FRIVOLOUS SUBJECT: “Wages” are taxable to a Nonresident Alien who does not VOLUNTARILY Effectively Connect

FALSE STATEMENT:

1. “Wages” are taxable to a Nonresident Alien who:

- Files the proper 1040NR.

- Does NOT VOLUNTEER to “Effectively Connect“.

- States under penalty of perjury with the tax return that any W-4 on file was submitted under duress and thus does NOT represent a 26 U.S.C. §3406(p) election of any kind. The following form does this:

W-2CC, Form #04.304

https://sedm.org/Forms/04-Tax/3-Reporting/FormW-2CC-Cust/FormW-2CC.pdf - Properly invokes the following authorities to exclude any reported “wages” on the W-2, since they are not paid USPI directly by the U.S. government:

3.1. 26 C.F.R. §31.3401(a)(6)-1(b) in the case of income tax.

3.2. 26 C.F.R. §31.3121(b)-3(c)(1) in the case of Social Security.

2. AND, if you filed a W-4 previously, you don’t have a choice about effectively connecting at filing time.

REBUTTAL:

1. “Wages” are ONLY “taxable” if you want them to be.

As we frequently point out on this website, “effectively connecting” is VOLUNTARY for American Nationals. See:

The Truth About “Effectively Connecting”, Form #05.056

https://sedm.org/Forms/05-MemLaw/EffectivelyConnected.pdf

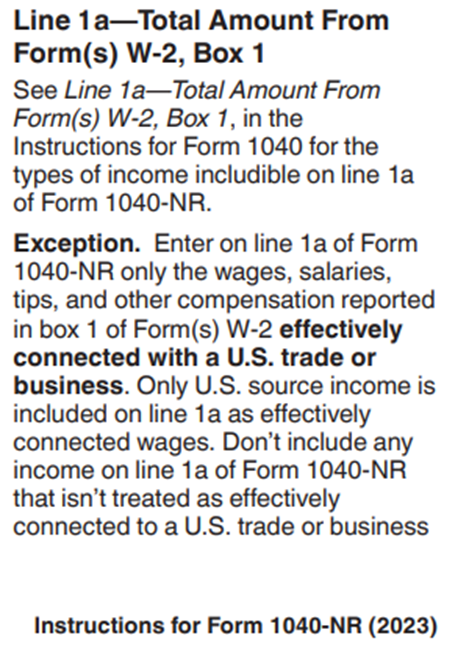

The above approach is EXACTLY what the IRS 1040NR instructions recommend in order to lawfully avoid paying tax on “wages”. The instructions say you HAVE to VOLUNTARILY “effectively connect” the “wages” reported on the W-2. They don’t TELL in the instructions that YOU get to choose to effectively connect and they can’t choose it FOR you in the case of American Nationals but in fact it IS if you file a 1040NR instead of a 1040:

SOURCE: https://www.irs.gov/instructions/i1040nr

The above notice in the 1040-NR instructions implements 26 U.S.C. §864(c)(1)(B). If you aren’t engaged in “trade or business within the United States,” and thus engaged in “personal services”, then under 26 U.S.C. §864(c)(1)(B), the only paragraphs that would apply to us are (6), (7), (8), and 26 U.S.C. §871(d). None of those provisions address “personal services” anyway, much less a W-4.

For the purposes of this website, “U.S. source” means USPI from the government, Not money paid to you by any PRIVATE person or entity. USPI must be involved in the case of American Nationals.

Why would IRS put the above warning on the 1040NR instructions if you COULD NOT do this?

There are LOTS of other reasons for this as well. The tax on “wages” is on “gross receipts”. The constitution forbids a “gross receipts” tax as a direct tax ONLY for those American Nationals standing on land protected by the constitution within the exclusive jurisdiction of a constitutional state. See:

- Constitutional taxation provisions 1:8:1, 1:9:4, 1:2:3, FTSIG

https://ftsig.org/history/constitutional-provisions-123-194/ - Microsoft Copilot: Is the income tax a DIRECT tax or an INDIRECT tax?, FTSIG

https://ftsig.org/microsoft-copilot-is-the-income-tax-a-direct-tax-or-an-indirect-tax/

Therefore, SOME kind of privilege is involved. That privilege is INVISIBLE to most people and NOT obvious to those filing the WRONG tax return: the 1040. This is done to keep you ENSLAVED to The Matrix by your own legal ignorance.

In the case of an American National filing a 1040NR, that privilege is ONLY “effectively connecting”, per the IRS’ OWN instructions for the 1040NR. This is also consistent with the definition of “personal services”, which means work performed in connection with a “trade or business”. See:

Authorities on “Personal services”, Family Guardian

https://famguardian.org/TaxFreedom/CitesByTopic/PersonalServices.htm

IRS has LOTS of propaganda on this subject such as the following:

The Truth About Frivolous Tax Arguments, Section B.1: Contention: Wages, tips and other compensation received for personal services are not income.

https://www.irs.gov/privacy-disclosure/the-truth-about-frivolous-arguments-section-i-a-to-c#contentionb1

What ALL of the above court cases have in common is the following:

- Filed a 1040 and thus usually unwittingly made a “U.S. person” election.

- Filed the 1040-NR but didn’t know they could avoid ECI by simply not entering it on the form per the IRS instructions.

- Didn’t file at all and later argued in court rather than just filing the correct return. Of course they are going to get CREAMED in court by doing this, because its done in presumption and ignorance and without evidence in their administrative record to prove compliance described at the beginning of this article.

There is not a SINGLE case they cite of someone who invoked the IRS’ OWN instructions and the proper Treasury Regulations indicated at the beginning of this article to LAWFULLY exclude “wages” from being entered on the 1040NR form. NOT ONE! Why would there ever even NEED to be? Do you think they want THAT kind of caselaw on the record showing people the exit door? It would probably go unpublished by the court so you never get the constitutionally required REASONABLE notice that your consent is required and HOW it is obtained!

The instructions and warnings about W-2 “wages” in the 1040NR Instructions are NOT found on the 1040 form instructions, however. This is because the filer is serving in a “U.S. Person” office that is the OWNER of the income, not the filer volunteering for the office. OF COURSE Uncle Sam can tax its own volunteer offices. It’s perfectly constitutional to do so. The problem is that:

- You are never FULLY informed that your CONSENT by ELECTION is obtained. Thus, the constitutional requirement for REASONABLE notice is violated and your consent is INVISIBLE. If everyone knew HOW they became volunteers, they would simply UNVOLUNTEER.

- Those mistakenly filing the 1040 form don’t know they are volunteers, so they think the system is behaving illegally when their own legal ignorance is the REAL problem.

- Judges HIDE this fact by not explaining that you CONSENTED and HOW you consented. The Declaration of Independence says that ALL JUST POWERS derive from CONSENT, but if the consent is invisible and never explicit, then government becomes inherently UNJUST.

Keep in mind also that many who work as “employees” often are given NO choice about whether to file the W-4 when they get hired. They are often threatened with being fired or not hired if they REFUSE to submit the W-4. For them, this procedure gives them a remedy at the time the file the return without having to worry about getting fired for doing so by their usually ignorant employer. The W-2CC, Form #04.304 above submitted at FILING time is the remedy for that.

Note that the FIRST income tax after the ratification of the Sixteenth Amendment in 1913 was the Tariff Act of 1913. That act was a tax on FOREIGN commerce including aliens but also upon DOMESTIC CIVIL CITIZENS by election. See:

Tariff Act of 1913, 38 State 114-203,

https://famguardian.org/PublishedAuthors/Govt/HistoricalActs/RevAct1913-38Stat114-203.pdf

The CIVIL citizen election codified in Sec. II, p. 166 of the above act later became the “U.S. person” election in 1962. The “effectively connected” election came MUCH later in Tax Reform Act of 1966, Public Law 89-809, enacted on November 13, 1966. TOGETHER, these two forms of election made the income tax an INTERNAL tax instead of only FOREIGN. Even then, your consent or election was required to allow that INTERNAL form of taxation.

- The “citizen of the United States” question was FIRST added to the 1921 tax return. That was the CIVIL citizen election that was the subject of the following case:

Cook v. Tait, 265 U.S. 47 (1924)

https://ftsig.org/cook-v-tait-265-u-s-47-1924/ - The “U.S. person” election first appeared in 1962 in Public Law 87-834, 76 Stat. 988, Section 7h. See:

“U.S. Person” Position, Form #05.053

https://sedm.org/Forms/05-MemLaw/USPersonPosition.pdf

You can learn more about the above in:

Tax Return History-Citizenship, Family Guardian Fellowship

https://famguardian.org/Subjects/Taxes/Citizenship/TaxReturnHistory-Citizenship/TaxReturnHistory-Citizenship.htm

If you want to know how this is done, see:

- 1040NR Attachment, Form #09.077

https://sedm.org/Forms/09-Procs/1040NR-Attachment.pdf - Procedure to File Returns Course, Form #09.075

https://sedm.org/product/procedure-to-file-tax-returns-form-09-075/ - How to File Returns, Form #09.074

https://sedm.org/product/filing-returns-form-09-074/

For a MUCH deeper treatment of the subject of this article, see:

Proof that Involuntary Income Taxes on Your labor are Slavery, Form #05.055

https://sedm.org/Forms/05-MemLaw/ProofIncomeTaxLaborSlavery.pdf

2. You can change your mind at the end of the year even with a W-4 on file

Remember: What you can convince the idiot employer to DO with your withholding paperwork and how you represent yourself in a tax filing are TWO COMPLETELY distinct and independent things. They don’t have to agree. The W-4 is never actually sent to the IRS ANYWAY. Its only there for the protection of the idiot employer.

Don’t pretend like your employer has to agree with your assessment or status or that you have to accept whatever the idiot malicious employer COMPELS you to declare on a government form. You can always claim duress or simply a change of mind. You own yourself. You’re not a victim. No excuses. Be a man.

We don’t care what IRS subjectively do without express delegated authority. We’re only interested in what the statutes and regulations authorize AFTER the status is volunteered for. Everything else is extortion and theft. The law cannot authorize theft and extortion and injustice with complete disregard for the requirement for consent. The Declaration of Independence declares that as the very definition of INJUSTICE.

The only person who can define what you earn as “wages” is YOU as the original, absolute, private owner. Only the owner can define ANYTHING that affects the property he or she owns. And you can change your mind at tax filing time if you want. Duress is voidable but not automatically void. Just point out the duress at filing time or simply withdraw your consent to call it “wages” as 26 U.S.C. §3402(p) authorizes. Even without duress, you can change your mind. See:

Using Form W-4 as a Nonresident Alien, FTSIG, Sections 2 and 7

https://ftsig.org/using-w-4-as-a-nonresident-alien/#7._Voluntary

No one else can define what you earn as PUBLIC “wagesPUB“. If they do, they are stealing and interfering with your control over absolutely owned, constitutionally protected PRIVATE property. YOU own yourself. And if you don’t, you’re a slave:

What is a “slave”?, SEDM

https://sedm.org/what-is-a-slave

If IRS in the executive branch tries to define it, they are illegally exercising legislative powers in violation of the separation of powers. They are usurping legislative powers reserved to congress and stealing property they don’t own. See:

Effect of Definitions Upon OWNERSHIP and CONTROL of Property, FTSIG

https://ftsig.org/how-you-volunteer/effect-of-definitions-upon-ownership-of-property/

Get real! Take some social responsibility for avoiding biblical harlotry and idolatrous state worship. Self-ownership and personal responsibility always go together. Injustice happens when they DON’T. Stop being a human sacrifice to “the BEAST” mainly out of fear, ignorance, laziness, and selfishness.

You’re NOT a victim, but you’re acting like one. Be a man.