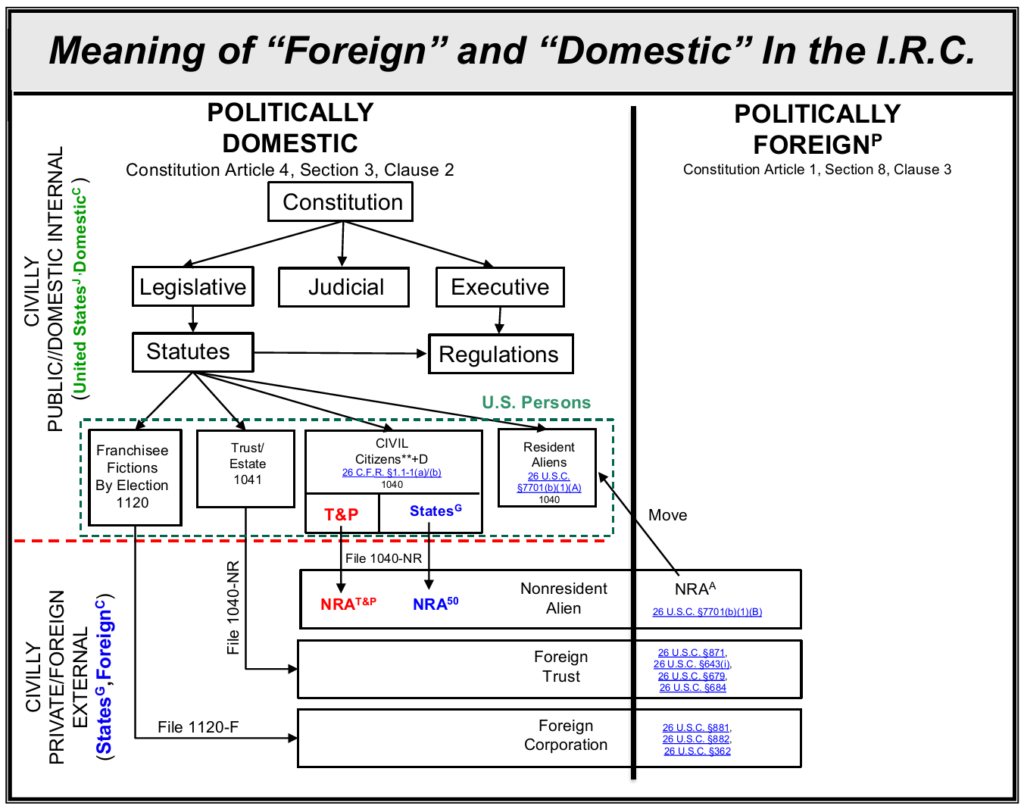

DEFINITIONS: “Foreign”

Writing Conventions On This Website

6. Foreign

There are TWO types of “foreign” you can be. Below is the symbology we use on this site for each:

- ForeignC=Civilly Foreign (private). CIVILLY FOREIGN=Foreign DOMICILE OUTSIDE the venue in question=Outside the “trade or business” excise taxable franchise. Not subject to federal preemption. Described but not defined in 26 C.F.R. §1.1441-1(c)(2)(ii). Governed exclusively by STATE and not FEDERAL law.

- ForeignS= ForeignC Sourced government payment under I.R.C. Subtitle A, Chapter 1, Subchapter N. Originating from government created and owned civil statutory entity or status=USPI=United StatesJ.

- ForeignP=POLITICALLY FOREIGN=Foreign NATIONALITY=Outside the COUNTRY under Article 1, Section 8, Clause 3 of the constitution. A matter of international affairs. Governed exclusively by the national government.

Note the central role of NATIONALITY and DOMICILE in determining what type of FOREIGN you are. We discuss the basis for each of these two components in:

Nationality v. Domicile, FTSIG

https://ftsig.org/civil-political-jurisdiction/two-statuses/nationality-v-domicile/

Below is a diagram of the relationship between POLITICALLY foreign and CIVILLY foreign:

How PROPERTY interacts with “foreign” PERSON status

- American nationals can ALWAYS make your person “foreign” by filing a 1040NR.

- Legislative control over PUBLIC PROPERTY DOES NOT automatically imply control over the PERSON in POSSESSION of said property. That control has to be acquired separately by a voluntary choice of domicile or a “U.S. person” election. Otherwise, they come under state law in accordance with 28 U.S.C. §1652 and Federal Rule of Civil Procedure 17. See:

Copilot: Limits of federal authority in states of the Union derived from Article 4, Section 3, Clause 2 jurisdiction and its affect on Constitutional/Private “persons”, FTSIG

https://ftsig.org/copilot-limits-of-federal-authority-in-states-of-the-union-derived-from-article-4-section-3-clause-2-jurisdiction-and-its-affect-on-constitutional-person/ - Mere receipt of a government payment does not automatically make the payment “effectively connected”. It takes more than that. Only the OWNER of the payment can do that, and not the PAYOR. Specifically:

3.1. CONSENT to effectively connect it voluntarily. You can’t do this for any of the things on the Schedule NEC, BTW. . .or

3.2. The government must NOTICE you of a reserved property interest in the payment AFTER you receive it. That’s what 26 U.S.C. §864(c)(6) does AFTER you effectively connect it YOURSELF previously in the case of a deferred payment. However, this cannot be done in a constitutional state, because the geographical United States does not expressly include the states of the Union so that there is no notice of extraterritoriality mandated under 4 U.S.C. §72, 28 U.S.C. §1652, Federal Rule of Civil Procedure 17, U.S. v. Bowman, 260 U.S. 94 (1922) and Foley Bros. v. Filardo, 336 U.S. 281 (1949). So it fails due process. - WARNING: “Effectively connecting” your PROPERTY UNAVOIDABLY makes YOU PUBLIC and a civil personPUB! See:

4.1. Establishing USPI thru laws of property, Section 2: The ORIGIN of PUBLIC/GOVERNMENT Property: “Domestic”/”trade or business within the United States”/”personal services”, FTSIG

https://ftsig.org/how-you-volunteer/establishing-uspi-thru-laws-of-property/#2._The

4.2. Nonresident Alien Position, Form #12.045, Section 25, p. 134:

https://sedm.org/LibertyU/NRA.pdf

The above are substantiated at:

PROOF OF FACTS: “Deferred earnings” paid in connection with government retirement earned as a “U.S. person” are not “foreign income” or taxable under I.R.C. 864(c), FTSIG

https://ftsig.org/proof-of-facts-deferred-retirement-earnings-not-taxable/

There are lots of reasons why the geographical “United States” defined at 26 U.S.C. §7701(a)(9) and (a)(10) and 4 U.S.C. §110(d) does not expressly include areas under the exclusive jurisdiction of the constitutional states and why Congress has no legislative authority to notice you of extraterritorial application of the income tax within states of the Union as a result:

- The Constitution does not authorize Congress to bestow any of the privileges or benefits that the income tax pays for so they can’t be offered there. This would:

1.1. Be a commercial invasion of the states in violation of Article 4, Section 4.

1.2. Violate the dual office prohibitions in state constitutions and state law.

1.3. Corrupt voters, jurists, and government officers with a criminal financial conflict of interest in violation of 18 U.S.C. §208, 28 U.S.C. §144, and 28 U.S.C. §455. - Congress cannot establish a trade or business in a state in order to tax it. License Tax Cases. The income tax is ONLY on this “trade or business” in fact.

- It’s never been the case that you can unilaterally elect yourself into a lawfully established public office managing property received OFF duty. That’s ridiculous and it would produce a de facto office. Preventing this from happening is EXACTLY what the declaration of independence was about:

“He has erected a multitude of New Offices, and sent hither swarms of Officers to harrass our people, and eat out their substance.”

De ja vu all over. The officers are called “taxpayers” and “U.S. persons”. To suggest that public offices and a “trade or business” can be authorized in a constitutional state is to violate the above. Given that states are not within the geographical definitions and there is no presence test for serving in said offices that would permit preemption to operate like there is with aliens (26 U.S.C. §7701(b)), possessions (26 U.S.C. §937), and abroad (26 U.S.C. §911).

TITLE 26 > Subtitle F > CHAPTER 79 > § 7701

(31) Foreign estate or trust

(A) Foreign estate The term “foreign estate” means an estate the income of which, from sources without the United States which is not effectively connected with the conduct of a trade or business within the United States, is not includible in gross income under subtitle A.

(B) Foreign trust The term “foreign trust” means any trust other than a trust described in subparagraph (E) of paragraph (30).

TITLE 26 > Subtitle F > CHAPTER 79 > § 7701

(5) Foreign

The term “foreign” when applied to a corporation or partnership means a corporation or partnership which is not domestic.

TITLE 26 > Subtitle B > CHAPTER 11 > Subchapter A > PART II > § 2014

§ 2014. Credit for foreign death taxes

(g) Possession of United States deemed a foreign country

For purposes of the credits authorized by this section, each possession of the United States shall be deemed to be a foreign country.

For all national purposes embraced by the Federal Constitution, the States and the citizens thereof are one, united under the same sovereign authority, and governed by the same laws. In all other respects the States are necessarily foreign and independent of each other.

[Buckner v. Finley, 2 Pet. 586 (1829)]

“as political communities, [are] distinct and sovereign, and consequently foreign to each other.”

[Bank of United States v. Daniel, 12 Pet. 32, 54 (1838)]

Foreign Laws:“The laws of a foreign country or sister state. In conflicts of law, the legal principles of jurisprudence which are part of the law of a sister state or nation. Foreign laws are additions to our own laws, and in that respect are called ‘jus receptum’.”

[Black’s Law Dictionary, 6th Edition, p. 647]

Foreign States:“Nations outside of the United States…Term may also refer to another state; i.e. a sister state.The term ‘foreign nations’, …should be construed to mean all nations and states other than that in which the action is brought; and hence, one state of the Union is foreign to another, in that sense.”

[Black’s Law Dictionary, 6th Edition, p. 648]

Sir William Blackstone, in his commentaries(a), distinguishes foreign from inland bills, by defining the former as bills drawn by a merchant residing abroad upon his correspondent in England, or vice versa; and the latter as those drawn by one person on another, when both drawer and drawee reside within the same kingdom. Chitty, p. 16, and the other writers(b) on bills of exchange are to the same effect; and all of them agree, that until the statutes of 8 and 9 W. III. ch. 17, and 3 and 4 Anne, ch. 9, which placed these two kinds of bills upon the same footing, and subjected inland bills to the same law and custom of merchants which governed foreign bills; the latter were much more regarded in the eye of the law than the former, as being thought of more public concern in the advancement of trade and commerce.

Applying this definition to the political character of the several states of this union in relation to each other, we are all clearly of opinion, that bills drawn in one of these states, upon persons living in any other of them, partake of the character of foreign bills, and ought so to be treated. For all national purposes embraced by the federal constitution, the states and the citizens thereof are one, united under the same sovereign authority, and governed by the same laws. In all other respects, the states are necessarily foreign to, and independent of each other. Their constitutions and forms of government being, although republican, altogether different, as are their laws and institutions. This sentiment was expressed, with great force, by the president of the court of appeals of Virginia, in the case of Warder vs. Arrell, 2 Wash. 298; where he states, that in cases of contracts, the laws of a foreign country, where the contract was made, must govern; and then adds as follows—’The same principle applies, though with no greater force, to the different states of America; for though they form a confederated government, yet the several states retain their individual sovereignties, and, with respect to their municipal regulations, are to each other foreign.’

[William Buckner Citizen of New York v. Finley and Van Lear, Citizens of the State of Maryland, 27 U.S. 586, 2 Pet. 586, 7 L.Ed. 528 (1829)]

“For all national purposes embraced by the Federal Constitution, the states and citizens thereof are one, united under the same sovereign authority, and governed by the same laws. In all other respects, the states are necessarily foreign to and independent of each other.” They are each governed by their own lanws, and their courts having no extraterritorial power to enforce the decrees beyond theyr jurisdictional limits, they are in that sense foreign to each other, which is the clear and settled doctrine of the common law.

[Smith v. Lathrop, 44 Pa. 326 (1863)]