opinion of Chase, J.” which is best described as misleading. Nevertheless, the NFIB decision appears settled: the ACA tax is neither a direct tax nor an income tax.

9. Income Tax/Derived

Income taxes may be imposed only on “derived” income. By “derived” we mean separated from the capital or transaction through a SALE of some kind:

After examining dictionaries in common use (Bouv. L.D.; Standard Dict.; Webster’s Internat. Dict.; Century Dict.), we find little to add to the succinct definition adopted in two cases arising under the Corporation Tax Act of 1909 (Stratton’s Independence v. Howbert, 231 U.S. 399, 415; Doyle v. Mitchell Bros. Co., 247 U.S. 179, 185) — “”Income may be defined as the gain derived from capital, from labor, or from both combined,” provided it be understood to include profit gained through a sale or conversion of capital assets, to which it was applied in the Doyle Case (pp. 183, 185).

Brief as it is, it indicates the characteristic and distinguishing attribute of income essential for a correct solution of the present controversy. The Government, although basing its argument upon the definition as quoted, placed chief emphasis upon the word “gain,” which was extended to include a variety of meanings; while the significance of the next three words was either overlooked or misconceived. “Derived — from — capital;” — “the gain — derived — from — capital,” etc. Here we have the essential matter: not a gain accruing to capital, not a growth or increment of value in the investment; but a gain, a profit, something of exchangeable value proceeding from the property, severed from the capital however invested or employed, and coming in, being “derived,” that is, received or drawn by the recipient (the taxpayer) for his separate use, benefit and disposal; — that is income derived from property. Nothing else answers the description.

The same fundamental conception is clearly set forth in the Sixteenth Amendment — “incomes, from whatever source derived” — the essential thought being expressed 208*208 with a conciseness and lucidity entirely in harmony with the form and style of the Constitution.

[Eisner v. Macomber, 252 U.S. 189, 207-208 (1920);

SOURCE: https://scholar.google.com/scholar_case?case=6666969430777270424]

This “realization event” requirement generally refers to a transaction other than the mere passage of time. Thus the Sixteenth Amendment permits taxation of gains realized through sales or exchanges of property, but not those resulting merely from increased values where there is no sale or exchange.

10. Importance of Understanding Direct Taxes to Nonresident Aliens

- If there is no privilege as in 26 U.S.C. §871(a), then its not an excise or indirect tax. In this case, the only privilege is “trade or business within the United States” in 26 U.S.C. §864(b).

- If it’s not an excise or indirect tax, then it has to be a foreign affairs function under sovereign power and Article 1, Section 8, Clause 3.

- And if it’s not an excise or indirect tax but it’s on American nationals (U.S. nationals) standing on land protected by the constitution, then its an unconstitutional direct tax.

- Because foreign nationals (NRAAliens/foreignP personsPUB) abroad don’t have constitutional protections, they are not protected by the prohibition on non-apportioned direct taxes. Thus, they CAN and DO have a direct non-apportioned tax levied on their profits as FDAP in 26 U.S.C. §871(a).

The Constitution identifies itself as “the law of the land” that protects only people standing on that land. Foreign nationals abroad are NOT standing on land protected by the Constitution. These foreign nationals are the ones to whom the following phrase in the Sixteenth Amendment applies:

“… without apportionment among the several States, and without regard to any census or enumeration ….”

In every other application it is simply a voluntary federal franchise tax under the proprietorial powers of Congress. Offering you the “personal services” position/status in 26 U.S.C. §864(b) is what MAKES it a proprietorial power. They are NOT talking about human services, but servicesPUB of a position or status as an agent of the national government occupied by a private human volunteer who made an election to become a “U.S. person” or a “nonresident alien” who “effectively connects”. For proof of this, see:

Copilot: Meaning of civil statutory “services”, FTSIG

https://ftsig.org/copilot-meaning-of-civil-statutory-services/

Judicial verbicide and equivocation sometimes is abused to make these “proprietorial powers” LOOK like “sovereignPUB powersPUB” over foreign affairs, when really they are referring to “sovereignPRI powerPRI” over government propertyPUB consisting in this case of the civil statutory STATUSPUB that they legislatively created and own which is engaging in “personal servicesPUB” rendered NOT to the third party contracting the services, but to Uncle Sam renting out its representatives to third parties. They are running a “rent and ident” service, as we say on the opening page of this website. This process would be instantly obvious if they only merely defined “services” and “personal servicesPUB” so they NEVER do and NEVER WILL. In scenarios where contracting Third parties are involved, for instance, there are TWO levels of “service” going on:

- You serve the position/status of “taxpayerPUB” as a volunteer who doesn’t even KNOW they are a volunteer in most cases. Your legal ignorance makes the volunteering process invisible and makes you what the Soviets called a “useful idiot”. See:

Taxpayer v. Nontaxpayer, FTSIG

https://ftsig.org/introduction/taxpayer-v-nontaxpayer/ - The United States corporation is the principal and you are the agent under the law of agency. See:

Treatise on the Law of Agency, Floyd Mechem

http://books.google.com/books?id=n2c9AAAAIAAJ&printsec=titlepage - Your “employment agreement” are the laws “created or organized” and therefore OWNED by Uncle Sam, which collectively are called “domestic” in 26 U.S.C. §7701(a)(4)

- The position serves the United States federal corporation AND the third party you contract with.

- The franchise mark and the name of the position/statusPUB are synonymous symbols of agency and constitute what the Supreme Court calls your “clothing”. This status is called a “straw man”. See:

Proof that There Is a “Straw Man”, Form #05.042

https://sedm.org/Forms/05-MemLaw/StrawMan.pdf - The actions of the agent or straw man are supervised and managed by the Administrative State as an “instrumentality” of the United States through administrative enforcement and distraint under 26 U.S.C. §6331:

Administrative State: Tactics and Defenses Course, Form #12.041

https://sedm.org/LibertyU/AdminState.pdf

You don’t know all this because it’s a third rail issue. See:

Third Rail Government Issues, Form #08.032

https://sedm.org/Forms/08-PolicyDocs/ThirdRailIssues.pdf

NOWHERE has ANY court ever described or defined how the civil statutory STATUSPUB of “personPUB” and the HUMANPRI become legally connected and whether consent or election is involved. This is no accident, but a diabolical secret plan of human enslavement invisible to the legally ignorant. Welcome to the Matrix, Neo!

Uncle Sam is in the franchising business. LONG before McDonald’s built its first franchise store, Uncle was building the model for franchising. All McDonald’s did was COPY IT and institutionalize it in the private sector! The problem is that NONE OF THIS is expressly authorized by the Constitution, so it’s quite suspect and deplorable. It’s just proprietary business activity engineered to raise revenue and expand the government beyond its constitutional limits into a Frankenstein monster. We call that monster a de facto government in below:

De Facto Government Scam, Form #05.043

https://sedm.org/Forms/05-MemLaw/DeFactoGov.pdf

These considerations are also why it’s critical to know that “personal servicesPUB” in the “United States” doesn’t mean in the United StatesG, which is really a veil for United StatesGOV.

United StatesG is not literally “geography,” but a federal preemption label that serves to hide the real source and connection of “personal services”—United StatesGOV. When you see United StatesG (the curtain) know that United StatesGOV is hiding behind that curtain. And United StatesG is not simply referring to a place where one can engage in economic activity.

But you won’t understand it all until you understand the following third rail issues:

- That they can’t reach the PROPERTY without OWNING the OWNER.

- The OWNER that they OWN is the CIVIL “person” STATUSPUB they legislatively created.

- PropertyPUB is then attached to the STATUSPUB of “person” through the SSN/TIN franchise mark.

- Since Uncle owns the civil “person” STATUSPUB, they then own the PROPERTYPUB connected to it through the SSN/TIN franchise mark.

- Anything “trade or business” in 26 U.S.C. §7701(a)(26) or Effectively Connected under 26 U.S.C. §864(c) IS that civil “person” status. Your consent or election activates the position or status and recruits you into it. This INCLUDES either of the following who have in common “trade or business within the United StatesGOV” in 26 U.S.C. §864(b):

5.1. The “U.S. person” under 26 U.S.C. §7701(a)(30).

5.2. The “nonresident alien” who “effectively connects” under 26 U.S.C. §864(c).

11. Further Reading

If you would like to learn more about the subject of this page, see:

- Copilot: Is the income tax a DIRECT tax or an INDIRECT tax?, FTSIG

https://ftsig.org/copilot-is-the-income-tax-a-direct-tax-or-an-indirect-tax/ - HOW TO: How to distinguish “sovereign power” from “proprietary power” in the context of taxation, FTSIG

https://ftsig.org/how-to-how-to-distinguish-sovereign-power-from-proprietary-power-in-the-context-of-taxation/ - Constitutional Income: Do You Have Any?, Phil Hart

http://www.constitutionalincome.com/ - Sixteenth Amendment Congressional Debates, Exhibit #02.007

https://sedm.org/Exhibits/EX02.007.pdf - Legislative Intent of the Sixteenth Amendment-very enlightening

https://famguardian.org/Subjects/Taxes/16Amend/LegIntent16thAmend.htm - Taxation Page, Family Guardian Fellowship

https://famguardian.org/Subjects/Taxes/taxes.htm - Sovereignty Forms and Instructions Online, Form #10.004, Cites by Topic: “income”

https://famguardian.org/TaxFreedom/CitesByTopic/income.htm