PROOF OF FACTS: Authorities on Privileges and Benefits

TABLE OF CONTENTS:

- Definition

- Memorandums of Law

- Power to regulate and tax predicated on receipt of a privilege or benefit

- Person Offering is the “Merchant” and those Accepting are the “Buyer”

4.1. Outline

4.2. An OFFER requires REAL CONSIDERATION, which in the context of government privileges means GOVERNMENT/PUBLIC property

4.3. The ability to take “deductions” against money that was NEVER taxable to begin with because it is EXCLUDED rather than EXEMPTED is NOT “real consideration”

4.4. Receiving your OWN money back as PRIVATE PROPERTY as part of a tax refund that was wrongfully withheld and paid is not REAL consideration or a privilege

4.5. More on this subject - Acceptance by “Buyer”

5.1. ACCEPTANCE OCCURS BY INVOKING THE BENEFITS OF THE CIVIL STATUS ELIGIBLE FOR THE PRIVILEGE

5.2. VOLUNTARY Acceptance creates a “quasi contract”

5.3. Result of VOLUNTARY ACCEPTANCE is you become “federal personnel”

5.4. Result of VOLUNTARY ACCEPTANCE is that you satisfy the MINIMUM CONTACTS DOCTRINE of the U.S. Supreme Court

5.5. In BIBLICAL terms, the ACCEPTANCE of the privilege or benefit is defined as “playing the harlot” - Acceptance is the Origin of the Power to Enforce

6.1. The main source of civil jurisdiction of Congress is the ability write “all needful rules” to regulate its own property

6.2. Only by accepting government/public property that retains its government ownership while in your possession or “benefit” do you become the proper target of CIVIL legislation

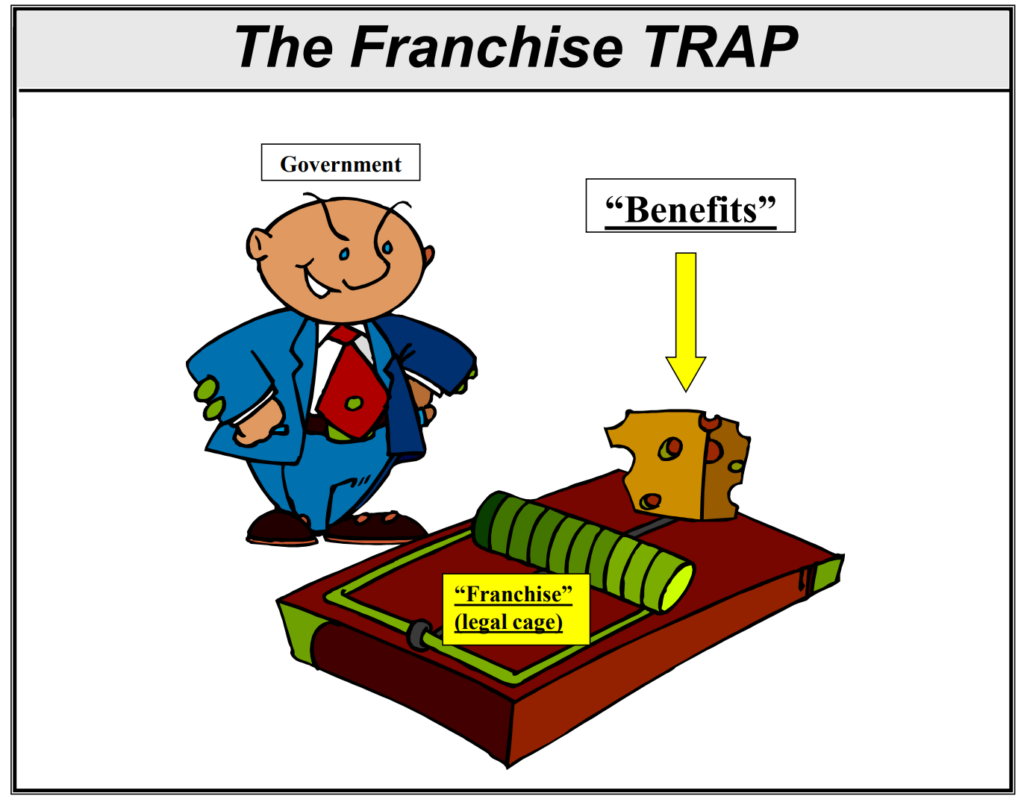

6.3. The clearest, most succinct evidence of the fact that government franchises and the “benefits” (meaning PROPERTY) they confer are the source of the loss of your rights is found in the following authorities - Enforcement of Obligations Attached to the Privilege Cannot Produce Unjust Enrichment by the Government

- Requirement to Pay For

- Right to Refuse Benefit

- Civil Statutory Law is a Privilege You Can Avoid

- Your Equal Right to Use Privileges Against the Government

- Supreme Court Doctrines that Implement Privileges and Benefits

- How to Reject All Privileges in a Tax Return Filing

- THE problem with FEDERAL privileges within the CONSTITUTIONAL states

- PRIVILEGES in a NUTSHELL

“Make it your ambition to lead a quiet life, to mind your own business and to work with your hands, just as we told you, so that your daily life may win the respect of outsiders and so that you will not be dependent on anybody.”

[1 Thess. 4:9-12, Bible, NIV]People of all races, genders, political beliefs, sexual orientations, and nearly all religions are welcome here. All are treated equally under REAL “law”. The only way to remain truly free and equal under the civil law is to avoid seeking government civil services, benefits, property, special or civil status, exemptions, privileges, or special treatment. All such pursuits of government services or property require individual and lawful consent to a franchise and the surrender of inalienable constitutional rights AND EQUALITY in the process, and should therefore be AVOIDED. The rights and equality given up are the “cost” of procuring the “benefit” or property from the government, in fact. Nothing in life is truly “free”. Anyone who claims that such “benefits” or property should be free and cost them nothing is a thief who wants to use the government as a means to STEAL on his or her behalf. All just rights spring from responsibilities/obligations under the laws of a higher power. If that higher power is God, you can be truly and objectively free. If it is government, you are guaranteed to be a slave because they can lawfully set the cost of their property as high as they want as a Merchant under the U.C.C. If you want it really bad from people with a monopoly, then you will pay dearly for the privilege. There are NO constitutional limits on the price government can charge for their monopoly services or property. Those who want no responsibilities can have no real/PRIVATE rights, but only privileges dispensed to wards of the state which are disguised to LOOK like unalienable rights. Obligations and rights are two sides of the same coin, just like self-ownership and personal responsibility. For the biblical version of this paragraph, read 1 Sam. 8:10-22. For the reason God answered Samuel by telling him to allow the people to have a king, read Deut. 28:43-51, which is God’s curse upon those who allow a king above them. Click Here for a detailed description of the legal, moral, and spiritual consequences of violating this paragraph.

[FTSIG]

1. DEFINITION

Understanding privileges and how to avoid them is the most important subject covered on this website. You have a right to avoid privileges and the obligations that go with them. The I.R.C. Subtitle A income tax is such a privilege and an indirect excise tax. This has been admitted by the U.S. SUpreme court but the IRS refuses to publicly give you reasonable notice of what the privilege is and how to avoid it, as described in:

Copilot: IRS Misrepresentation of Income Tax as NOT an excise and refusal to recognize the activity subject to tax and how to unvolunteer, FTSIG

https://ftsig.org/copilot-irs-misrepresentation-of-income-tax-as-not-an-exise/

Below are authorities describing what a “privilege” is.

1.1. Sovereignty Forms and Instructions Online, Form #10.004, Cites by Topic: “privilege”

https://famguardian.org/TaxFreedom/CitesByTopic/privilege.htm

1.2. Sovereignty Forms and Instructions Online, Form #10.004, Cites by Topic: “franchise”

https://famguardian.org/TaxFreedom/CitesByTopic/franchise.htm

1.3. U.S. Code

TITLE 5 > PART I > CHAPTER 5 > SUBCHAPTER II > § 552a

§ 552a. Records maintained on individuals(a) Definitions.— For purposes of this section—

(12) the term “Federal benefit program” means any program administered or funded by the Federal Government, or by any agent or State on behalf of the Federal Government, providing cash or in-kind assistance in the form of payments, grants, loans, or loan guarantees to individuals;. . .

1.4. Black’s Law Dictionary

Benefit. Advantage; profit; fruit; privilege; gain; interest. The receiving as the exchange for promise some performance or forbearance which promisor was not previously entitled to receive. Graphic Arts Finishers, Inc. v. Boston Redevelopment Authority, 357 Mass. 49, 255 N.E.2d. 793, 795. Benefits are something to advantage of, or profit to, recipient. Cheltenham Tp. V. Cheltenham Tp. Police Dept., 11 Pa.Cmwlth. 348, 312 A.2d. 835, 838.

Financial assistance received in time of sickness, disability, unemployment, etc. either from insurance or public programs such as social security.

Contracts. When it is said that a valuable consideration for a promise may consist of a benefit to the promisor, “benefit” means that the promisor has, in return for his promise, acquired some legal right to which he would not otherwise have been entitled. Woolum v. Sizemore, 267 Ky. 384, 102 S.W.2d. 323, 324. “Benefits” of contract are advantages which result to either party from performance by other. DeCarlo v. Geryco, Inc. 46 N.C. App. 15, 264 S.E.2d. 370, 375.

Eminent domain. It is a rule that, in assessing damages for private property taken or injured for public use, “special benefits” may be set off against the amount of damage found, but not “general benefits,” Within the meaning of this rule, general benefits are such as accrue to the community at large, to the vicinage, or to all property similarly situated with reference to the work or improvement in question; while special benefits are such as accrue directly and solely to the owner of the land in question and not to others.

As respects eminent domain law, “general benefits” are those which arise from the fulfillment of the public object which justified the taking, while “special benefits” are those which arise from the particular relation of the land in question to the public improvement. Morehead v. State Dept. of Roads, 195 Neb. 31, 236 N.W.2d. 623, 627.

[Black’s Law Dictionary, Sixth Edition, p. 158]

2. MEMORANDUMS OF LAW

- Government Franchises Course, Form #12.012

SLIDES: https://sedm.org/LibertyU/GovFranchises.pdf

VIDEO: http://youtu.be/vnDcauqlbTQ - Government Instituted Slavery Using Franchises, Form #05.030

https://sedm.org/Forms/05-MemLaw/Franchises.pdf - The Government “Benefits” Scam, Form #05.040** (Member Subscriptions)

https://sedm.org/product/the-government-benefits-scam-form-05-040/ - Why the Government is the Only Real Beneficiary of All Government Franchises, Form #05.051** (Member Subscriptions)

https://sedm.org/product/why-the-government-is-the-only-real-beneficiary-of-all-government-franchises-form-05-051/

3. POWER TO REGULATE AND TAX PREDICATED ON RECEIPT OF A PRIVILEGE OR BENEFIT

“The power of taxation, indispensable to the existence of every civilized government, is exercised upon the assumption of an equivalent rendered to the taxpayer in the protection of his person and property, in adding to the value of such property, or in the creation and maintenance of public conveniences in which he shares, such, for instance, as roads, bridges, sidewalks, pavements, and schools for the education of his children. If the taxing power be in no position to render these services, or otherwise to benefit the person or property taxed, and such property be wholly within the taxing power of another State, to which it may be said to owe an allegiance and to which it looks for protection, the taxation of such property within the domicil of the owner partakes rather of the nature of an extortion than a tax, and has been repeatedly held by this court to be beyond the power of the legislature and a taking of property without due process of law. Railroad Company v. Jackson, 7 Wall. 262; State Tax on Foreign-held Bonds, 15 Wall. 300; Tappan v. Merchants’ National Bank, 19 Wall. 490, 499; Delaware &c. R.R. Co. v. Pennsylvania, 198 U.S. 341, 358. In Chicago &c. R.R. Co. v. Chicago, 166 U.S. 226, it was held, after full consideration, that the taking of private property 203*203 without compensation was a denial of due process within the Fourteenth Amendment. See also Davidson v. New Orleans, 96 U.S. 97, 102; Missouri Pacific Railway v. Nebraska, 164 U.S. 403, 417; Mount Hope Cemetery v. Boston, 158 Massachusetts, 509, 519.

[. . .]

But notwithstanding the rule of uniformity lying at the basis of every just system of taxation, there are doubtless many individual cases where the weight of a tax falls unequally upon the owners of the property taxed. This is almost unavoidable under every system of direct taxation. But the tax is not rendered illegal by such discrimination. Thus every citizen is bound to pay his proportion of a school tax, though he have no children; of a police tax, though he have no buildings or personal property to be guarded; or of a road tax, though he never use the road. In other words, a general tax cannot be dissected to show that, as to certain constituent parts, the taxpayer receives no benefit. Even in case of special assessments imposed for the improvement of property within certain limits, the fact that it is extremely doubtful whether a particular lot can receive any benefit from the improvement does not invalidate the tax with respect to such lot. Kelly v. Pittsburgh, 204*204 104 U.S. 78; Amesbury Nail Factory Co. v. Weed, 17 Massachusetts, 53; Thomas v. Gay, 169 U.S. 264; Louisville &c. R.R. Co. v. Barber Asphalt Co., 197 U.S. 430. Subject to these individual exceptions, the rule is that in classifying property for taxation some benefit to the property taxed is a controlling consideration, and a plain abuse of this power will sometimes justify a judicial interference. Norwood v. Baker, 172 U.S. 269. It is often said protection and payment of taxes are correlative obligations.

[Union Refrigerator Transit Co. v. Kentucky, 199 US 194 (1905);

SOURCE: https://scholar.google.com/scholar_case?case=14163786757633929654]

“As was said in Wisconsin v. J. C. Penney Co., 311 U.S. 435, 444 (1940), “[t]he simple but controlling question is whether the state has given anything for which it can ask return.”

[Colonial Pipeline Co v Traigle, 421 U.S. 100, 109 (1975); SOURCE: https://scholar.google.com/scholar_case?case=16559630216409245512]

“Cujus est commodum ejus debet esse incommodum.

He who receives the benefit should also bear the disadvantage.”“Que sentit commodum, sentire debet et onus.

He who derives a benefit from a thing, ought to feel the disadvantages attending it. 2 Bouv. Inst. n. 1433.”[Bouvier’s Maxims of Law, 1856;

SOURCE: http://famguardian.org/Publications/BouvierMaximsOfLaw/BouviersMaxims.htm]

“When Sir Matthew Hale, and the sages of the law in his day, spoke of property as affected by a public interest, and ceasing from that cause to be juris privati solely, that is, ceasing to be held merely in private right, they referred to

[1] property dedicated [DONATED] by the owner to public uses, or

[2] to property the use of which was granted by the government [e.g. Social Security Card], or

[3] in connection with which special privileges were conferred [licenses].

Unless the property was thus dedicated [by one of the above three mechanisms], or some right bestowed by the government was held with the property, either by specific grant or by prescription of so long a time as to imply a grant originally, the property was not affected by any public interest so as to be taken out of the category of property held in private right.”

[Munn v. Illinois, 94 U.S. 113, 139-140 (1876);

SOURCE: https://scholar.google.com/scholar_case?case=6419197193322400931]

4. PERSON OFFERING IS THE “MERCHANT” AND THOSE ACCEPTING ARE THE “BUYER”

- Person offering is the “Merchant”/Creditor under U.C.C. §2-104(1).

- Person accepting is the “Buyer”/Debtor under U.C.C. §2-103(1)(a).

- The ONLY party who normally makes all the rules relating to their relationship is the Merchant. They must obey you and not the other way around.

- You NEVER want to be a Buyer and always want to be a Merchant in relation to government.

“All subjects over which the sovereign power of a state extends, are objects of taxation; but those over which it does not extend, are, upon the soundest principles, exempt from taxation… The sovereignty of a state extends to everything which exists by its own authority, or is introduced by its permission;”.

[McCulloch v. Maryland, 17 U. S. 316, 209-210 (1819); SOURCE: https://scholar.google.com/scholar_case?case=9272959520166823796EDITORIAL: You need PERMISSION from the state to use or benefit from PUBLIC property]

“As was said in Wisconsin v. J. C. Penney Co., 311 U.S. 435, 444 (1940), “[t]he simple but controlling question is whether the state has given anything for which it can ask return.”

[Colonial Pipeline Co v Traigle, 421 U.S. 100, 109 (1975); SOURCE: https://scholar.google.com/scholar_case?case=16559630216409245512]

- The Truth About “Effectively Connecting“, Form #05.056

https://sedm.org/Forms/05-MemLaw/EffectivelyConnected.pdf - Excluded Earnings and People, Form #14.019

https://sedm.org/Forms/14-PropProtection/ExcludedEarningsAndPeople.pdf

The United States, we have held, cannot, as against the claim of an innocent party, hold his money which has gone into its treasury by means of the fraud of its agent. While here the money was taken through mistake without element of fraud, the unjust retention is immoral and amounts in law to a fraud of the taxpayer’s rights. What was said in the State Bank Case applies with equal force to this situation. ‘An action will lie whenever the defendant has received money which is the property of the plaintiff, and which the defendant is obligated by natural justice and equity to refund. The form of the indebtedness or the mode in which it was incurred is immaterial.

[Bull v. United States, 295 U.S 247, 261, 55 S.Ct. 695, 700, 79 L.Ed. 1421;

SOURCE: https://scholar.google.com/scholar_case?case=16468645332325230169]

When the Government has illegally received money which is the property of an innocent citizen and when this money has gone into the Treasury of the United States, there arises an implied contract on the part of the Government to make restitution to the rightful owner under the Tucker Act and this court has jurisdiction to entertain the suit.

90 Ct.Cl. at 613, 31 F.Supp. at 769.

It does not follow, however, that there is a contract implied in fact where, as now, a nontaxpayer may recover property improperly levied upon through timely suit in the district court. In this situation it seems unlikely that the government also has agreed to make restitution to the nontaxpayer under an implied contract, which may be sued upon in this court. An important reason for the Kirkendall decision, although not explicitly set forth in the opinion, would appear to be that unless there were such a contract implied in fact, there might be no method by which the nontaxpayer effectively could recover the property the government improperly had taken from him through a levy. With the enactment of section 110(a), however, that situation no longer exists. Cf. Fletcher v. United *847 States, Ct.Cl. No. 572-79T, order entered December 31, 1980.

In view of our disposition of this case, there is no occasion here to reach this issue, which neither party has addressed. I discuss it only because it seems important to point out that, if and when the court faces the issue, it may conclude that Kirkendall no longer is viable.[Gordon v. U. S., 227 Ct.Cl. 328, 649 F.2d 837 (Ct.Cl., 1981);

SOURCE: https://scholar.google.com/scholar_case?case=2766905623968774369]

- Government Instituted Slavery Using Franchises, Form #05.030, Section 2.5

https://sedm.org/Forms/05-MemLaw/Franchises.pdf - Path to Freedom, Form #09.015, Sections 5.6 and 5.7

https://sedm.org/Forms/FormIndex.htm

5. ACCEPTANCE BY “BUYER”

5.1. ACCEPTANCE OCCURS BY INVOKING THE BENEFITS OF THE CIVIL STATUS ELIGIBLE FOR THE PRIVILEGE

“In other words, the principle was declared that the government, by its very nature, benefits the [person who ELECTS the CIVIL STATUTORY FRANCHISE STATUS OF] citizen [on a 1040 Tax form like Cook did] and his property wherever found and, therefore, has the power to make the benefit complete. Or to express it another way, the basis of the power to tax was not and cannot be made dependent upon the situs of the property in all cases, it being in or out of the United States, and was not and cannot be made dependent upon the domicile of the citizen, that being in or out of the United States, but upon his relation [CIVIL FRANCHISE STATUS ELECTION] as citizen to the United States and the relation of the latter to him as citizen. The consequence of the relations is that the native citizen who is taxed may have domicile, and the property from which his income is derived may have situs, in a foreign country and the tax be legal — the government having power to impose the tax.

[Cook v. Tait, 265 U.S. 47, 56 (1924);

SOURCE: https://scholar.google.com/scholar_case?case=10657110310496192378]“A voluntary acceptance of the benefit of a transaction is equivalent to a consent to all obligations arising from it, so far as the facts are known, or ought to be known, to the person accepting” California [Civil Code, Section 1589]

5.2. VOLUNTARY Acceptance creates a “quasi contract”

“Even if the judgment is deemed to be colored by the nature of the obligation whose validity it establishes, and we are free to re-examine it, and, if we find it to be based on an obligation penal in character, to refuse to enforce it outside the state where rendered, see Wisconsin v. Pelican Insurance Co., 127 U.S. 265 , 292, et seq. 8 S.Ct. 1370, compare Fauntleroy v. Lum, 210 U.S. 230 , 28 S.Ct. 641, still the obligation to pay taxes is not penal. It is a statutory liability, quasi contractual in nature, enforceable, if there is no exclusive statutory remedy, in the civil courts by the common-law action of debt or indebitatus assumpsit. United States v. Chamberlin, 219 U.S. 250 , 31 S.Ct. 155; Price v. United States, 269 U.S. 492 , 46 S.Ct. 180; Dollar Savings Bank v. United States, 19 Wall. 227; and see Stockwell v. United States, 13 Wall. 531, 542; Meredith v. United States, 13 Pet. 486, 493. This was the rule established in the English courts before the Declaration of Independence. Attorney General v. Weeks, Bunbury’s Exch. Rep. 223; Attorney General v. Jewers and Batty, Bunbury’s Exch. Rep. 225; Attorney General v. Hatton, Bunbury’s Exch. Rep. [296 U.S. 268, 272] 262; Attorney General v. _ _, 2 Ans.Rep. 558; see Comyn’s Digest (Title ‘Dett,’ A, 9); 1 Chitty on Pleading, 123; cf. Attorney General v. Sewell, 4 M.&W. 77. “

[Milwaukee v. White, 296 U.S. 268 (1935)];

SOURCE: http://caselaw.lp.findlaw.com/scripts/getcase.pl?navby=case&court=us&vol=296&page=268

5.3. Result of VOLUNTARY ACCEPTANCE is you become “federal personnel”

TITLE 5 > PART I > CHAPTER 5 > SUBCHAPTER II > § 552a

§552a. Records maintained on individuals(a) Definitions.— For purposes of this section—

(13) the term “Federal personnel” means officers and employees of the Government of the United States, members of the uniformed services (including members of the Reserve Components), individuals entitled to receive immediate or deferred retirement benefits under any retirement program of the Government of the United States (including survivor benefits).

- Foreign Sovereign Immunities Act, 28 U.S.C. Chapter 97.

- International Shoe Co. v. Washington, 326 U.S. 310 (1945).

The MINIMUM CONTACTS TEST is a legal standard used to determine if a court has jurisdiction over an out-of-state defendant. To meet this test, the following elements must be satisfied:

- Reasonableness: Exercising jurisdiction must be reasonable and fair, considering the burden on the defendant, the forum state’s interest in adjudicating the dispute, and the plaintiff’s interest in obtaining convenient and effective relief.

- Purposeful Availment: The defendant must have purposefully availed themselves of the privilege of conducting activities within the forum state, thus invoking the benefits and protections of its laws.

- Foreseeability: It must be foreseeable that the defendant could be haled into court in the forum state.

- Relatedness: The litigation must arise out of or relate to the defendant’s contacts with the forum state.

The above goes BOTH WAYS. If you don’t want the benefit or privilege and the government insists you must pay for them or obey the obligations anyway, then THEY and not YOU are:

- Satisfying the MINIMUM CONTACTS TEST.

- Operating in a purely private capacity.

- Stealing private property in violation of the Fifth Amendment.

- Waiving official, judicial, and sovereign immunity.

“[T]he doctrine of sovereign immunity is not a constitutional right; it is a common law theory or defense established by [our Supreme] Court…. Thus, when there is a clash between these constitutional rights and sovereign immunity, the constitutional rights must prevail.” Id. at 786, 413 S.E.2d at 292. Every expropriation of a citizen’s fruits of his or her labor by the government is a taking, whether through taxation or by the power of eminent domain. However, of all rights enumerated in our constitutions, only the taking of an individual’s property rights by the sovereign for public use requires remuneration. This right “was designed to bar Government from forcing some people alone to bear public burdens which, in all fairness and justice, should be borne by the public as a whole.” Armstrong v. United States , 364 U.S. 40, 49, 80 S.Ct. 1563, 1569, 4 L.Ed.2d 1554, 1561 (1960).”

[Beroth Oil Co. v. N.C. Dep’t of Transp., 256 N.C. App. 401, 415 (N.C. Ct. App. 2017)]

See:

Are You “Playing the Harlot” with the Government?, SEDM

https://sedm.org/are-you-playing-the-harlot/

6. ACCEPTANCE IS THE ORIGIN OF THE POWER TO ENFORCE

United States Constitution

Article 4, Section 3, Clause 2The Congress shall have Power to dispose of and make all needful Rules and Regulations respecting the Territory or other Property belonging to the United States; and nothing in this Constitution shall be so construed as to Prejudice any Claims of the United States, or of any particular State.

“It is only where some right or privilege [which are GOVERNMENT PROPERTY] is conferred by the government or municipality upon the owner, which he can use in connection with his property, or by means of which the use of his property is rendered more valuable to him, or he thereby enjoys an advantage over others, that the compensation to be received by him becomes a legitimate matter of regulation. Submission to the regulation of compensation in such cases is an implied condition of the grant, and the State, in exercising its power of prescribing the compensation, only determines the conditions upon which its concession shall be enjoyed. When the privilege ends, the power of regulation ceases.”

[Munn v. Illinois, 94 U.S. 113 (1876);

SOURCE: https://scholar.google.com/scholar_case?case=6419197193322400931]

6.3. The clearest, most succinct evidence of the fact that government franchises and the “benefits” (meaning PROPERTY) they confer are the source of the loss of your rights is found in the following authorities.

These authorities establish that no publication of rules in the Federal Register is necessary in the case of those in receipt of government benefits or in possession of government property. The result is that you must follow ANY and ALL of the enactments of Congress in exchange for the PRIVILEGE of receiving the benefit and you in effect, become a public officer or employee in the process. The “individual” they are talking about is, in fact THE “officer and individual” mentioned in 5 U.S.C. §2105(a) who must obey ALL the enactments of congress:

5 U.S. Code §553 – Rule making

(a) This section applies, according to the provisions thereof, except to the extent that there is involved—

(2) a matter relating to agency management or personnel or to public property, loans, grants, benefits, or contracts.

_______________________________________________________________________________________

TITLE 5 > PART I > CHAPTER 5 > SUBCHAPTER II > §552a

§552a. Records maintained on individualsDefinitions.— For purposes of this section—

(12) the term “Federal benefit program” means any program administered or funded by the Federal Government, or by any agent or State on behalf of the Federal Government, providing cash or in-kind assistance in the form of payments, grants, loans, or loan guarantees to individuals;. . .

_______________________________________________________________________________________

“The principle is invoked that one who accepts the benefit of a statute cannot be heard to question its constitutionality. Great Falls Manufacturing Co. v. Attorney General, 124 U.S. 581, 8 S.Ct. 631, 31 L.Ed. 527; Wall v. Parrot Silver & Copper Co., 244 U.S. 407, 37 S.Ct. 609, 61 L.Ed. 1229; St. Louis, etc., Co., v. George C. Prendergast Const. Co., 260 U.S. 469, 43 S.Ct. 178, 67 L.Ed. 351.”

[Ashwander v. Tennessee Valley Authority, 297 U.S. 288, 56 S.Ct. 466 (1936);

SOURCE: https://scholar.google.com/scholar_case?case=17743531891216865789]

The criteria to LAWFULLY receive a government “benefit” are:

- The CONSENTING Buyer (U.C.C. §2-103(1)(a)) of the privilege must be an “Individual”, who is defined in 5 U.S.C. §552a(a)(2) as a “citizen or resident of the United States**” (federal zone, not constitutional state) domiciled on federal territory and not within any state of the Union.

- The CONSENTING Buyer (U.C.C. §2-103(1)(a)) of the privilege must receive cash or in-kind assistance in the form of payments, grants, loans, or loan guarantees.

- The party must be ELIGIBLE BY LAW rather than BY FIAT or purely judicial discretion to “receive” the benefit.

3.1. If they aren’t legally eligible, then technically, they are not in “receipt” of the LAWFUL “benefit” but instead are merely criminal money launderers if they do in fact receive these ILLEGAL payments. See Form #05.044 for details on money laundering.

3.2. People in states of the Union ARE NOT eligible to receive Social Security or ANY OTHER government benefit, but because of the misrepresentation of eligibility and violation of law by those ADMINISTERING the program, they are offered and paid the benefit ILLEGALLY and UNCONSTITUTIONALLY, as proven below:

| Why You Aren’t Eligible for Social Security, Form #06.001 https://sedm.org/Forms/06-AvoidingFranch/SSNotEligible.pdf |

7. ENFORCEMENT OF OBLIGATIONS ATTACHED TO THE PRIVILEGE CANNOT PRODUCE UNJUST ENRICHMENT BY THE GOVERNMENT

More on the subject of this section at:

- AI DISCOVERY: Abuse of State Driver Licensing Monopoly to effect Unconstitutional Conditions that Destroy Rights, SEDM

https://sedm.org/ai-discovery-abuse-of-state-driver-licensing-monopoly-to-effect-unconstitutional-conditions-that-destroy-rights/ - Anti-Weaponization Attachment, FTSIG

https://ftsig.org/anti-weaponization-attachment/ - Reference->Member Subscriber DVDs->TaxDVD** menu, SEDM (OFFSITE LINK)

Look in the \Franchises\UnconstCondit directory

https://sedm.org/reference/dvds/tax-dvd/ - Government Instituted Slavery Using Franchises, Form #05.030, Section 28.3: Unconstitutional Conditions

https://sedm.org/Forms/05-MemLaw/Franchises.pdf

The power of taxation, indispensable to the existence of every civilized government, is exercised upon the assumption of an equivalent rendered to the taxpayer in the protection of his person and property, in adding to the value of such property, or in the creation and maintenance of public conveniences in which he shares, such, for instance, as roads, bridges, sidewalks, pavements, and schools for the education of his children. If the taxing power be in no position to render these services, or otherwise to benefit the person or property taxed, and such property be wholly within the taxing power of another State, to which it may be said to owe an allegiance and to which it looks for protection, the taxation of such property within the domicil of the owner partakes rather of the nature of an extortion than a tax, and has been repeatedly held by this court to be beyond the power of the legislature and a taking of property without due process of law. Railroad Company v. Jackson, 7 Wall. 262; State Tax on Foreign-held Bonds, 15 Wall. 300; Tappan v. Merchants’ National Bank, 19 Wall. 490, 499; Delaware &c. R.R. Co. v. Pennsylvania, 198 U.S. 341, 358. In Chicago &c. R.R. Co. v. Chicago, 166 U.S. 226, it was held, after full consideration, that the taking of private property 203*203 without compensation was a denial of due process within the Fourteenth Amendment. See also Davidson v. New Orleans, 96 U.S. 97, 102; Missouri Pacific Railway v. Nebraska, 164 U.S. 403, 417; Mount Hope Cemetery v. Boston, 158 Massachusetts, 509, 519.

Most modern legislation upon this subject has been directed (1) to the requirement that every citizen shall disclose the amount of his property subject to taxation and shall contribute in proportion to such amount; and (2) to the voidance of double taxation. As said by Adam Smith in his “Wealth of Nations,” Book V., Ch. 2, Pt. 2, “the subjects of every State ought to contribute towards the support of the Government as nearly as possible in proportion to their respective abilities; that is, in proportion to the revenue which they respectively enjoy under the protection of the State. The expense of Government to the individuals [COWS] of a great nation [FARM] is like the expense of management to the joint tenants of a great estate [surety for debts but not owners of the PLANTATION], who are all obliged [OWNERS aren’t OBLIGATED to do ANYTHING, only CATTLE ARE] to contribute in proportion to their respective interest in the estate. In the observation or neglect of this maxim consists what is called equality or inequality of taxation. “

But notwithstanding the rule of uniformity lying at the basis of every just system of taxation, there are doubtless many individual cases where the weight of a tax falls unequally upon the owners of the property taxed. This is almost unavoidable under every system of direct taxation. But the tax is not rendered illegal by such discrimination. Thus every citizen is bound to pay his proportion of a school tax, though he have no children; of a police tax, though he have no buildings or personal property to be guarded; or of a road tax, though he never use the road. In other words, a general tax cannot be dissected to show that, as to certain constituent parts, the taxpayer receives no benefit. Even in case of special assessments imposed for the improvement of property within certain limits, the fact that it is extremely doubtful whether a particular lot can receive any benefit from the improvement does not invalidate the tax with respect to such lot. Kelly v. Pittsburgh, 204*204 104 U.S. 78; Amesbury Nail Factory Co. v. Weed, 17 Massachusetts, 53; Thomas v. Gay, 169 U.S. 264; Louisville &c. R.R. Co. v. Barber Asphalt Co., 197 U.S. 430. Subject to these individual exceptions, the rule is that in classifying property for taxation some benefit to the property taxed is a controlling consideration, and a plain abuse of this power will sometimes justify a judicial interference. Norwood v. Baker, 172 U.S. 269. It is often said protection and payment of taxes are correlative obligations.

[Union Refrigerator Transit Co. v. Kentucky, 199 US 194 (1905);

SOURCE: https://scholar.google.com/scholar_case?case=14163786757633929654]

8. REQUIREMENT TO PAY FOR

“A person is ordinarily not required to pay for benefits which were thrust upon him with no opportunity to refuse them. The fact that he is enriched is not enough, if he cannot avoid the enrichment.” Wade, Restitution for Benefits Conferred Without Request, 19 Vand. L. Rev. at 1198 (1966).

[Siskron v. Temel-Peck Enterprises, 26 N.C.App. 387, 390 (N.C. Ct. App. 1975)]

9. RIGHT TO REFUSE BENEFIT

“Cujus est commodum ejus debet esse incommodum.

He who receives the benefit should also bear the disadvantage.”“Que sentit commodum, sentire debet et onus.

He who derives a benefit from a thing, ought to feel the disadvantages attending it. 2 Bouv. Inst. n. 1433.”Commodum ex injuri su non habere debet.

No man ought to derive any benefit of his own wrong. Jenk. Cent. 161.Invito beneficium non datur.

No one is obliged to accept a benefit against his consent. Dig. 50, 17, 69. But if he does not dissent he will be considered as assenting. Vide Assent.Potest quis renunciare pro se, et suis, juri quod pro se introductum est.

A man may relinquish, for himself and his heirs, a right which was introduced for his own benefit. See 1 Bouv. Inst. n. 83.Quilibet potest renunciare juri pro se inducto.

Any one may renounce a law introduced for his own benefit. To this rule there are some exceptions. See 1 Bouv. Inst. n. 83.[Bouvier’s Maxims of Law, 1856;

SOURCE: http://famguardian.org/Publications/BouvierMaximsOfLaw/BouviersMaxims.htm]

10. CIVIL STATUTORY LAW IS A PRIVILEGE YOU CAN AVOID

More on the subject of this section at:

- Why Domicile and Becoming a “Taxpayer” Require Your Consent, Form #05.002

https://sedm.org/Forms/05-MemLaw/Domicile.pdf - Why Statutory Civil Law is Law for Government and Not Private Persons, Form #05.037

https://sedm.org/Forms/05-MemLaw/StatLawGovt.pdf - Government Identity Theft, Form #05.046-what happens when they FORCE you to participate in a privilege or franchise or benefit such as the civil statutory law.

https://sedm.org/Forms/05-MemLaw/GovernmentIdentityTheft.pdf

Appellant, a citizen and resident of Mississippi, brought the present suit to set aside the assessment of a tax upon so much of his net income for 1929 as arose from the construction by him of public highways in the State of Tennessee. The taxing statute was challenged on the ground that in so far as it imposes a tax on income derived wholly from activities carried on outside the state, it deprived appellant of property without due process of law, and that in exempting corporations, which were his competitors, from a tax on income derived from like activities carried on outside the state, it denied to him the equal protection of the laws.

The obligation of one domiciled within a state to pay taxes there, arises from unilateral action of the state government in the exercise of the most plenary of sovereign powers, that to raise revenue to defray the expenses of government and to distribute its burdens equably among those who enjoy its benefits. Hence, domicile in itself establishes a basis for taxation. Enjoyment of the privileges of residence within the state, and the attendant right to invoke the protection of its laws, are inseparable from the responsibility for sharing the costs of government. See Fidelity & Columbia Trust Co. v. Louisville, 245 U.S. 54, 58; Maguire v. Trefry, 253 U.S. 12, 14, 17; Kirtland v. Hotchkiss, 100 U.S. 491, 498; Shaffer v. Carter, 252 U.S. 37, 50. The Federal Constitution imposes on the states no particular modes of taxation, and apart from the specific grant to the federal government of the exclusive 280*280 power to levy certain limited classes of taxes and to regulate interstate and foreign commerce, it leaves the states unrestricted in their power to tax those domiciled within them, so long as the tax imposed is upon property within the state or on privileges enjoyed there, and is not so palpably arbitrary or unreasonable as to infringe the Fourteenth Amendment. Kirtland v. Hotchkiss, supra.

Taxation at the place of domicile of tangibles located elsewhere has been thought to be beyond the jurisdiction of the state, Union Refrigerator Transit Co. v. Kentucky, 199 U.S. 194; Frick v. Pennsylvania, 268 U.S. 473, 488-489; but considerations applicable to ownership of physical objects located outside the taxing jurisdiction, which have led to that conclusion, are obviously inapplicable to the taxation of intangibles at the place of domicile or of privileges which may be enjoyed there. See Foreign Held Bond Case, 15 Wall. 300, 319; Frick v. Pennsylvania, supra, p. 494. And the taxation of both by the state of the domicile has been uniformly upheld. Kirtland v. Hotchkiss, supra; Fidelity & Columbia Trust Co. v. Louisville, supra; Blodgett v. Silberman, 277 U.S. 1; Maguire v. Trefry, supra; compare Farmers Loan & Trust Co. v. Minnesota, 280 U.S. 204; First National Bank v. Maine, 284 U.S. 312.

The present tax has been defined by the Supreme Court of Mississippi as an excise and not a property tax, Hattiesburg Grocery Co. v. Robertson, 126 Miss. 34; 88 So. 4; Knox v. Gulf, M. & N.R. Co., 138 Miss. 70; 104 So. 689, but in passing on its constitutionality we are concerned only with its practical operation, not its definition or the precise form of descriptive words which may be applied to it. See Educational Films Corp. v. Ward, 282 U.S. 379, 387; Pacific Co. v. Johnson, 285 U.S. 480; Shaffer v. Carter, supra, pp. 54-55.

It is enough, so far as the constitutional power of the state to levy it is concerned, that the tax is imposed 281*281 by Mississippi on its own citizens with reference to the receipt and enjoyment of income derived from the conduct of business, regardless of the place where it is carried on. The tax, which is apportioned to the ability of the taxpayer to bear it, is founded upon the protection afforded to the recipient of the income by the state, in his person, in his right to receive the income, and in his enjoyment of it when received. These are rights and privileges incident to his domicile in the state and to them the economic interest realized by the receipt of income or represented by the power to control it, bears a direct legal relationship. It would be anomalous to say that although Mississippi may tax the obligation to pay appellant for his services rendered in Tennessee, see Fidelity & Columbia Trust Co. v. Louisville, supra; Farmers Loan & Trust Co. v. Minnesota, supra, still, it could not tax the receipt of income upon payment of that same obligation. We can find no basis for holding that taxation of the income at the domicile of the recipient is either within the purview of the rule now established that tangibles located outside the state of the owner are not subject to taxation within it, or is in any respect so arbitrary or unreasonable as to place it outside the constitutional power of taxation reserved to the state. Maguire v. Trefry, supra; see Fidelity & Columbia Trust Co. v. Louisville, supra.

The Supreme Court of Mississippi found it unnecessary to pass upon the validity of so much of the statute, added by the amendment of 1928, as exempted domestic corporations from the tax on income derived from activities outside the state. It said that if the amendment were valid, appellant could not complain; if invalid, he would still be subject to the tax, since the act which it amended, § 11, c. 132, Laws of 1924, would then remain in full force, and under it individuals and domestic corporations are taxed alike. Knox v. Gulf, M. & N.R. Co., supra.

282*282 But the Constitution, which guarantees rights and immunities to the citizen, likewise insures to him the privilege of having those rights and immunities judicially declared and protected when such judicial action is properly invoked. Even though the claimed constitutional protection be denied on non-federal grounds, it is the province of this Court to inquire whether the decision of the state court rests upon a fair or substantial basis. If unsubstantial, constitutional obligations may not be thus avoided. See Ward v. Love County, 253 U.S. 17, 22; Enterprise Irrigation District v. Canal Co., 243 U.S. 157, 164; Fox River Paper Co. v. Railroad Commission, 274 U.S. 651, 655. Upon one of the alternative assumptions made by the court, that the amendment is discriminatory, appellant’s constitutional rights were infringed when the tax was levied upon him, and state officers acting under the amendment refrained from assessing the like tax upon his corporate competitors. See Iowa-Des Moines National Bank v. Bennett, 284 U.S. 239, 246. If the Constitution exacts a uniform application of this tax on appellant and his competitors, his constitutional rights are denied as well by the refusal of the state court to decide the question, as by an erroneous decision of it, see Greene v. Louisville & Interurban R. Co., 244 U.S. 499, 508, 512 et seq.; Smith v. Cahoon, 283 U.S. 553, 564, for in either case the inequality complained of is left undisturbed by the state court whose jurisdiction to remove it was rightly invoked. The burden does not rest on him to test again the validity of the amendment by some procedure to compel his competitors to pay the tax under the earlier statute. Iowa-Des Moines Nat. Bank v. Bennett, supra, p. 247. See Cumberland Coal Co. v. Board of Revision, 284 U.S. 23. We therefore conclude that the purported non-federal ground put forward by the state court for its refusal to decide the constitutional question was unsubstantial and 283*283 illusory, and that the appellant may invoke the jurisdiction of this Court to decide the question.

[Lawrence v. State Tax Commission, 286 U.S. 276 (1932); SOURCE: https://scholar.google.com/scholar_case?case=10241277000101996613]

11. YOUR EQUAL RIGHT TO USE PRIVILEGES AGAINST THE GOVERNMENT

“The State in such cases exercises no greater right than an individual may exercise over the use of his own property when leased or loaned to others. The conditions upon which the privilege shall be enjoyed being stated or implied in the legislation authorizing its grant, no right is, of course, impaired by their enforcement. The recipient of the privilege, in effect, stipulates to comply with the conditions. It matters not how limited the privilege conferred, its acceptance implies an assent to the regulation of its use and the compensation for it.”

[Munn v. Illinois, 94 U.S. 113 (1876);

SOURCE: https://scholar.google.com/scholar_case?case=6419197193322400931 ]

For an example of how to implement the above, see:

Injury Defense Franchise and Agreement, Form #06.027

https://sedm.org/Forms/06-AvoidingFranch/InjuryDefenseFranchise.pdf

12. SUPREME COURT DOCTRINES THAT IMPLEMENT PRIVILEGES AND BENEFITS

- Constitutional Avoidance Doctrine, U.S. Supreme Court. See:

Catalog of U.S. Supreme Court Doctrines, Litigation Tool #10.020, Section 5.13

https://sedm.org/Litigation/10-PracticeGuides/SCDoctrines.pdf - Public Rights Doctrine, U.S. Supreme Court. See:

Catalog of U.S. Supreme Court Doctrines, Litigation Tool #10.020, Section 5.3

https://sedm.org/Litigation/10-PracticeGuides/SCDoctrines.pdf

13. How to Reject All Privileges in a Tax Return Filing

How to Reject All Privileges in a Tax Return Filing, FTSIG

https://ftsig.org/how-to-reject-all-privileges-in-a-tax-return-filing/

14. THE problem with FEDERAL privileges within the CONSTITUTIONAL states

“Thus, Congress having power to regulate commerce with foreign nations, and among the several States, and with the Indian tribes, may, without doubt, provide for granting coasting licenses, licenses to pilots, licenses to trade with the Indians, and any other licenses necessary or proper for the exercise of that great and extensive power; and the same observation is applicable to every other power of Congress, to the exercise of which the granting of licenses may be incident. All such licenses confer authority, and give rights to the licensee.

But very different considerations apply to the internal commerce or domestic trade of the States. Over this commerce and trade Congress has no power of regulation nor any direct control. This power belongs exclusively to the States. No interference by Congress with the business of citizens transacted within a State is warranted by the Constitution, except such as is strictly incidental to the exercise of powers clearly granted to the legislature. The power to authorize [e.g. LICENSE or turn into a franchise] a business within a State is plainly repugnant to the exclusive power of the State over the same subject. It is true that the power of Congress to tax is a very extensive power. It is given in the Constitution, with only one exception and only two qualifications. Congress cannot tax exports, and it must impose direct taxes by the rule of apportionment, and indirect taxes by the rule of uniformity. Thus limited, and thus only, it reaches every subject, and may be exercised at discretion. But, it reaches only existing subjects. Congress cannot authorize [e.g. “license”] a trade or business within a State in order to tax it.”

[License Tax Cases, 72 U.S. 462, 18 L.Ed. 497, 5 Wall. 462, 2 A.F.T.R. 2224 (1866) ]

“The power to “legislate generally upon” life, liberty, and property, as opposed to the “power to provide modes of redress” against offensive state action, was “repugnant” to the Constitution. Id., at 15. See also United States v. Reese, 92 U.S. 214, 218 (1876) ; United States v. Harris, 106 U.S. 629, 639 (1883) ; James v. Bowman, 190 U.S. 127, 139 (1903) . Although the specific holdings of these early cases might have been superseded or modified, see, e.g., Heart of Atlanta Motel, Inc. v. United States, 379 U.S. 241 (1964) ; United States v. Guest, 383 U.S. 745 (1966) , their treatment of Congress’ §5 power as corrective or preventive, not definitional, has not been questioned.”

[City of Boerne v. Florez, Archbishop of San Antonio, 521 U.S. 507 (1997) ]

Mr. Logan: “…Natural laws can not be created, repealed, or modified by legislation. Congress should know there are many things which it can not do…”

“It is now proposed to make the Federal Government the guardian of its citizens. If that should be done, the Nation soon must perish. There can only be a free nation when the people themselves are free and administer the government which they have set up to protect their rights. Where the general government must provide work, and incidentally food and clothing for its citizens, freedom and individuality will be destroyed and eventually the citizens will become serfs to the general government…”

[Congressional Record-Senate, Volume 77- Part 4, June 10, 1933, Page 12522;SOURCE: http://famguardian.org/TaxFreedom/CitesByTopic/Sovereignty-CongRecord-Senate-JUNE101932.pdf]

“It is the greatest absurdity to suppose it [would be] in the power of one, or any number of men, at the entering into society, to renounce their essential natural rights, or the means of preserving those rights; when the grand end of civil government, from the very nature of its institution, is for the support, protection, and defense of those very rights; the principal of which … are life, liberty, and property. If men, through fear, fraud, or mistake, should in terms renounce or give up any essential natural right, the eternal law of reason and the grand end of society would absolutely vacate such renunciation. The right to freedom being the gift [CREATION] of God Almighty, it is not in the power of man to alienate this gift and voluntarily become a slave”

[Samuel Adams, The Rights of the Colonists, November 20, 1772; http://www.foundingfatherquotes.com/father/quotes/2]

“My ardent desire is, and my aim has been…to comply strictly with all our engagements foreign and domestic; but to keep the United States free from political connections with every other Country. To see that they may be independent of all, and under the influence of none. In a word, I want an American character, that the powers of Europe may be convinced we act for ourselves and not for others [as “public officers”]; this, in my judgment, is the only way to be respected abroad and happy at home.”

[George Washington, (letter to Patrick Henry, 9 October 1775);

Reference: The Writings of George Washington, Fitzpatrick, ed., vol. 34 (335)]

“Take heed to yourself, lest you make a covenant or mutual agreement [contract, franchise agreement] with the inhabitants of the land to which you go, lest it become a snare in the midst of you.”

[Exodus 34:12, Bible, Amplified version]

“You shall make no covenant [contract or franchise] with them [foreigners, pagans], nor with their [pagan government] gods [laws or judges]. They shall not dwell in your land [and you shall not dwell in theirs by becoming a “resident” in the process of contracting with them], lest they make you sin against Me [God]. For if you serve their gods [under contract or agreement or franchise], it will surely be a snare to you.”

[Exodus 23:32-33, Bible, NKJV]

15. PRIVILEGES in a NUTSHELL