DEFINITIONS: “Income”

What is Income-Attorney Larry Becraft

Court Case Citations on the Nature of “income”

The Character of “Income”

The Character of “Income”

How the Government Defrauds You of Legitimate Deductions for the Market Value of Your Labor, Form #05.026 (OFFSITE LINK) -why your personal labor is not “income” and how the government hides or avoids this.

The Taxing Power, the Sixteenth Amendmnet, and the Meaning of Income, Erik M. Jensen, Case Western Reserve University, School of Law

Constitutionally Exempt Regulations (OFFSITE LINK)-In earlier versions of the statutes, they recognized PRIVATE property protected by the Constitution. Now they just unconstitutionally PRESUME that everything is PUBLIC property owned by the government

Internal Revenue Code of 1939, Section 22: Gross Income -compensation of President and Judges is “gross income”. Everything else is on profit

Senator Cummins, 1913 Congressional Record, Vol L, Part 4 pg. 3843

“The word “income” had a well-defined meaning before the amendment of the Constitution was adopted. It has been defined in all the courts of this country. When the people of the country granted to Congress the right to levy a tax on incomes, that right was granted with reference to the legal meaning and interpretation of the word “income” as it was then or as it might thereafter be defined or understood in legal procedure. If we could call anything income that we pleased, we could obliterate all the distinction between income and principal.”

26 C.F.R. §1.1001-1 – Computation of gain or loss.

26 C.F.R. §1.1001-1 – Computation of gain or loss.

§ 1.1001-1 Computation of gain or loss.

(a) General rule.

Except as otherwise provided in subtitle A of the Code, the gain or loss realized from the conversion of property into cash, or from the exchange of property for other property differing materially either in kind or in extent, is treated as income or as loss sustained. The amount realized from a sale or other disposition of property is the sum of any money received plus the fair market value of any property (other than money) received. The fair market value of property is a question of fact, but only in rare and extraordinary cases will property be considered to have no fair market value. The general method of computing such gain or loss is prescribed by section 1001 (a) through (d) which contemplates that from the amount realized upon the sale or exchange there shall be withdrawn a sum sufficient to restore the adjusted basis prescribed by section 1011 and the regulations thereunder (i.e., the cost or other basis adjusted for receipts, expenditures, losses, allowances, and other items chargeable against and applicable to such cost or other basis). The amount which remains after the adjusted basis has been restored to the taxpayer constitutes the realized gain. If the amount realized upon the sale or exchange is insufficient to restore to the taxpayer the adjusted basis of the property, a loss is sustained to the extent of the difference between such adjusted basis and the amount realized. The basis may be different depending upon whether gain or loss is being computed. For example, see section 1015(a) and the regulations thereunder. Section 1001(e) and paragraph (f) of this section prescribe the method of computing gain or loss upon the sale or other disposition of a term interest in property the adjusted basis (or a portion) of which is determined pursuant, or by reference, to section 1014 (relating to the basis of property acquired from a decedent), section 1015 (relating to the basis of property acquired by gift or by a transfer in trust), or section 1022 (relating to the basis of property acquired from certain decedents who died in 2010).

26 C.F.R. § 1.61-6 – Gains derived from dealings in property.

26 C.F.R. § 1.61-6 – Gains derived from dealings in property.

§ 1.61-6 Gains derived from dealings in property.

(a) In general. Gain realized on the sale or exchange of property is included in gross income, unless excluded by law. For this purpose property includes tangible items, such as a building, and intangible items, such as goodwill. Generally, the gain is the excess of the amount realized over the unrecovered cost or other basis for the property sold or exchanged. The specific rules for computing the amount of gain or loss are contained in section 1001 and the regulations thereunder. When a part of a larger property is sold, the cost or other basis of the entire property shall be equitably apportioned among the several parts, and the gain realized or loss sustained on the part of the entire property sold is the difference between the selling price and the cost or other basis allocated to such part. The sale of each part is treated as a separate transaction and gain or loss shall be computed separately on each part. Thus, gain or loss shall be determined at the time of sale of each part and not deferred until the entire property has been disposed of. This rule may be illustrated by the following examples:

Example 1.

A, a dealer in real estate, acquires a 10-acre tract for $10,000, which he divides into 20 lots. The $10,000 cost must be equitably apportioned among the lots so that on the sale of each A can determine his taxable gain or deductible loss.

Example 2.

B purchases for $25,000 property consisting of a used car lot and adjoining filling station. At the time, the fair market value of the filling station is $15,000 and the fair market value of the used car lot is $10,000. Five years later B sells the filling station for $20,000 at a time when $2,000 has been properly allowed as depreciation thereon. B’s gain on this sale is $7,000, since $7,000 is the amount by which the selling price of the filling station exceeds the portion of the cost equitably allocable to the filling station at the time of purchase reduced by the depreciation properly allowed.

(b) Nontaxable exchanges. Certain realized gains or losses on the sale or exchange of property are not “recognized”, that is, are not included in or deducted from gross income at the time the transaction occurs. Gain or loss from such sales or exchanges is generally recognized at some later time. Examples of such sales or exchanges are the following:

(1) Certain formations, reorganizations, and liquidations of corporations, see sections 331, 333, 337, 351, 354, 355, and 361;

(2) Certain formations and distributions of partnerships, see sections 721 and 731;

(3) Exchange of certain property held for productive use or investment for property of like kind, see section 1031;

(4) A corporation‘s exchange of its stock for property, see section 1032;

(5) Certain involuntary conversions of property if replaced, see section 1033;

(6) Sale or exchange of residence if replaced, see section 1034;

(7) Certain exchanges of insurance policies and annuity contracts, see section 1035; and

(8) Certain exchanges of stock for stock in the same corporation, see section 1036.

(c) Character of recognized gain. Under Subchapter P, Chapter 1 of the Code, relating to capital gains and losses, certain gains derived from dealings in property are treated specially, and under certain circumstances the maximum rate of tax on such gains is 25 percent, as provided in section 1201. Generally, the property subject to this treatment is a “capital asset”, or treated as a “capital asset”. For definition of such assets, see sections 1221 and 1231, and the regulations thereunder. For some of the rules either granting or denying this special treatment, see the following sections and the regulations thereunder:

(1) Transactions between partner and partnership, section 707;

(2) Sale or exchange of property used in the trade or business and involuntary conversions, section 1231;

(3) Payment of bonds and other evidences of indebtedness, section 1232;

(4) Gains and losses from short sales, section 1233;

(5) Options to buy or sell, section 1234;

(6) Sale or exchange of patents, section 1235;

(7) Securities sold by dealers in securities, section 1236;

(8) Real property subdivided for sale, section 1237;

(9) Amortization in excess of depreciation, section 1238;

(10) Gain from sale of certain property between spouses or between an individual and a controlled corporation, section 1239;

(11) Taxability to employee of termination payments, section 1240.

26 C.F.R. § 1.911-3 – Determination of amount of foreign earned income to be excluded.

§ 1.911-3 Determination of amount of foreign earned income to be excluded.

(a) Definition of foreign earned income.

For purposes of section 911 and the regulations thereunder, the term “foreign earned income” means earned income (as defined in paragraph (b) of this section) from sources within a foreign country (as defined in § 1.911-2(h)) that is earned during a period for which the individual qualifies under § 1.911-2(a) to make an election. Earned income is from sources within a foreign country if it is attributable to services performed by an individual in a foreign country or countries. The place of receipt of earned income is immaterial in determining whether earned income is attributable to services performed in a foreign country or countries.

26 U.S.C. §83 Property transferred in connection with performance of services

TITLE 26 > Subtitle A > CHAPTER 1 > Subchapter B > PART II > § 83

§ 83. Property transferred in connection with performance of services

(a) General rule

If, in connection with the performance of services [labor], property is transferred [compensation] to any person [employee] other than the person for whom such services are performed [employer], the excess of—

(1) the fair market value of such property [compensation] (determined without regard to any restriction other than a restriction which by its terms will never lapse) at the first time the rights of the person having the beneficial interest in such property are transferable or are not subject to a substantial risk of forfeiture, whichever occurs earlier, over

(2) the amount (if any) paid [labor] for such property [compensation], shall be included in the gross income of the person who performed such services [employee] in the first taxable year in which the rights of the person having the beneficial interest in such property are transferable or are not subject to a substantial risk of forfeiture, whichever is applicable. The preceding sentence shall not apply if such person sells or otherwise disposes of such property in an arm’s length transaction before his rights in such property become transferable or not subject to a substantial risk of forfeiture.

26 C.F.R. §39.21-1 (1956) Meaning of net income.

26 C.F.R. §39.21-1 (1956) Meaning of net income. (a) The tax imposed by chapter 1 is upon income. Neither income exempted by statute or fundamental law – (the Constitution), nor expenses incurred in connection therewith, other than interest, enter into the computation of net Income as defined by section 21 26 CFR 39.22(b)-1 Exemption — Exclusions from gross income. Certain items of income specified in section 22(b) are exempt from tax and may be excluded from gross income. These items however, are exempt only to the extent and in the amount specified. No other items may be excluded from gross income except (a) those items of income which are under the Constitution, not taxable by the Federal government;”

[26 C.F.R. §39.21-1 (1956)]

26 C.F.R. §1.61-1 (current)

26 C.F.R. §1.61-1 : Gross income. General definition: Gross income means all income from whatever source derived unless excluded by [FUNDAMENTAL/CONSTITUTIONAL] law.” [Also see 26 C.F.R. §1.312-6(b) “income not taxable by Federal Government under the Constitution”.]

[26 C.F.R. §1.61-1]

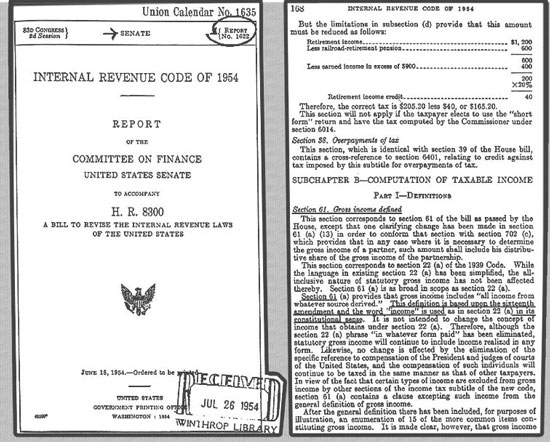

Internal Revenue Code of 1954, Senate Report 1622, “Report of the Committee on Finance, United States Senate, To Accompany H.R. 8300”, p. 168:

{kind=link}

“Section 61(a) provides that gross income includes “all income from whatever source derived.” This definition is based upon the sixteenth amendment and the word “income” is used as in section 22(a) in the constitutional sense. It is not intended to change the concept of income that obtains under section 22(a).”

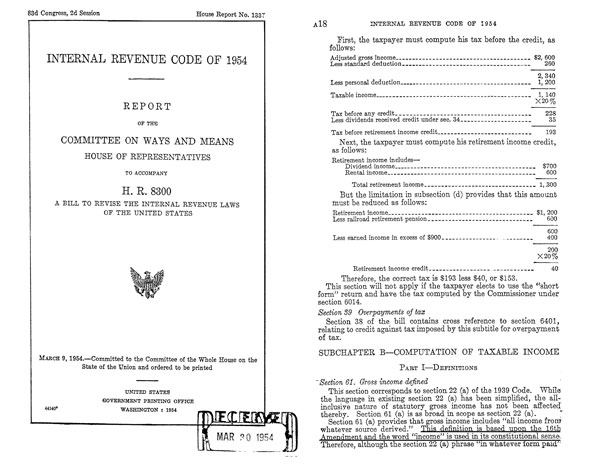

Internal Revenue Code of 1954, Report of the Committee on Ways and Means, House of Representatives, p. A18, March 9, 1954

{kind=link}

Section 61. Gross income defined

This section corresponds to section 22(a) of the 1939 Code. While the language in existing section 22(a) has been simplified, the all-inclusive nature of statutory gross income has not been affected thereby. Section 61(a) provides that gross income includes “all income from whatever source derived” This definition is based upon the 16 Amendment and the word “income” is used in its constitutional sense.

26 U.S.C. §643(b): Definitions applicable to Subparts A, B, C, and D

TITLE 26 > Subtitle A > CHAPTER 1 > Subchapter J > PART I > Subpart A > § 643

§ 643. Definitions applicable to subparts A, B, C, and D

(b) Income

For purposes of this subpart and subparts B, C, and D, the term “income”, when not preceded by the words “taxable”, “distributable net”, “undistributed net”, or “gross”, means the amount of income of the estate or trust for the taxable year determined under the terms of the governing instrument and applicable local law. Items of gross income constituting extraordinary dividends or taxable stock dividends which the fiduciary, acting in good faith, determines to be allocable to corpus under the terms of the governing instrument and applicable local law shall not be considered income.

26 C.F.R. §1.643(b)-1: Definition of income

Title 26: Internal Revenue

PART 1—INCOME TAXES

Estates, Trusts, and Beneficiaries

§ 1.643(b)-1 Definition of income.For purposes of subparts A through D, part I, subchapter J, chapter 1 of the Internal Revenue Code, “income,” when not preceded by the words “taxable,” “distributable net,” “undistributed net,” or “gross,” means the amount of income of an estate or trust for the taxable year determined under the terms of the governing instrument and applicable local law. Trust provisions that depart fundamentally from traditional principles of income and principal will generally not be recognized. For example, if a trust instrument directs that all the trust income shall be paid to the income beneficiary but defines ordinary dividends and interest as principal, the trust will not be considered one that under its governing instrument is required to distribute all its income currently for purposes of section 642(b) (relating to the personal exemption) and section 651 (relating to simple trusts). Thus, items such as dividends, interest, and rents are generally allocated to income and proceeds from the sale or exchange of trust assets are generally allocated to principal. However, an allocation of amounts between income and principal pursuant to applicable local law will be respected if local law provides for a reasonable apportionment between the income and remainder beneficiaries of the total return of the trust for the year, including ordinary and tax-exempt income, capital gains, and appreciation. For example, a state statute providing that income is a unitrust amount of no less than 3% and no more than 5% of the fair market value of the trust assets, whether determined annually or averaged on a multiple year basis, is a reasonable apportionment of the total return of the trust. Similarly, a state statute that permits the trustee to make adjustments between income and principal to fulfill the trustee’s duty of impartiality between the income and remainder beneficiaries is generally a reasonable apportionment of the total return of the trust. Generally, these adjustments are permitted by state statutes when the trustee invests and manages the trust assets under the state’s prudent investor standard, the trust describes the amount that may or must be distributed to a beneficiary by referring to the trust’s income, and the trustee after applying the state statutory rules regarding the allocation of receipts and disbursements to income and principal, is unable to administer the trust impartially. Allocations pursuant to methods prescribed by such state statutes for apportioning the total return of a trust between income and principal will be respected regardless of whether the trust provides that the income must be distributed to one or more beneficiaries or may be accumulated in whole or in part, and regardless of which alternate permitted method is actually used, provided the trust complies with all requirements of the state statute for switching methods. A switch between methods of determining trust income authorized by state statute will not constitute a recognition event for purposes of section 1001 and will not result in a taxable gift from the trust’s grantor or any of the trust’s beneficiaries. A switch to a method not specifically authorized by state statute, but valid under state law (including a switch via judicial decision or a binding non-judicial settlement) may constitute a recognition event to the trust or its beneficiaries for purposes of section 1001 and may result in taxable gifts from the trust’s grantor and beneficiaries, based on the relevant facts and circumstances. In addition, an allocation to income of all or a part of the gains from the sale or exchange of trust assets will generally be respected if the allocation is made either pursuant to the terms of the governing instrument and applicable local law, or pursuant to a reasonable and impartial exercise of a discretionary power granted to the fiduciary by applicable local law or by the governing instrument, if not prohibited by applicable local law. This section is effective for taxable years of trusts and estates ending after January 2, 2004.

[T.D. 9102, 69 FR 19, Jan. 2, 2004]

Eisner v. Macomber, 252 U.S. 189, 207, 40 S.Ct. 189, 9 A.L.R. 1570 (1920):

“In order, therefore, that the [apportionment] clauses cited from article I [§2, cl. 3 and §9, cl. 4] of the Constitution may have proper force and effect …[I]t becomes essential to distinguish between what is an what is not ‘income,’…according to truth and substance, without regard to form. Congress cannot by any definition it may adopt conclude the matter, since it cannot by legislation alter the Constitution, from which alone, it derives its power to legislate, and within those limitations alone that power can be lawfully exercised… [pg. 207]…After examining dictionaries in common use we find little to add to the succinct definition adopted in two cases arising under the Corporation Tax Act of 1909, Stratton’s Independence v. Howbert, 231 U.S. 399, 415, 34 S.Sup.Ct. 136, 140 [58 L.Ed. 285] and Doyle v. Mitchell Bros. Co., 247 U.S. 179, 185, 38 S.Sup.Ct. 467, 469, 62 L.Ed. 1054…”

[Eisner v. Macomber, 252 U.S. 189, 207, 40 S.Ct. 189, 9 A.L.R. 1570 (1920)]

Doyle v. Mitchell Brothers Co., 247 U.S. 179, 185, 38 S.Ct. 467 (1918):

“…Whatever difficulty there may be about a precise scientific definition of ‘income,’ it imports, as used here, something entirely distinct from principal or capital either as a subject of taxation or as a measure of the tax; conveying rather the idea of gain or increase arising from corporate activities.”

[Doyle v. Mitchell Brothers Co. , 247 U.S. 179, 185, 38 S.Ct. 467 (1918)]

Stratton’s Independence v. Howbert, 231 U.S. 399, 414, 58 L.Ed. 285, 34 Sup.Ct. 136 (1913)

“This court had decided in the Pollock Case that the income tax law of 1894 amounted in effect to a direct tax upon property, and was invalid because not apportioned according to populations, as prescribed by the Constitution. The act of 1909 avoided this difficulty by imposing not an income tax, but an excise tax upon the conduct of business in a corporate capacity, measuring, however, the amount of tax by the income of the corporation…Flint v. Stone Tracy Co., 220 U.S. 107, 55 L.Ed. 389, 31 Sup.Ct.Rep. 342, Ann. Cas.”

[Stratton’s Independence v. Howbert, 231 U.S. 399, 414, 58 L.Ed. 285, 34 Sup.Ct. 136 (1913)]

Commissioner v. Glenshaw Glass Co., 348 U.S. 426 (Supreme Court 1955)

“Here we have instances of undeniable accessions to wealth, clearly realized, and over which the taxpayers have complete dominion. The mere fact that the payments were extracted from the wrongdoers as punishment for unlawful conduct cannot detract from their character as taxable income to the recipients. Respondents concede, as they must, that the recoveries are taxable to the extent that they compensate for damages actually incurred. It would be an anomaly that could not be justified in the absence of clear congressional intent to say that a recovery for actual damages is taxable but not the additional amount extracted as punishment for the same conduct which caused the injury. And we find no such evidence of intent to exempt these payments.

[. . .]

It is conceded by the respondents that there is no constitutional barrier to the imposition of a tax on punitive damages. Our question is one of statutory construction: are these payments comprehended by § 22 (a)?

The sweeping scope of the controverted statute is readily apparent:

“SEC. 22. GROSS INCOME.

“(a) GENERAL DEFINITION.—`Gross income’ includes gains, profits, and income derived from salaries, wages, or compensation for personal service . . . of whatever kind and in whatever form paid, or from professions, vocations, trades, businesses, commerce, or sales, or dealings in property, whether real or personal, growing out of the ownership or use of or interest in such property; also from interest, rent, dividends, securities, or the transaction of any business carried on for gain or profit, or gains or profits and income derived from any source whatever. . . .” (Emphasis added.)[4]

This Court has frequently stated that this language was used by Congress to exert in this field “the full measure of its taxing power.” Helvering v. Clifford, 309 U. S. 331, 334; Helvering v. Midland Mutual Life Ins. Co., 300 U. S. 216, 223; Douglas v. Willcuts, 296 U. S. 1, 9; Irwin v. Gavit, 268 U. S. 161, 166. Respondents contend that punitive damages, characterized as “windfalls” flowing from the culpable conduct of third parties, are not within the scope of the section. But Congress applied no limitations as to the source of taxable receipts, nor restrictive 430*430 labels as to their nature. And the Court has given a liberal construction to this broad phraseology in recognition of the intention of Congress to tax all gains except those specifically exempted. Commissioner v. Jacobson, 336 U. S. 28, 49; Helvering v. Stockholms Enskilda Bank, 293 U. S. 84, 87-91. Thus, the fortuitous gain accruing to a lessor by reason of the forfeiture of a lessee’s improvements on the rented property was taxed in Helvering v. Bruun, 309 U. S. 461. Cf. Robertson v. United States, 343 U. S. 711; Rutkin v. United States, 343 U. S. 130; United States v. Kirby Lumber Co., 284 U. S. 1. Such decisions demonstrate that we cannot but ascribe content to the catchall provision of § 22 (a), “gains or profits and income derived from any source whatever.” The importance of that phrase has been too frequently recognized since its first appearance in the Revenue Act of 1913[5] to say now that it adds nothing to the meaning of “gross income.”

Nor can we accept respondent’s contention that a narrower reading of § 22 (a) is required by the Court’s characterization of income in Eisner v. Macomber, 252 U. S. 189, 207, as “the gain derived from capital, from labor, or from both combined.”[6] The Court was there endeavoring to determine whether the distribution of a corporate stock dividend constituted a realized gain to the shareholder, or changed “only the form, not the essence,” of 431*431 his capital investment. Id., at 210. It was held that the taxpayer had “received nothing out of the company’s assets for his separate use and benefit.” Id., at 211. The distribution, therefore, was held not a taxable event. In that context—distinguishing gain from capital—the definition served a useful purpose. But it was not meant to provide a touchstone to all future gross income questions. Helvering v. Bruun, supra, at 468-469; United States v. Kirby Lumber Co., supra, at 3.

Here we have instances of undeniable accessions to wealth, clearly realized, and over which the taxpayers have complete dominion. The mere fact that the payments were extracted from the wrongdoers as punishment for unlawful conduct cannot detract from their character as taxable income to the recipients. Respondents concede, as they must, that the recoveries are taxable to the extent that they compensate for damages actually incurred. It would be an anomaly that could not be justified in the absence of clear congressional intent to say that a recovery for actual damages is taxable but not the additional amount extracted as punishment for the same conduct which caused the injury. And we find no such evidence of intent to exempt these payments.

It is urged that re-enactment of § 22 (a) without change since the Board of Tax Appeals held punitive damages nontaxable in Highland Farms Corp., 42 B. T. A. 1314, indicates congressional satisfaction with that holding. Re-enactment—particularly without the slightest affirmative indication that Congress ever had the Highland Farms decision before it—is an unreliable indicium at best. Helvering v. Wilshire Oil Co., 308 U. S. 90, 100-101; Koshland v. Helvering, 298 U. S. 441, 447. Moreover, the Commissioner promptly published his nonacquiescence in this portion of the Highland Farms holding[7] and has, 432*432 before and since, consistently maintained the position that these receipts are taxable.[8] It therefore cannot be said with certitude that Congress intended to carve an exception out of § 22 (a)’s pervasive coverage. Nor does the 1954 Code’s[9] legislative history, with its reiteration of the proposition that statutory gross income is “all-inclusive,”[10] give support to respondent’s position. The definition of gross income has been simplified, but no effect upon its present broad scope was intended.[11] Certainly punitive damages cannot reasonably be classified as gifts, cf. Commissioner v. Jacobson, 336 U. S. 28, 47-52, nor do they come under any other exemption provision in the Code. We would do violence to the plain meaning of the statute and restrict a clear legislative attempt to 433*433 bring the taxing power to bear upon all receipts constitutionally taxable were we to say that the payments in question here are not gross income. See Helvering v. Midland Mutual Life Ins. Co., supra, at 223.

Reversed.

______________________

FOOTNOTES:

[11] In discussing § 61 (a) of the 1954 Code, the House Report states:

“This section corresponds to section 22 (a) of the 1939 Code. While the language in existing section 22 (a) has been simplified, the all-inclusive nature of statutory gross income has not been affected thereby. Section 61 (a) is as broad in scope as section 22 (a).

“Section 61 (a) provides that gross income includes `all income from whatever source derived.’ This definition is based upon the 16th Amendment and the word `income’ is used in its constitutional sense.” H. R. Rep. No. 1337, supra, note 10, at A18.

A virtually identical statement appears in S. Rep. No. 1622, supra, note 10, at 168.

[Commissioner v. Glenshaw Glass Co., 348 U.S. 426 (Supreme Court 1955)]

[EDITORIAL: SCOTUS uses the phrase “accession to wealth” in Glenshaw Glass as a synonym for a GAIN. SCOTUS in that case ruled that an award of exemplary damages is an accession to wealth and is therefore income, in contrast with COMPENSATORY damages which the SCOTUS recognized is NOT an accession to wealth but only restores the capital/makes the recipient whole, and is therefore NOT income. By the same logic, it is clear that compensation for ANYTHING is not a gain or an accession to wealth and is therefore NOT income.

If you read the Supreme Court’s Glenshaw Glass case, it’s obvious enough that Congress never intended (in the written law) for wages, salaries or compensation for labor/services to be construed as THEMSELVES constituting “gross income”; rather, section 22(a) of the 1939 IRC makes it obvious those things are only SOURCES from which income might be DERIVED.

And SCOTUS point outs in Glenshaw Glass that the rewording of that provision in IRC 61 had “no effect” on the meaning of “gross income”. It did not EXPAND the meaning of gross income nor place any new restrictions on it.

So even though the current IRC Section 61 makes it appear that “compensation for services” is itself included in “gross income” this is not the case! That provision must be construed in the light of the predecessor provision at section 22 of IRC, where compensation paid to the President of the United States or federal judges is specifically included in gross income. Only THAT compensation can be construed to ITSELF be included in “gross income”. See:

So the shell game “they” have played in court for many years is to misconstrue IRC Section 61 as including ALL compensation for services in “gross income”, when such construction is proper only in the case of compensation paid to the President and federal judges.

That’s why Congress chose to include “compensation for services” in the list of items at IRC section 61 but did not include “wages” or “salaries” in that list.

The compensation for services in that list means only compensation paid to POTUS or federal judges IF compensation is itself construed as “gross income”. Otherwise it can only be a SOURCE from which income is derived.These conclusions are consistent with the U.S. Supreme Court’s ruling in Southern Pacific v. Lowe, in which they held that gross income does NOT mean everything that comes in.]

President Taft letter to Congress on June 16, 1909 given to introduce the Sixteenth Amendment for ratification. Below is an excerpt from that speech:

I therefore recommend to the Congress that both Houses, by a two-thirds vote, shall propose an amendment to the Constitution conferring the power to levy an income tax upon the National Government without apportionment among the States in proportion to population.

…

Second, the decision in the Pollock case left power in the National Government to levy an excise tax, which accomplishes the same purpose as a corporation income tax and is free from certain objections urged to the proposed income tax measure.

I therefore recommend an amendment to the tariff bill Imposing upon all corporations and joint stock companies for profit, except national banks (otherwise taxed), savings banks, and building and loan associations, an excise tax measured by 2 per cent on the net income of such corporations. This is an excise tax upon the privilege of doing business as an artificial entity and of freedom from a general partnership liability enjoyed by those who own the stock. [Emphasis added] I am informed that a 2 per cent tax of this character would bring into the Treasury of the United States not less than $25,000,000.

The decision of the Supreme Court in the case of Spreckels Sugar Refining Company against McClain (192 U.S., 397), seems clearly to establish the principle that such a tax as this is an excise tax upon privilege and not a direct tax on property, and is within the federal power without apportionment according to population. The tax on net income is preferable to one proportionate to a percentage of the gross receipts, because it is a tax upon success and not failure. It imposes a burden at the source of the income at a time when the corporation is well able to pay and when collection is easy.

[President Taft letter to Congress on June 16, 1909 given to introduce the Sixteenth Amendment for ratification, SEDM Exhibit #02.001;

SOURCE: http://sedm.org/Exhibits/ExhibitIndex.htm ]

Merchants’ L. T. Co. v. Smietanka, 255 U.S. 509, 516-517 (1921)

“Section 2(a) of the Act of September 8, 1916 ( 39 Stat. 757; 40 Stat. 300, 307, § 212), applicable to the case, defines the income of “a taxable person” as including “gains, profits and income derived from . . . sales, or dealings in property, whether real or personal, growing out of the ownership or use of or interest in real or personal property, . . . or gains or profits and income derived from any source whatever.” Plainly the gain we are considering was derived from the sale of personal property, and, very certainly the comprehensive last clause “gains or profits and income derived from any source whatever,” must also include it, if the trustee was a “taxable person” within the meaning of the act when the assessment was made.”

[. . .]

“Further, § 2(c) clearly shows that it was the purpose of Congress to tax gains, derived from such a sale as we have here, in the manner in which this fund was assessed, by providing that “for the purpose of ascertaining the gain derived from the sale or other disposition of property, real, personal, or mixed, acquired before March first, nineteen hundred and thirteen, the fair market price or value of such property as of March first, nineteen hundred and thirteen, shall be the basis for determining the amount of such gain derived.””

[Merchants’ L. T. Co. v. Smietanka, 255 U.S. 509, 516-517 (1921)]

[EDITORIAL: Here is an interesting case from 1921 revealing that in the 1916 Revenue Act, Congress recognized that fair market value is a BASIS when selling any kind of personal property in order to determine the amount of GAIN]

Bowers v. Kerbaugh-Empire Co., 271 U.S. 170, 174, (1926)

“The Sixteenth Amendment declares that Congress shall have power to levy and collect taxes on income, “from [271 U.S. 174] whatever source derived,” without apportionment among the several states and without regard to any census or enumeration. It was not the purpose or effect of that amendment to bring any new subject within the taxing power. Congress already had power to tax all incomes. But taxes on incomes from some sources had been held to be “direct taxes” within the meaning of the constitutional requirement as to apportionment. Art. 1, § 2, cl. 3, § 9, cl. 4; Pollock v. Farmers’ Loan & Trust Co., 158 U.S. 601. The Amendment relieved from that requirement, and obliterated the distinction in that respect between taxes on income that are direct taxes and those that are not, and so put on the same basis all incomes “from whatever source derived.” Brushaber v. Union P. R. Co., 240 U.S. 1, 17. “Income” has been taken to mean the same thing as used in the Corporation Excise Tax Act of 1909, in the Sixteenth Amendment, and in the various revenue acts subsequently passed. Southern Pacific Co. v. Lowe, 247 U.S. 330, 335; Merchants’ L. & T. Co. v. Smietanka, 255 U.S. 509, 219. After full consideration, this Court declared that income may be defined as gain derived from capital, from labor, or from both combined, including profit gained through sale or conversion of capital. Stratton’s Independence v. Howbert, 231 U.S. 399, 415; Doyle v. Mitchell Brothers Co., 247 U.S. 179, 185; Eisner v. Macomber, 252 U.S. 189, 207. And that definition has been adhered to and applied repeatedly. See, e.g., Merchants’ L. & T. Co. v. Smietanka, supra; 518; Goodrich v. Edwards, 255 U.S. 527, 535; United States v. Phellis, 257 U.S. 156, 169; Miles v. Safe Deposit Co., 259 U.S. 247, 252-253; United States v. Supplee-Biddle Co., 265 U.S. 189, 194; Irwin v. Gavit, 268 U.S. 161, 167; Edwards v. Cuba Railroad, 268 U.S. 628, 633. In determining what constitutes income, substance rather than form is to be given controlling weight. Eisner v. Macomber, supra, 206. [271 U.S. 175]”

[Bowers v. Kerbaugh-Empire Co., 271 U.S. 170, 174, (1926)]

Pete Hendrickson on the Meaning of “Income” (MP3, 3 Mbytes)

U.S. v. Whiteridge, 231 U.S. 144, 34 S.Sup. Ct. 24 (1913)

“As repeatedly pointed out by this court, the Corporation Tax Law of 1909..imposed an excise or privilege tax, and not in any sense, a tax upon property or upon income merely as income. It was enacted in view of the decision of Pollock v. Farmer’s Loan & T. Co., 157 U.S. 429, 29 L. Ed. 759, 15 Sup. St. Rep. 673, 158 U.S. 601, 39 L. Ed. 1108, 15 Sup. Ct. Rep. 912, which held the income tax provisions of a previous law to be unconstitutional because amounting in effect to a direct tax upon property within the meaning of the Constitution, and because not apportioned in the manner required by that instrument.”

[U.S. v. Whiteridge, 231 U.S. 144, 34 S.Sup. Ct. 24 (1913)]

47A Corpus Juris Secundum (C.J.S.) Pages 182 through 189, Sections 56-58: Income Taxable In General (796 KBytes)

Brushaber v. Union Pacific Railroad Co., 240 U.S. 1, 16-17 (1916)

“The conclusion reached in the Pollack case.. recognized the fact that taxation on income was, in its nature, an excise…”

[Brushaber v. Union Pacific Railroad Co., 240 U.S. 1, 16-17 (1916)]

Southern Pacific Co., v. Lowe, 247 U.S. 330, 335, 38 S.Ct. 540 (1918)

“We must reject in this case, as we have rejected in cases arising under the Corporation Excise Tax Act of 1909 (Doyle, Collector, v. Mitchell Brothers Co., 247 U.S. 179, 38 Sup. Ct. 467, 62 L. Ed.–), the broad contention submitted on behalf of the government that all receipts—everything that comes in-are income within the proper definition of the term ‘gross income,’ and that the entire proceeds of a conversion of capital assets, in whatever form and under whatever circumstances accomplished, should be treated as gross income. Certainly the term “income’ has no broader meaning in the 1913 act than in that of 1909 (see Stratton’s Independence v. Howbert, 231 U.S. 399, 416, 417 S., 34 Sup. Ct. 136), and for the present purpose we assume there is not difference in its meaning as used in the two acts.”

[Southern Pacific Co., v. Lowe, 247 U.S. 330, 335, 38 S.Ct. 540 (1918)]

Bank of America Nat. T. S. Ass’n v. U.S., 459 F.2d. 513, 517-18 (Fed. Cir. 1972)

“There is consensus on certain basic principles, in addition to the rule that the United States notion of income taxes furnishes the controlling guide. All are agreed that an income tax is a direct tax on gain or profits, and that gain is a necessary ingredient of income. See Stratton’s Independence, Ltd. v. Howbert, 231 U.S. 399, 415, 34 S.Ct. 136, 58 L.Ed. 285 (1931); Brushaber v. Union Pacific R. R., 240 U.S. 1, 36 S.Ct. 236, 60 L.Ed. 493 (1916); Eisner v. Macomber, 252 U.S. 189, 207, 40 S.Ct. 189, 64 L.Ed. 521 (1920); Keasbey Mattison Co. v. Rothensies, 133 F.2d 894, 897 (C.A.3), cert. denied, 320 U.S. 739, 64 S.Ct. 39, 88 L.Ed. 438 (1943). Income, including gross income, must be distinguished from gross receipts which can cover returns of capital. Doyle v. Mitchell Bros. Co., 247 U.S. 179, 185, 38 S.Ct. 467, 62 L.Ed. 1054 (1918); Allstate Ins. Co. v. United States, 419 F.2d 409, 414, 190 Ct.Cl. 19, 27 (1969); 1 Mertens, Law of Federal Income Taxation, § 5.10 at 35-36 (1969). Only an “income tax”, not a tax which is truly on gross receipts, is creditable.”[Bank of America Nat. T. S. Ass’n v. U.S., 459 F.2d 513, 517-18 (Fed. Cir. 1972)]

Stapler v. U.S., 21 F.Supp. 737,U.S. Dist. Ct. EDPA (1937)

It follows that the value of buildings erected by a tenant is taxable to the landlord if it is “income” within the meaning of the Sixteenth Amendment, and therefore within the purview of the Revenue Act.

In the present case the new building was erected by the plaintiff’s tenant in 1933 and the income tax, which was imposed [**6] upon them with respect thereto for the year 1934, was computed under paragraph (c) of the regulation which authorized the lessor to report as income for each year of the lease an aliquot part of the estimated depreciated value of the buildings at the expiration of the lease. This paragraph, however, is obviously for the benefit of the taxpayer and must be held to be valid if the provisions of paragraph (b) are valid.

It follows, I think, that the sole question for consideration in this case is, as before stated, whether the value at the end of the lease of such a building erected by a lessee is income to the lessor in the year of erection within the meaning of the Sixteenth Amendment.

The Sixteenth Amendment authorizes the taxation without apportionment of “incomes, from whatever source derived.” Income has been defined as “the gain derived from capital, from labor, or from both combined,” Stratton’s Independence v. Howvert, 231 U.S. 399, 34 S.Ct. 136, 140, 58 L.Ed. 285, “including profit gained through sale or conversion of capital,” Doyle v. Mitchell Bros. Co., 247 U.S. 179, 38 S.Ct. 467, 62 L.Ed. 1054; Eisner v. Macomber, 252 U.S. 189, 40 S.Ct. 189, 193, 64 L.Ed. 521, 9 A.L.R. [**7] 1570. The gain is, however, not taxable until it is realized. North American Oil Consol. v. Burnet, 286 U.S. 417, 52 S.Ct. 613, 76 L.Ed. 1197. Furthermore, a gain from capital must be derived from it, not merely accruing to it. Eisner v. Macomber, supra. In the case just cited Mr. Justice Pitney, after quoting the foregoing definition, said, 252 U.S. 189, at page 207, 40 S.Ct. 189, 193, 64 L.Ed. 521, 9 A.L.R. 1570:

“Brief as it is, it indicates the characteristic and distinguishing attribute of income essential for a correct solution of the present controversy. The government, although basing its argument upon the definition as quoted, placed chief emphasis upon the word ‘gain,’ which was extended to include a variety of meanings; while the significance of the next three words was either overlooked or misconceived. ‘Derived — from — capital’; ‘the gain — derived — from — capital,’ etc. Here we have the essential matter: not a gain accruing to capital; not a growth or increment of value in the investment; but a gain, a profit, something of exchangeable value, proceeding from the property, severed from the capital, however invested or employed, and coming in, being ‘derived’ [**8] — that is, received or drawn by the recipient (the taxpayer) for his separate use, benefit and disposal — that is income derived from property. Nothing else answers the description.

“The same fundamental conception is clearly set forth in the Sixteenth Amendment — [*740] ‘incomes, from whatever source derived’ — the essential thought being expressed with a conciseness and lucidity entirely in harmony with the form and style of the Constitution.”

In the light of this authoritative definition I have reached the conclusion that the value of a building erected by a tenant on his own initiative and without any obligation to do so, which by reason of its being annexed to the freehold becomes the property of the landlord, is not income of the landlord until the land is sold or otherwise disposed of. I am not passing upon the question whether the value of such a building would be taxable income to the landlord if erected by the tenant pursuant to a definite obligation to do so contained in the lease. In such a case it might well be argued that the increased value of the leased premises represented an additional rental to the landlord which was reserved by him and agreed upon [**9] when the lease was executed. Such is not this case, however.

[Stapler v. U.S., 21 F.Supp. 737,U.S. Dist. Ct. EDPA (1937)]

Goodrich v. Edwards, 255 U.S. 527 (1921)

And the definition of ‘income’ approved by this Court is:

It is thus very plain that the statute imposes the income tax on the proceeds of the sale of personal property to the extent only that gains are derived therefrom by the vendor, and we therefore agree with the Solicitor General that since no gain was realized on this investment by the plaintiff in error no tax should have been assessed against him.

[Goodrich v. Edwards, 255 U.S. 527 (1921)]

N. Cal. Small Bus. Assistants Inc. v. Comm’r, 153 T.C. No. 4, at *29 n.14 (U.S.T.C. Oct. 23, 2019)

“If “‘income’ may be defined as the gain derived from capital, from labor, or from both combined”, Stratton’s Indep., Ltd. v. Howbert, 231 U.S. at 415 (emphasis added), then a business’s cost of labor should be no less deductible than its cost to acquire items it sells.”

[N. Cal. Small Bus. Assistants Inc. v. Comm’r, 153 T.C. No. 4, at *29 n.14 (U.S.T.C. Oct. 23, 2019)]

[EDITORIAL: Note that the Tax Court in 2019 is confirming that the definition of “income” as a gain from 100 years ago still stands.]

Gray v. Franchise Tax Board, 235 Cal.App.3d. 36, 42-43 (Cal.Ct.App. 1991)

“A gross income tax is distinguishable from a gross receipts tax because a return of capital is excluded from gross income, while gross receipts may include income as well as return of capital. (Robinson v. Franchise Tax Board (1981) 120 Cal.App.3d 72, 78, 174 Cal.Rptr. 437.) ”[Gray v. Franchise Tax Board, 235 Cal.App.3d 36, 42-43 (Cal.Ct.App. 1991)]

S.G. Borello & Sons, Inc. v. Dep’t of Indus. Relations, 48 Cal.3d. 341, 364 (Cal. 1989)

“These facts also demonstrate the majority’s error in stating that the sharefarmers make no investment in the enterprise. They invest the value of their labor. That may be insignificant to the majority but it is no doubt significant to the sharefarmers, as it is to me. The value of one’s labor is ultimately the source of all capital. Many generations of American immigrants have become successful entrepreneurs doing just that — investing the only asset at their command, the value of their labor.”

[S.G. Borello & Sons, Inc. v. Dep’t of Indus. Relations, 48 Cal.3d. 341, 364 (Cal. 1989)]

Commissioner of Int. Rev. v. Obear-Nester Glass, 217 F.2d. 56, 58 (7th Cir. 1954)

“Before the Sixteenth Amendment Congress could not levy a direct tax without apportionment among the states. Pollock v. Farmers’ Loan Trust Co., 157 U.S. 429, 15 S.Ct. 673, 39 L.Ed. 759, Id., 158 U.S. 601, 15 S.Ct. 912, 39 L.Ed. 1108. The Amendment allows a tax on “income” without apportionment, but an unapportioned direct tax on anything that is not income would still, under the rule of the Pollock case, be unconstitutional.”

[. . .]

The first question is: which definition of income is controlling, that of Congress or that of the Supreme Court? Since the judiciary is traditionally charged with the responsibility of interpreting the Constitution, we shall assume, for the purposes of this decision only, that, because the Sixteenth Amendment is limited to income, Congress may not tax directly without apportionment that which the Supreme Court does not so define.

The conflict centers around two different interpretations of the definition of income in Eisner v. Macomber, supra. In Central R. Co. of New Jersey v. Commissioner, 3 Cir., supra, the case upon which the nontaxability of punitive damages is based, the court treated the definition as if the Supreme Court had intended it to be all inclusive. Since the gain involved in that case did not fall within the definition it could not be income and was, therefore, not taxable. In General American Investors Co. v. Commissioner, 2 Cir., supra, the court thought that the Supreme Court did not intend that the definition be all inclusive. The court there admitted that the gain involved did not fall within the Eisner definition but it nevertheless held that it was taxable income.

60*60 In Eisner v. Macomber the Supreme Court was faced with the problem of distinguishing between a capital gain and income derived from capital. Having made the distinction the Court wanted to establish which was taxable and which was not. For this purpose it looked to a definition in Webster’s International Dictionary, which had already been repeated in two cases, that income was gain derived from capital or labor. The Court was not primarily interested in defining income according to its source, but wanted to show that income attributable to capital must be derived from capital, and, therefore, an increase in capital which could not be separated from it was not income. The borrowed definition served its purpose in separating the gain attributable to capital which was taxable as income from that which was not.

In Helvering v. Bruun, 309 U.S. 461, 60 S.Ct. 631, 84 L.Ed. 864, the Court refused to treat the Eisner v. Macomber definition as all inclusive. In that case a landlord was taxed for the increased value of repossessed land on which the tenant had put a building. Citing Eisner v. Macomber, 309 U.S. at pages 468-469, note 8, 60 S.Ct. at page 634, the Court said:

“* * * These expressions however, were used to clarify the distinction between an ordinary dividend and a stock dividend. They were meant to show that in the case of a stock dividend, the stockholder’s interest in the corporate assets after receipt of the dividend was the same as and inseverable from that which he owned before the dividend was declared. We think they are not controlling here.”

In James F. Waters, Inc., v. Commissioner of Internal Revenue, 9 Cir., 160 F.2d 596, 597, the court also interpreted the definition as covering only part of income.

“The final argument on this phase is that the insurance proceeds constitute an indemnification of the taxpayer for the loss of its president, and are not income within the intendment of the Sixteenth Amendment. Eisner v. Macomber [citation] is relied on as authority. While that decision has displayed an unexpected vitality within the limits of its particular facts, the lower federal courts would hardly be justified in extending its doctrine to wider fields.”

After Eisner v. Macomber the Board of Tax Appeals itself said in Hawkins v. Commissioner of Internal Revenue, 6 B.T.A. 1023, 1024:

“* * * Whether this description of income [the Eisner v. Macomber definition] is to be regarded as exclusive of everything not clearly within its terms, so that both the Sixteenth Amendment and the statute (which is said to be the fullest exercise of the constitutional power [citations]) are forever to be limited by a judicial definition, may still be doubtful, for the Supreme Court is not in the habit of defining words abstractly, but only for the purpose of determining whether the matter then under consideration comes within their fair intendment. * * * there may be cases in which taxable income will be judicially found although outside the precise scope of the description already given.”

In Magill, Taxable Income, at page 67, the author speaks of Eisner v. Macomber as “a futile attempt to confine a term that must remain elastic.” This criticism is justified only if the Court in that opinion intended that its definition be all encompassing.

We feel, as do the courts cited above, that the Supreme Court in Eisner v. Macomber was merely borrowing a definition of income to support its holding that income attributable to capital must come from it, i. e., be separately expendable, and that it did not consider that definition all encompassing. Even as to income derived from capital the Eisner case has been limited to its specific facts. Helvering v. Bruun, 309 U.S. 461, 60 S.Ct. 631, 84 L.Ed. 864; Koshland v. Helvering, 298 U.S. 441, 56 61*61 S.Ct. 767, 80 L.Ed. 1268. In Helvering v. Griffiths, 318 U.S. 371, 375, 63 S.Ct. 636, 639, 87 L.Ed. 843, the Court, speaking of the Koshland case, supra, said:

“She argued that her dividend, notwithstanding Eisner v. Macomber, to which she gave a narrow reading, was constitutionally taxable as income at the time received. The Court held unanimously and squarely that the dividend in question did constitute income within the Sixteenth Amendment, and in effect limited Eisner v. Macomber to the kind of dividend there dealt with.”

We do not believe that the Supreme Court intended to define income exclusively according to its source. The great argument which resulted in this country’s adoption of an income tax, and the fundamental principle upon which that tax is still based, is that individuals will be taxed according to their ability to pay. Cole v. Commissioner of Internal Revenue, 9 Cir., 81 F.2d 485, 487, 104 A.L.R. 420. See Mertens, Law of Federal Income Taxation, Section 1.03, especially note 38. There is no rational connection between the source of the taxpayer’s gain and his ability to pay. The question is: has he realized an economic gain, from whatever source, which leaves him better able to contribute to the support of his government?

Of course, gains from some sources are not taxable, but the reason is not that they do not constitute income, but rather that either the Constitution or Congress forbids the collection of the tax on income from those particular sources.

If gain not derived from capital or labor is excluded from taxation, the burden on income that is derived from these sources, will of course, be all the greater. We feel, as did the Court of Claims in Park & Tilford Distillers Corp. v. United States, 107 F.Supp. 941, 942, 123 Ct.Cl. 509, that: “If Congress were to select one kind of receipt of money which, above all others, would be a fair mark for taxation, it might well be `windfalls.'” There can be no question that the punitive damages recovered by the respondent here greatly enhanced its ability to pay. Realizing that one reason for the adoption of the Sixteenth Amendment was to place the burden of taxation according to the ability to pay, we cannot believe that the term “income” as used in that Amendment was not intended to include the type of gain involved here.

There can be little doubt that Congress intended to include the punitive damages, here involved, in income if it had the constitutional power to do so. Section 22(a) of the Internal Revenue Code provides:

“`Gross income’ includes gains, profits, and income derived from salaries, wages, or compensation for personal service * * * of whatever kind and in whatever form paid, or from professions, vocations, trades, businesses, commerce, or sales, or dealings in property, whether real or personal, growing out of the ownership or use of or interest in such property; also from interest, rent, dividends, securities, or the transaction of any business carried on for gain or profit, or gains or profits and income derived from any source whatever.” 26 U.S. C.A. § 22(a). (Emphasis added.)

The Supreme Court has said that Congress in defining “gross income” in Section 22(a) intended to use its taxing power to its fullest measure. Helvering v. Clifford, 309 U.S. 331, 337, 60 S.Ct. 554, 84 L.Ed. 788.

The respondent suggests that by allowing the taxation of treble damages awarded under the anti-trust acts, we would be defeating Congress’ attempt to encourage the prosecution of violators of these acts. The first answer to this contention is that once it is established that the award involved here is income and comes within the coverage of Section 22(a), Congress must specifically provide for its exclusion or deduction by statute if it so desires. We might further say that the principal purpose of treble damages seems to be punishment which will deter the violator and others from future illegal acts. Compensation 62*62 for actual damages is enough to encourage legal action, not to mention the substantial amount of punitive damages the injured party still retains after taxes are paid.

Respondent’s argument works against it, for if, as respondent suggests, punitive damages were intended principally to encourage the uncovering of antitrust violators, then it might be said that the taxpayer “earned” the punitive damages by prosecuting the action for the recovery. If this interpretation were made, the punitive damages here would fall within the Eisner v. Macomber definition as gain derived from labor.

We believe that the award involved here is included in “income” as used in the Sixteenth Amendment, and that Congress has covered it in Section 22(a) of the Internal Revenue Code.

The decision of the Tax Court is, therefore, reversed and the cause is remanded for further proceedings consistent with the views expressed in this opinion.

[Commissioner of Int. Rev. v. Obear-Nester Glass, 217 F.2d. 56, 58 (7th Cir. 1954)]

Conner v. United States, 303 F. Supp. 1187, 1190 (S.D. Tex. 1969)

“The language of section 61(a) of the Internal Revenue Code of 1954, set forth above, might at first glance appear to have broadened the definition of gross income by the omission of any reference to gain. This, however, is not so, because the Supreme Court had before it the then recently enacted 1954 Code of Internal Revenue when it decided Commissioner v. Glenshaw Glass Co., supra. It noted that, although the definition of gross income had been simplified, “no effect on its present broad scope was intended.” 348 U.S. 432, 75 S.Ct. 477. In addition, the Court in General American Investors Co. v. Commissioner of Internal Revenue, 348 U.S. 434, 75 S.Ct. 478, 99 L.Ed. 504 (1955), decided the same day as Glenshaw Glass Company, supra, held that “insider profits” under the Securities and Exchange Act of 1934 were includable in the recipient corporation’s gross income.”

Conner v. United States, 303 F. Supp. 1187, 1190 n.4 (S.D. Tex. 1969)

“I.R.C. (1939), section 22(a), is an example of what the drafting experts in the Office of the Legislative Council refer to as the “can of worms” school of drafting, whereas I.R.C. (1954), section 61(a) is an example of the “laundry list” school. See Mertens, Code Commentary, supra, p. 19.”

Conner v. United States, 303 F. Supp. 1187, 1191 (S.D. Tex. 1969)

“Income is nothing more nor less than realized gain. Shuster v. Helvering, 121 F.2d 643 (2nd Cir. 1941). It is not synonymous with receipts. 47 C.J.S. Internal Revenue § 98, p. 226.”

Conner v. United States, 439 F.2d. 974, 980-81 (5th Cir. 1971)

“We agree with the District Court that “there must be gain before there is income within the meaning of the sixteenth amendment”. We further agree that the receipt of these funds for the reasons and uses indicated represented no gain to these taxpayers and did not have to be reported as gross income for which there was no corresponding deduction. Eisner v. Macomber, 1919, 252 U.S. 189, 40 S.Ct. 189, 64 L.Ed. 521; Commissioner of Internal Revenue v. Glenshaw Glass Company, 1955, 348 U.S. 426, 75 S.Ct. 473, 99 L.Ed. 483; Commissioner of Internal Revenue v. Lo Bue, 1956, 351 U.S. 243, 76 S.Ct. 800, 100 L.Ed. 1142.”

Edwards v. Keith, 231 Fed 110:

“One does not derive income by rendering services and charging for them.”

[Edwards v. Keith, 231 Fed. 110]

Oliver v. Halstead, 196 Va. 992 (1955):

“The word “profit” is defined in Black’s Law Dictionary (3rd ed.) as “The advance in the price of goods sold beyond the cost of purchase. The gain made by the sale of produce or manufactures, after deducting the value of the labor, materials, rents, and all expenses, together with the interest of the capital employed.” There is a clear distinction between “profit” and “wages” or compensation for labor. “Compensation for labor can not be regarded as profit within the meaning of the law. The word ‘profit’, as ordinarily used, means the gain made upon any business or investment — a different thing altogether from mere compensation for labor.” The Commercial [***5] League Association of America v. The People ex rel. Thomas B. Needles, Auditor, 90 Ill. 166. “Reasonable compensation for labor or services rendered is not profit.” Laureldale Cemetery Association v. Matthews, 354 Pa. 239, 47 A.(2d) 277.”

[Oliver v. Halstead, 196 Va. 992 (1955)]

Laureldale Cemetery Assoc. v. Matthews, 354 Pa. 239 (1946), 47 A.2d. 277, 280

“The payment by the Association of salaries to its president, superintendent, and secretary afford no basis for denying exemption. The president receives, $2400, the superintendent $2600, and the secretary $1400 per [*244] annum. In each case the salary is in the same amount paid for the same work by Laureldale Cemetery Company, a shareholder’s company organized for profit, and considering the nature and extent of the Association’s business they are not excessive. Like wages paid the gravediggers such outlays are chargeable as necessary expenses incident to the proper maintenance of the cemetery. HN2 Reasonable compensation for labor or services rendered is not profit . To hold otherwise would be to nullify the exemption statute.“

[Laureldale Cemetery Assoc. v. Matthews, 354 Pa. 239 (1946), 47 A.2d. 277, 280]

Roberts v. Commissioner of Internal Revenue, 176 F.2d. 221, 225 (9th Cir. 1949)

“Treasury Regulations 111 defines “compensation for personal services” in this manner: “Sec. 29.22(a)-2. Compensation for Personal Services. Commissions paid salesmen, compensation for services on the basis of a percentage of profits, commissions on insurance premiums, tips * * *.

“The essential question for determination is whether tips are income. The Regulation just cited declares them such. Treasury Regulations, — unless in excess of authority, are binding upon the courts, especially if the provisions which they interpret were reenacted after their promulgation. Morrissey v. Commissioner, 1935, 296 U.S. 344, 56 S.Ct. 289, 80 L.Ed. 263; Coast Carton Co. v. Commissioner, 9 Cir., 1945, 149 F.2d 739. Of course, regulations “can add nothing to income as defined by Congress.” M.E. Blatt Co. v. United States, 1938, 305 U.S. 267, 279, 59 S.Ct. 186, 190, 83 L.Ed. 167.“

[. . .]

“In tipping, the financial advantage is conferred on the basis of a consideration which is related to service. This makes it clearly income.”

[Roberts v. Commissioner of Internal Revenue, 176 F.2d. 221, 225 (9th Cir. 1949)]

___________________________

[EDITORIAL: The court conveniently leaves out this part of the regulation

“…unless excluded by law”, which is what 26 U.S.C. 872 does in the case of Nonresident Aliens.

This is an interesting admission by the Court:

“Treasury Regulations, — unless in excess of authority, are binding upon the courts”

This regulation is in excess of authority if it is construed to make all tips INCOME, because there is no statute enacted by Congress that purports to make all tips INCOME.

Here is why this taxpayer lost his case:

“The petitioner challenges the regulation upon the ground that the tips are gifts under Section 22(b)(3) of the Internal Revenue Code, 26 U.S.C.A. § 22(b)(3).”

Tips do not have to be gifts in order to not be INCOME. By arguing they are gifts, he rested his whole case on this argument, which fails as a matter of law. Tips are not gifts. he was arguing for a statutory exclusion, when he did not NEED one

The court also stated:

“It may be conceded that, as a rule, a payment cannot, at the same time, be a gift and income. Bogardus v. Commissioner, 1937, 302 U.S. 34, 58 S.Ct. 61, 82 L.Ed. 32. However that norm is applicable only in case of genuine gifts. In Botchford v. Commissioner, 9 Cir., 1936, 81 F.2d 914, 110 A.L.R. 281, this court recognized the principle that additional compensation for past services may constitute taxable income. And this principle is generally recognized in other Circuits. These decisions make the determination dependent upon the circumstances surrounding each case. And generally, the courts insist that the essential characteristics of a gift, — absence of consideration — be present. Blair v. Rosseter, 9 Cir., 1929, 33 F.2d 286; Schumacher v. United States, 1932, 55 F.2d 1007, 74 Ct.Cl. 720; Weagant v. Bowers, 2 Cir., 1932, 57 F.2d 679; and see, Bass v. Hawley, 5 Cir., 1933, 62 F.2d 721, 732; Simpkinson v. Commissioner, 5 Cir., 1937, 89 F.2d 397, 399; Willkie v. Commissioner, 6 Cir., 1942, 127 F.2d 953, 955-956; Dasteel v. Rogan, 1941, D.C.Cal., 41 F. Supp. 836.”

Note the Court focuses on establishing tips are not gifts which is all it has to do to shoot down this petitioner’s argument it does not even have to say that tips are income, as the petitioner essentially conceded that tips ARE income if they are not found to be GIFTS.]

Murphy v. IRS, DC Court of Appeals No. 03cv02414

Murphy v. I.R.S, 460 F.3d. 79, 85 (D.C. Cir. 2006)

“ Broad though the power granted in the Sixteenth Amendment is, the Supreme Court, as Murphy points out, has long recognized “the principle that a restoration of capital [i]s not income; hence it [falls] outside the definition of `income’ upon which the law impose[s] a tax.” O’Gilvie, 519 U.S. at 84, 117 S.Ct. 452; see, e.g., Doyle v. Mitchell Bros. Co., 247 U.S. 179, 187-88, 38 S.Ct. 467, 62 L.Ed. 1054 (1918); S. Pac. Co. v. Lowe, 247 U.S. 330, 335, 38 S.Ct. 540, 62 L.Ed. 1142 (1918) (return of capital not income under IRC or Sixteenth Amendment). By analogy, Murphy contends a damage award for personal injuries — including nonphysical injuries — is not income but simply a return of capital — “human capital,” as it were. See Gary S. Becker, Human Capital (1st ed.1964); Gary S. Becker, “The Economic Way of Looking at Life,” 43-45 (Nobel Lecture, Dec. 9, 1992). ”

[. . .]

“ To be sure, the Supreme Court has broadly construed the phrase “gross income” in the IRC and, by implication, the word “incomes” in the Sixteenth Amendment, but it also has made plain that the power to tax income extends only to “gain[s]” or “accessions to wealth.” Glenshaw Glass, 348 U.S. at 430-31, 75 S.Ct. 473. That is why, as noted above, the Supreme Court has held a “return of capital” is not income. Doyle, 247 U.S. at 187, 38 S.Ct. 467; S. Pac. Co., 247 U.S. at 335, 38 S.Ct. 540. The question in this case is not, however, about a return of capital — except insofar as Murphy analogizes human capital to physical or financial capital; the question is whether the compensation she received for her injuries is income.[*]”

[Murphy v. I.R.S, 460 F.3d. 79, 85 (D.C. Cir. 2006)]

[EDITORIAL: This case originally held that proceeds for personal injury were not income. It was appealed in Murphy v. IRS, 493 F.3d 170 (2007) and the DC Circuit held that it WAS income because “. The taxpayer was taxed only after receiving a compensatory award, thus, it was akin to a duty upon the facilities made use of and actually employed in the transaction. The tax laid upon an award of damages for a nonphysical personal injury operated with “the same force and effect” throughout the United States and therefore was uniform under U.S. Const. art. I, § 8, cl. 1.” In other words, because the COURTS were used to obtain the damage award and they are PUBLIC rather than PRIVATE, then the award was a “benefit” in relation to the PUBLIC court and thus taxable as a privilege.

This case, however, very deviously AVOIDS the main issue, which is that statutory “gross income” under 26 U.S.C. §61 is already PRIVIELGED income and can be received ONLY by those lawfully engaged in the “trade or business” franchise, including statutory “U.S. persons” under 26 U.S.C. §7701(a)(30) and “nonresident aliens” engaged in a “trade or busienss” under 26 U.S.C. §871(b). Section 61 does not apply in the case of “nonresident aliens” NOT engaged in a “trade or business” under 26 U.S.C. §871(a). This is covered in:

Excluded Earnings, and People, Form #14.019, Section 3; https://sedm.org/Forms/14-PropProtection/ExcludedEarningsAndPeople.pdf]

Murphy v. I.R.S, 460 F.3d. 79, 87-88 (D.C. Cir. 2006)

“The Sixteenth Amendment simply does not authorize the Congress to tax as “incomes” every sort of revenue a taxpayer may receive. As the Supreme Court noted long ago, the “Congress cannot make a thing income which is not so in fact.” Burk-Waggoner Oil Ass’n v. Hopkins, 269 U.S. 110, 114, 46 S.Ct. 48, 70 L.Ed. 183 (1925). Indeed, because the “the power to tax involves the power to destroy,” McCulloch v. Maryland, 17 U.S. (4 Wheat.) 316, 431, 4 L.Ed. 579 (1819), it would not be consistent with our constitutional government, and the sanctity of property in our system, merely to rely upon the legislature to decide what constitutes income.”[Murphy v. I.R.S, 460 F.3d 79, 87-88 (D.C. Cir. 2006)]

United States v. Romero, 640 F.2d. 1014 (1981)

“Romero’s proclaimed belief that he was not a “person” and that the wages he earned as a carpenter were not “income” is fatuous as well as obviously incorrect. See Lucas v. Earl, 281 U.S. 111, 114-15, 50 S. Ct. 241, 74 L. Ed. 731 (1930); Roberts v. Commissioner, 176 F.2d 221, 225 (9th Cir. 1949); 26 U.S.C. § 61 (1976). The trial judge acted properly with respect to his comments and instructions regarding this matter of law. See United States v. Miller, 634 F.2d 1134 (8th Cir. 1980).

Romero received a fair trial. He based his defense on his proclaimed belief that the wages he earned were not taxable income and that he was not a person within the meaning of the income tax laws. At trial the judge properly instructed the jury on these matters of law. HN8 The jury’s function is to determine matters of fact. HN9 Compensation for labor or services, paid in the form of wages or salary, has been universally, held by the courts of this republic to be income, subject to the income tax laws [**8] currently applicable. We recognize that the tax laws bear heavily on all persons engaged in gainful activity, and recognize the right of a taxpayer to minimize his taxes by all lawful means. But Romero here is not attempting to minimize his taxes; instead he is attempting willfully and intentionally to shift his burden to his fellow workers by the use of semantics. He seems to have been inspired by various tax protesting groups across the land who postulate weird and illogical theories of tax avoidance, all to the detriment of the common weal and of themselves.”

[United States v. Romero, 640 F.2d. 1014 (1981)]

[EDITORIAL: This is often quoted obiter dicta, and it is 100% bullshit. This court does not cite even ONE court case that held that “compensation for services, paid in the form of wages or salary” is income]

So. Pacific v. Lowe, 238 F. 847, 247 U.S. 30(1918)(U.S. Dist. Ct. S.D. N.Y. 1917)

“… `income’ as used in the statute should be given a meaning so as not to include everything that comes in, the true function of the words `gains’ and `profits’ is to limit the meaning of the word `income'”

[So. Pacific v. Lowe, 238 F. 847, 247 U.S. 30 (1918)(U.S. Dist. Ct. S.D. N.Y. 1917)]

Eisner v. Macomber, 252 U.S. 189, 207, 40 S.Ct. 189, 9 A.L.R. 1570 (1920):

“… the definition of income approved by the Court is:

`The gain derived from capital, from labor, or from both combined, provided it be understood to include profits gained through sale or conversion of capital assets.'”

Helvering v. Edison Bros. Stores, 133 F.2d. 575 (1943)

“The Treasury Department cannot, by interpretative regulations, make income of that which is not income within the meaning of the revenue acts of Congress, nor can Congress, without apportionment, tax as income that which is not income within the meaning of the Sixteenth Amendment. Eisner v. Macomber, 252 U.S. 189, 40 S. Ct. 189, 64 L. Ed. 521, 9 A.L.R. 1570; M. E. Blatt Co. v. United States, 305 U.S. 267, 59 S. Ct. 186, 83 L. Ed. 167.”

[Helvering v. Edison Bros. Stores, 133 F.2d. 575 (1943)]

United States Glue Co. v. Town of Oak Creek, 247 U.S. 321 (1918)

“Corporations are allowed to make certain deductions from gross income, including amounts paid for personal services of officers and employees and other ordinary expenses paid out of income in the maintenance and operation of business and property, including a reasonable allowance for depreciation, losses not compensated for by insurance or otherwise, taxes, etc. These need not be further mentioned, beyond saying that the intent and necessary effect of the act is to tax not gross receipts but net income;”

[United States Glue Co. v. Town of Oak Creek, 247 U.S. 321, 324 (1918)][. . .]

“The difference in effect between a tax measured by gross receipts and one measured by net income, recognized by our decisions, is manifest and substantial, and it affords a convenient and workable basis of distinction between a direct and immediate burden upon the business affected and a charge that is only indirect and incidental.”

[United States Glue Co. v. Town of Oak Creek, 247 U.S. 321, 328 (1918)]

20 C.F.R. §416.1102: What is income

Income is anything you receive in cash or in kind that you can use to meet your needs for food, clothing, and shelter. Sometimes income also includes more or less than you actually receive (see § 416.1110 and § 416.1123(b)). In-kind income is not cash, but is actually food, clothing, or shelter, or something you can use to get one of these.

[56 F.R. 3212, Jan. 29, 1991]

20 C.F.R. §416.1103: What is not income

Some things you receive are not income because you cannot use them as food, clothing, or shelter, or use them to obtain food, clothing, or shelter. In addition, what you receive from the sale or exchange of your own property [and the Supreme Court in Butcher’s Union declared that labor is property] is not income; it remains a resource. The following are some items that are not income:

(a) Medical care and services. Medical care and services are not income if they are any of the following:

(1) Given to you free of charge or paid for directly to the provider by someone else;

(2) Room and board you receive during a medical confinement;

(3) Assistance provided in cash or in kind (including food, clothing, or shelter) under a Federal, State, or local government program, whose purpose is to provide medical care or services (including vocational rehabilitation);

(4) In-kind assistance (except food, clothing, or shelter) provided under a nongovernmental program whose purpose is to provide medical care or medical services;

(5) Cash provided by any nongovernmental medical care or medical services program or under a health insurance policy (except cash to cover food, clothing, or shelter) if the cash is either:

(i) Repayment for program-approved services you have already paid for; or

(ii) A payment restricted to the future purchase of a program-approved service.

Procedure for calculating taxable income:

1. The income tax is imposed on the “citizen” in 26 C.F.R. §1.1-1 on “worldwide income” of citizens “wherever resident”

2. HOWEVER, “wherever resident” does not mean ANYPLACE they physically are. Instead, it means wherever they have the CIVIL STATUS of “resident”. See:

Flawed Tax Arguments to Avoid, Form #-08.004, Section 8.20

https://sedm.org/Forms/08-PolicyDocs/FlawedArgsToAvoid.pdf3. See also section 8.24 of the above as well for proof that NOT EVERYTHING a citizen makes is subject to tax. It must instead originate from a taxable source.

4. Only income earned abroad to “citizens” or “residents” under 26 U.S.C. §911 is taxable or at home by “nonresidents” who are “aliens” if at home under 26 U.S.C. §871. Rev. Rul. 75-489.

5. Only be BEING abroad can a “citizen” or “resident” in fact BE a STATUTORY “individual”. See 26 U.S.C. §911(d)(2). In that capacity, they are called a “qualified individual”. Otherwise, they are NOT within the definition of statutory “individual” in 26 C.F.R. §1.1441-1(c)(3) [see SEDM Form #04.226]. Without being a statutory “individual“, they cannot be a statutory “person” under 26 U.S.C. §7701(a)(1) and hence would be outside the code and it would be impossible to be a “taxpayer”. See:

Policy Document: IRS Fraud and Deception About the Statutory Word “Person”, Form #08.023

https://sedm.org/Forms/08-PolicyDocs/IRSPerson.pdf6. Furthermore, they cannot have the civil statutory status of “citizen” without a domicile on federal territory and being born there under 8 U.S.C. §1401.

Why You are a Political Citizen but Civil Non-Citizen, National, and Nonresident Alien, Form #05.006

https://sedm.org/Forms/05-MemLaw/WhyANational.pdfIf they shift their domicile abroad, they have the right to politically and legally disassociate and become a nonresident with a foreign domicile. If they are DUMB enough at that point to call themselves a “citizen” like Cook did in Cook v. Tait, then they had better bend over. If they are smart and become a nonresident, they can keep everything they earn. See:

Why Domicile and Becoming a “Taxpayer” Require Your Consent, Form #05.002

https://sedm.org/Forms/05-MemLaw/Domicile.pdf7. The significance of Cook v. Tait is discussed in Sections 4.2 through 4.4 of the following:

Federal Jurisdiction, Form #05.018

https://sedm.org/Forms/05-MemLaw/FederalJurisdiction.pdf8. Statutory “income” is earned based on where services are performed, not where payment is made or sent. They must be performed abroad to be “income”. 26 C.F.R. §1.911-3(a)

https://www.law.cornell.edu/cfr/text/26/1.911-3There is NO definition of “income” that includes “DOMESTIC” income in the case of STATUTORY “citizens” or “residents”. Only foreign. So its not income if its earned at home by a “citizen” or a “resident”. Only “nonresidents” who are also “aliens” can earn domestic income under 26 U.S.C. §871. By “home” we mean the “United States” as defined in 26 U.S.C. §7701(a)(9) and (a)(10). Everything outside of that is “foreign” but not necessarily “abroad” under 26 U.S.C. §911. This is consistent with 26 C.F.R. §1.1441-1(d)(1) and TD8734, which says on the subject the following. Keep in mind that this Treasury Decision is the ENTIRE basis of 26 C.F.R. §1.1441-1:

“As a general matter, a withholding agent (whether U.S. or foreign) must ascertain whether the payee is a U.S. or a foreign person. If the payee is a U.S. person, the withholding provisions under chapter 3 of the Code do not apply; however, information reporting under chapter 61 of the Code may apply; further, if a TIN is not furnished in the manner required under section 3406, backup withholding may also apply. If the payee is a foreign person, however, the withholding provisions under chapter 3 of the Code apply instead. To the extent withholding is required under chapter 3 of the Code, or is excused based on documentation that must be provided, none of the information reporting provisions under chapter 61 of the Code apply, nor do the provisions under section 3406. If, however, withholding under chapter 3 of the Code does not apply irrespective of documentation (e.g., in the case of foreign source income or gross proceeds dealt with under section 6045), documentation may nevertheless have to be furnished to the withholding agent under the provisions of chapter 61 of the Code in order to be excused from Form 1099 information reporting and, possibly, from backup withholding under section 3406. Determinations of payee’s status are generally made at each level of the chain of payment, until, ultimately, the payment is made to the beneficial owner.”