USPI thru Changing the Status of Your PROPERTY to Domestic

TABLE OF CONTENTS

- Introduction

- The PROPERTY Angle of the Scam

- Consequences of making ALL government payments PUBLIC property AFTER they are received without your consent or permission

- Diagrams

- 26 U.S.C. 871(a): Not Effectively Connected (NEC)

- 26 U.S.C. 871(b) Effectively Connected (1040-NR main form)

6.1. Definition

6.2. THREE types of EC: Involuntary, Optional, and Mistaken

6.3. Why Involuntary Effectively Connected Income is a SCAM for American Nationals

6.4. Traps/Springes on the 1040-NR Effectively Connected Section

6.5. Defense from the Traps

6.6. Sample Statement to Attach to 1040-NR return relating to “Effectively Connected” Blocks - Conclusion

1. Introduction

We have already covered how your election to a DOMESTIC/PUBLIC statutory “U.S. person” status creates obligations to pay income tax on your worldwide earnings no matter where you are. If you get smart and stop making that IGNORANT and EXTREMELY costly and UNNECESSARY election, there is still another hurdle Uncle Sam will try to trip you up with. That hurdle consists of seeking or receiving gross income from a “U.S. source” under 26 U.S.C. §871. This statute is divided into TWO classes of “gross income”:

- Income Not Connected with United States business—30 percent tax under 26 U.S.C. §871(a).

1.1. This goes on the Schedule NEC (Not Effectively Connected) form with the 1040NR filing.

1.2. This is typically government payments ONLY. To tax payments between private people, the government would have to interfere with the right to contract of both parties and STEAL private property, which would be unconstitutional.

1.3. We allege that the property subject to taxation in this provision is ONLY PUBLIC property and never PRIVATE property. 26 U.S.C. §864(c)(3) alludes to this.

1.4. This includes everything under 26 U.S.C. §871(a)(1) only, because 26 U.S.C. §871(a)(2) and (3) are ECI as well, according to 26 U.S.C. §864(c)(3).

1.5. This also includes everything under 26 U.S.C. §871(h), 26 U.S.C. §881(a), and 26 U.S.C. §881(c). - Income Connected with United States business—graduated rate of tax under 26 U.S.C. §871(b).

2.1. This goes directly on the 1040-NR form.

2.2. This is also called “Effectively Connected Income” (ECI).

2.3. The THING it is connected to is the excise taxable “trade or business” franchise, which is an office in the national government. Since no one can FORCE you WORK in such an office, then it is voluntary. See:

The “Trade or Business” Scam, Form #05.001

https://sedm.org/Forms/05-MemLaw/TradeOrBusScam.pdf

2.4. The “United States” in this context is the government as a legal person, which consists entirely and only of OFFICES and PROPERTY.

2.5. Since OFFICES are also property, it consists essentially of ONLY PUBLIC/GOVERNMENT property.

2.6. This status makes the earnings taxable anywhere in the world and is nongeographical.

2.7. It is entirely voluntary in nearly all cases.

2.8. Is documented in 26 U.S.C. §864(c).

2.9. This also includes earnings from 26 U.S.C. §871(a)(2) and (3) as well, according to 26 U.S.C. §864(c)(3).

The only status of people permitted to use this website are those NOT connected to the “trade or business” excise taxable franchise as documented in 26 U.S.C. §864(c)(1)(A). In that scenario Effectively Connected Income (ECI) can still happen INVOLUNTARY under 26 U.S.C. §864(c) under the following circumstances:

- 26 U.S.C. §864(c)(6): Treatment of certain deferred payments.

- 26 U.S.C. §864(c)(7): Treatment of certain property transactions.

- 26 U.S.C. §864(c)(8): Gain or loss of foreign persons from sale or exchange of certain partnership interests.

- Federal Investment in Real Property Transfer Act (FIRPTA)

4.1. 26 U.S.C. §871(d): Election to treat real property income as income connected with “trade or business”.

4.2. 26 U.S.C. §882(d): Election to treat real property income as income connected with “trade or business”. - 26 U.S.C. §882(e): Interest on United States Obligations Received by Banks Organized in Possessions.

Item 1 above, Not Effectively Connected (NEC) under 26 U.S.C. §871(a), is the most nebulous for most people. This is mostly because of the equivocation surrounding the context of the term “United States” so that you are unable to distinguish whether the term means:

- The GEOGRAPHICAL “United States” defined in 26 U.S.C. §7701(a)(9) and (a)(10) or

- The LEGAL “United States” as a federal corporation and a “person”.

Both of the above are technically synonymous, because this site treats United StatesG as a virtual layer that United StatesSMJ attaches to by your CONSENT in some form. Your consent to convert either YOUR status or the status of your PROPERTY to the United StatesG virtual layer makes either the lawful target of government enforcement.

The above dichotomy is recognized in the Treasury Regulations at 26 C.F.R. §301.7701(b)-2(c) in the case of aliens.

For American nationals who are nonresident aliens residing and working within the exclusive jurisdiction of the Constitutional states of the Union, they are not receiving earnings from the statutory “United States” unless they are receiving government payments, benefits, or tax refunds, in which case the GEOGRAPHICAL “United States” really just means the LEGAL “United States” as a civil “person” and “corporation”. The United States federal corporation under 28 U.S.C. §3002(15)(A), by the way, is a FOREIGN corporation in respect to a Constitutional State. Thus, the term “Domestic” defined in the 26 U.S.C. §7701(a)(4) means WITHIN that corporation as a public officer, agent, or contractor, including but not limited to “taxpayer”, “person”, “citizen**+D of the United States**”, “resident of the United States*” under the Internal Revenue Code:

26 U.S. Code § 7701 – Definitions

(a)When used in this title, where not otherwise distinctly expressed or manifestly incompatible with the intent thereof—

(4)Domestic

The term “domestic” when applied to a corporation or partnership means created or organized in the United States or under the law of the United States or of any State unless, in the case of a partnership, the Secretary provides otherwise by regulations.

In terms of business entities, whether the entity is “domestic” or “foreign” is determined under the following rules:

- 26 C.F.R. §301.7701-1 Classification of organizations for federal tax purposes.

- 26 C.F.R. §301.7701-2 Business entities; definitions.

- 26 C.F.R. §301.7701-3 Classification of certain business entities.

- 26 C.F.R. §301.7701-4 Trusts.

- 26 C.F.R. §301.7701-5 Domestic and foreign business entities.

- 26 C.F.R. §301.7701-6 Definitions; person, fiduciary.

- 26 C.F.R. §301.7701-7 Trusts—domestic and foreign.

Regardless of whether we are talking about a HUMAN BEING or a BUSINESS ENTITY, in ALL CASES we have seen, those not actually physically working and doing business within the statutory GEOGRAPHICAL “United States”, if they file a DOMESTIC “U.S. person” return, are making a VOLUNTARY election to be treated AS IF they are officers and agents of the national government whose activities are “organized and directed” by the laws of the United States and therefore are acting as AGENTS of the United States. Thus, they are within the LEGAL “United States” (corporation and fictional “person”) rather than the GEOGRAPHICAL “United States”.

“The State is a political corporate body, can act only through agents, and can command only by laws. It is necessary, therefore, for such a defendant, in order to complete his defence, to produce a law of the State which constitutes his commission as its agent, and a warrant for his act. “

[Poindexter v. Greenhow, 114 U.S. 270, 288 (1885);

SOURCE: https://scholar.google.com/scholar_case?case=3335705609810307048]

The inference from the above then is that:

- Those acting under the authority of any civil law are, by definition, agents and representatives of the government which ENACTED the law.

- The income tax is a tax upon:

2.1. The OFFICE, and not the OFFICER. This includes all property voluntarily connected to the OFFICE by the SSN or TIN franchise mark. or

2.2. All property DONATED to the government by “effectively connecting” or which remained government property AFTER it was paid to you in temporary possession of it. - The income tax extends wherever the GOVERNMENT extends, and not where the GEOGRAPHY extends.

That last item is confirmed by no less than the U.S. Supreme Court! Notice they used the term “government extends” rather than “geography extends” and the phrase “without limitation as to place”.

“Loughborough v. Blake, 18 U.S. 317, 5 Wheat. 317, 5 L.Ed. 98, was an action of trespass (or, as appears by the original record, replevin) brought in the Circuit Court for the District of Columbia to try the right of Congress to impose a direct tax for general purposes on that District. 3 Stat. 216, c. 60, Fed. 17, 1815. It was insisted that Congress could act in a double capacity: in [****32] one as legislating [*260] for the States; in the other as a local legislature for the District of Columbia. In the latter character, it was admitted that the power of levying direct taxes might be exercised, but for District purposes only, as a state legislature might tax for state purposes; but that it could not legislate for the District under Art. I, sec. 8, giving to Congress the power “to lay and collect taxes, imposts and excises,” which “shall be uniform throughout the United States,” inasmuch as the District was no part of the United States. It was held that the grant of this power was a general one without limitation as to place, and consequently extended to all places over which the government extends; and that it extended to the District of Columbia as a constituent part of the United States. The fact that Art. I, sec. 20 , declares that “representatives and direct taxes shall be apportioned among the several States . . . according to their respective numbers,” furnished a standard by which taxes were apportioned; but not to exempt any part of the country from their operation. “The words used do not mean, that direct taxes shall be imposed on States only which are [****33] represented, or shall be apportioned to representatives; but that direct taxation, in its application to States, shall be apportioned to numbers.” That Art. I, sec. 9, P4, declaring that direct taxes shall be laid in proportion to the census, was applicable to the District of Columbia, “and will enable Congress to apportion on it its just and equal share of the burden, with the same accuracy as on the respective States. If the tax be laid in this proportion, it is within the very words of the restriction. It is a tax in proportion to the census or enumeration referred to.” It was further held that the words of the ninth section did not “in terms require that the system of direct taxation, when resorted to, shall be extended to the territories, as the words of the second section require that it shall be extended to all the [**777] States. They therefore may, without violence, be understood to give a rule when the territories shall be taxed without imposing the necessity of taxing them.”

[Downes v. Bidwell, 182 U.S. 244 (1901);

SOURCE: https://scholar.google.com/scholar_case?case=9926302819023946834]

2. The PROPERTY Angle of the Franchise

ALWAYS remember that as long as you have GOVERNMENT/PUBLIC property in your hands, the government has the power to regulate and tax the use of the property under the authority of Article 4, Section 3, Clause 2 of the Constitution and NOT even under the taxing powers of Congress if they choose not to even call it a tax! That is why a “franchise” is legally defined as “a privilege [PUBLIC PROPERTY] IN THE HANDS of a subject”. To wit:

FRANCHISE. A special privilege conferred by government on individual or corporation, and which does not belong to citizens of country generally of common right. Elliott v. City of Eugene, 135 Or. 108, 294 P. 358, 360. In England it is defined to be a royal privilege in the hands of a subject.

A “franchise,” as used by Blackstone in defining quo warranto, (3 Com. 262 [4th Am. Ed.] 322), had reference to a royal privilege or branch of the king’s prerogative subsisting in the hands of the subject, and must arise from the king’s grant, or be held by prescription, but today we understand a franchise to be some special privilege conferred by government on an individual, natural or artificial, which is not enjoyed by its citizens in general. State v. Fernandez, 106 Fla. 779, 143 So. 638, 639, 86 A.L.R. 240.

In this country a franchise is a privilege or immunity of a public nature, which cannot be legally exercised without legislative grant. To be a corporation is a franchise. The various powers conferred on corporations are franchises. The execution of a policy of insurance by an insurance company [e.g. Social Insurance/Socialist Security], and the issuing a bank note by an incorporated bank [such as a Federal Reserve NOTE], are franchises. People v. Utica Ins. Co.. 15 Johns., N.Y., 387, 8 Am.Dec. 243. But it does not embrace the property acquired by the exercise of the franchise. Bridgeport v. New York & N. H. R. Co., 36 Conn. 255, 4 Arn.Rep. 63. Nor involve interest in land acquired by grantee. Whitbeck v. Funk, 140 Or. 70, 12 P.2d 1019, 1020. In a popular sense, the political rights of subjects and citizens are franchises, such as the right of suffrage. etc. Pierce v. Emery, 32 N.H. 484 ; State v. Black Diamond Co., 97 Ohio St. 24, 119 N.E. 195, 199, L.R.A.l918E, 352.

[Black’s Law Dictionary, 4th Edition, pp. 786-787]

You BECOME “the subject” by literally having GOVERNMENT/PUBLIC property IN YOUR HANDS, meaning within your temporary control or possession or benefit. “Privilege” is a synonym for PUBLIC PROPERTY, by the way. Once you possess, receive, or benefit from PUBLIC property without absolutely owning it, you volunteered to become a SUBJECT and a “taxpayer”. You are in effect “renting” public property from Uncle Sam and the income tax is the “rent” to use or benefit from the property. In that sense, being a “beneficial owner” mentioned in the Internal Revenue Code is REALLY the person who owns the BENEFIT or ENTITLEMENT to the PUBLIC property, but not the actual PUBLIC PROPERTY ITSELF! Uncle owns that! See:

- Authorities on “beneficial owner”, Family Guardian Fellowship

https://famguardian.org/TaxFreedom/CitesByTopic/BeneficialOwner.htm - Website Definitions: 34. Beneficial Owner, FTSIG

https://ftsig.org/advanced/definitions/#34._Beneficial

This was further affirmed by the U.S. Supreme Court:

“When Sir Matthew Hale, and the sages of the law in his day, spoke of property as affected by a public interest, and ceasing from that cause to be juris privati solely, that is, ceasing to be held merely in private right, they referred to

[1] property dedicated [DONATED] by the owner to public uses [by EFFECTIVELY CONNECTING” it], or

[2] to property the use of which was granted by the government [e.g. Social Security Card or passport], or

[3] in connection with which special privileges were conferred [licenses, such as the SSN or TIN].

Unless the property was thus dedicated [by one of the above three mechanisms], or some right bestowed by the government was held with the property, either by specific grant or by prescription of so long a time as to imply a grant originally, the property was not affected by any public interest so as to be taken out of the category of property held in private right.”

[Munn v. Illinois, 94 U.S. 113, 139-140 (1876);

SOURCE: https://scholar.google.com/scholar_case?case=6419197193322400931]

The key thing to avoid “effective connection” of earnings is found in the following regulation:

26 C.F.R. §1.872-2 – Exclusions from gross income of nonresident alien individuals.

(f) Other exclusions.

Income which is from sources without the United States, as determined under the provisions of sections 861 through 863, and the regulations thereunder, is not included in the gross income of a nonresident alien individual unless such income is effectively connected for the taxable year with the conduct of a trade or business in the United States by that individual. To determine specific exclusions in the case of other items which are from sources within the United States, see the applicable sections of the Code. For special rules under a tax convention for determining the sources of income and for excluding, from gross income, income from sources without the United States which is effectively connected with the conduct of a trade or business in the United States, see the applicable tax convention. For determining which income from sources without the United States is effectively connected with the conduct of a trade or business in the United States, see section 864(c)(4) and § 1.864-5.

3. Consequences of making ALL government payments PUBLIC property AFTER they are received without your consent or permission

The constitution MANDATES a THICK bright red line of separation between PUBLIC and PRIVATE as documented in:

Separation Between Public and Private Course, Form #12.025

https://sedm.org/LibertyU/SeparatingPublicPrivate.pdf

On the PUBLIC side, there is no question that those who lawfully occupy an elected or appointed public office within the national government under Titles 5, 10, and 50 of the U.S. Code and receive a compensation for doing so from the national government are taxpayers and should pay their income tax. That is the very purpose of 26 U.S.C. §864(c), in fact. We conclude that in the following articles:

- Foreign Tax Status will NOT eliminate income tax obligations for Government Employees, FTSIG

https://ftsig.org/foreign-tax-status-will-not-eliminate-income-tax-obligations-for-government-employees/ - Microsoft Copilot: Do real “public officers” in Titles 5 and 10 of the U.S. Code always owe tax?, FTSIG

https://ftsig.org/microsoft-copilot-do-real-public-offices-in-titles-5-and-10-of-the-u-s-code-always-owe-tax/ - Why Your Government is a Thief or You are a “Public Officer” for Income Tax Purposes, Form #05.008

https://sedm.org/Forms/05-MemLaw/WhyThiefOrPubOfficer.pdf

Below is an example from the U.S. Supreme Court affirming that those who work as public officers implicitly waive constitutional protections and in effect agree to by taxed and regulated TO DEATH:

“The restrictions that the Constitution places upon the government in its capacity as lawmaker, i.e., as the regulator of private conduct [under the Public Interest Doctrine], are not the same as the restrictions that it places upon the government in its capacity as employer. We have recognized this in many contexts, with respect to many different constitutional guarantees. Private citizens perhaps cannot be prevented from wearing long hair, but policemen can. Kelley v. Johnson, 425 U.S. 238, 247 (1976). Private citizens cannot have their property searched without probable cause, but in many circumstances government employees can. O’Connor v. Ortega, 480 U.S. 709, 723 (1987) (plurality opinion); id., at 732 (SCALIA, J., concurring in judgment). Private citizens cannot be punished for refusing to provide the government information that may incriminate them, but government employees can be dismissed when the incriminating information that they refuse to provide relates to the performance of their job. Gardner v. Broderick, [497 U.S. 62, 95] 392 U.S. 273, 277 -278 (1968). With regard to freedom of speech in particular: Private citizens cannot be punished for speech of merely private concern, but government employees can be fired for that reason. Connick v. Myers, 461 U.S. 138, 147 (1983). Private citizens cannot be punished for partisan political activity, but federal and state employees can be dismissed and otherwise punished for that reason. Public Workers v. Mitchell, 330 U.S. 75, 101 (1947); Civil Service Comm’n v. Letter Carriers, 413 U.S. 548, 556 (1973); Broadrick v. Oklahoma, 413 U.S. 601, 616 -617 (1973).”

[Rutan v. Republican Party of Illinois, 497 U.S. 62, 94-95 (1990);

SOURCE: https://scholar.google.com/scholar_case?case=5322176927652912012]

Unfortunately, through sophistry and equivocation, the I.R.C. blurs the lines between public and private to in effect make “U.S. persons” in 26 U.S.C. §7701(a)(30) and “persons” in 26 U.S.C. §6671(b) and 26 U.S.C. §7343 into the equivalent of public officers above. Those who elect the “nonresident alien” status become said “person” through “effectively connected” elections by virtue of 26 U.S.C. §864(b).

HOWEVER, on the PRIVATE side in the case of those who are not lawfully employed as public officers, such as “U.S. persons” or “nonresident aliens” who effectively connect, constitutional protections of PRIVATE property and PRIVATE rights prevent the involuntary collection of the income tax from non-consenting private people. Constitutional protections remain intact for these people and they remain as PRIVATE, FOREIGN, and “non-persons”. They and their property are not subject to federal preemption so they have to be LEFT ALONE as “justice” itself requires. They come under the protections of the laws of the locality and state they reside in instead. Any kind of elections or consent REMOVE such protections under the Constitutional Avoidance Doctrine and the Public Rights Doctrine of the U.S. Supreme Court.

For PRIVATE, constitutionally protected people who have consented or elected to NOTHING, even assuming that U.S. source means government payment and USPI, by retaining a property interest in the U.S. source payment AFTER it is received by you to render the ENTIRE amount taxable as a direct tax, Uncle Sam is:

- Acting as an “Indian Giver”

- Engaging in a conspiracy to destroy your happiness, because private property is synonymous with “pursuit of happiness” as interpreted by the U.S. Supreme Court.

- Using its own disbursements to solicit or demand a bribe or kickback to receive the payment to begin with. Bribery is a crime.

- Committing extortion, which is a crime.

- Not giving you reasonable notice about how it acquires jurisdiction by confusing “U.S. source” with a geography instead of a government.

- Violating the Unconstitutional Conditions Doctrine. See below.

- Unconstitutionally interfering with its own contracts in violation of Constitution Article 1, Section 10 if the payment fulfilled a contractual obligation, such as an enlistment contract by unilaterally reducing the consideration in violation of the Clearfield Doctrine.

The above lead us to believe that the income tax therefore cannot rationally behave as a “quid pro quo” or “quantum meruit” exchange of consideration whenever the government pays you money. That would be a dishonest, corrupt, and even criminal act of extortion.

In the case of item 6 above, Congress cannot condition receipt of a federal benefit (such as tax deductions) or payment on bribing them with a kickback that surrenders private property rights protected by the Fifth Amendment. That’s a violation of the unconstitutional conditions doctrine if you were standing on land within the exclusive jurisdiction of a constitutional state of the Union that is protected by the constitution. However, it would not be such a violation in places NOT protected by the Constitution, such as federal enclaves, abroad, territories, and possessions, or even NRAAliens doing business in the states of the Union but residing in places not protected by the constitution such as abroad.

“. . .this Court has made clear that even though a person has no “right” to a valuable governmental benefit and even though the government may deny him the benefit for any number of reasons, there are some reasons upon which the government may not rely. It may not deny a benefit to a person on a basis that infringes his constitutionally protected interests— especially, his interest in freedom of speech. For if the government could deny a benefit to a person because of his constitutionally protected speech or associations, his exercise of those freedoms would in effect be penalized and inhibited. This would allow the government to “produce a result which [it] could not command directly.” Speiser v. Randall, 357 U. S. 513, 526. Such interference with constitutional rights is impermissible.

[Perry v. Sindermann, 408 U.S. 593, 597 (1972);

SOURCE: https://scholar.google.com/scholar_case?case=4415013413682250783]

In Nollan v. California Coastal Commission, 483 U.S. 825 (1987), the U.S. Supreme court held that conditioning a building permit on granting public access across private property was held to violate the Takings Clause of the Fifth Amendment. This is a classic example of the government demanding a property right in exchange for a regulatory benefit, which the Court found unconstitutional.

In Dolan v. City of Tigard, 512 U.S. 374 (1994), the Court struck down a permit condition requiring landowners to dedicate land for public use, reinforcing that exactions must be proportional and justified. This case further refined the unconstitutional conditions doctrine in the context of land-use regulation.

In Koontz v. St. Johns River Water Management District, 570 U.S. 595 (2013), the U.S. Supreme Court held that monetary exactions (not just land) can also trigger the unconstitutional conditions doctrine. This extended the doctrine to financial demands tied to government benefits or approvals or even just payments of any kind.

As far as the application of these same protections of the constitution to territories and possessions, however, the U.S. Supreme Court held that such Constitutional protections, including Fifth Amendment protections for private property, do not automatically extend to them unless Congress expressly enacts a law doing so:

Indeed, the practical interpretation put by Congress upon the Constitution has been long continued and uniform to the effect 279*279 that the Constitution is applicable to territories acquired by purchase or conquest only when and so far as Congress shall so direct. Notwithstanding its duty to “guarantee to every State in this Union a republican form of government,” Art. IV, sec. 4, by which we understand, according to the definition of Webster, “a government in which the supreme power resides in the whole body of the people, and is exercised by representatives elected by them,” Congress did not hesitate, in the original organization of the territories of Louisiana, Florida, the Northwest Territory, and its subdivisions of Ohio, Indiana, Michigan, Illinois and Wisconsin, and still more recently in the case of Alaska, to establish a form of government bearing a much greater analogy to a British crown colony than a republican State of America, and to vest the legislative power either in a governor and council, or a governor and judges, to be appointed by the President. It was not until they had attained a certain population that power was given them to organize a legislature by vote of the people. In all these cases, as well as in Territories subsequently organized west of the Mississippi, Congress thought it necessary either to extend the Constitution and laws of the United States over them, or to declare that the inhabitants should be entitled to enjoy the right of trial by jury, of bail, and of the privilege of the writ of habeas corpus, as well as other privileges of the bill of rights.

[Downes v. Bidwell, 182 U.S. 244, 278-279 (1901);

SOURCE: https://scholar.google.com/scholar_case?case=9926302819023946834]

The ONLY way around the Unconstitutional Conditions Doctrine that allows the government to deliver a service NOT authorized by the constitution in states of the Union and to raise revenue to PAY for the service is therefore to pay for the service with funds collected BEFORE the payment is received and not AFTER or as PART of the benefit payment. This is why:

- Social Security is identified as taxable only to aliens per 26 U.S.C. §871(a)(3) in the case of ONLY “nonresident aliens”. How do we know this? Because:

1.1. IRS represents FDAP in 26 U.S.C. §871(a) as a tax on the GROSS AMOUNT and it would be an unconstitutional direct tax if it pertained to non-privileged people in the states of the Union.

1.2. The top of the Schedule NEC requires a tax treaty and American nationals don’t have one and CAN’T have one.

1.3. The bottom on the Schedule NEC pertains only to aliens in 26 U.S.C. §871(a)(2). - Social Security benefits are on the Schedule NEC instead of the main form 1040NR. Thus, they only pertain to American nationals abroad or aliens but not American nationals at home. You aren’t ALLOWED as an American national to even PUT it on the regular 1040NR. There is no place to write it, because its NOT taxable to an American national filing NRA, even though its one of very few real U.S. sources.

- Ironically, the main 1040NR form Effectively Connected section asks you to attach the SSA-1042-S even though you can’t enter the benefits in this section.

Evidence supporting that last item is below:

For further details on the Unconstitutional Conditions Doctrine, see:

Government Instituted Slavery Using Franchises, Form #05.030, Section 28.2

https://sedm.org/Forms/05-MemLaw/Franchises.pdf

For an example of how to apply the Unconstitutional Conditions Doctrine of the U.S. Supreme Court to challenging income taxation enforcement within states of the Union against American nationals residing there, see:

Microsoft Copilot: Unconstitutional Conditions Doctrine applied to Federal and State Income Taxation, FTSIG

https://ftsig.org/microsoft-copilot-unconstitutional-conditions-doctrine-applied-to-federal-and-state-income-taxation/

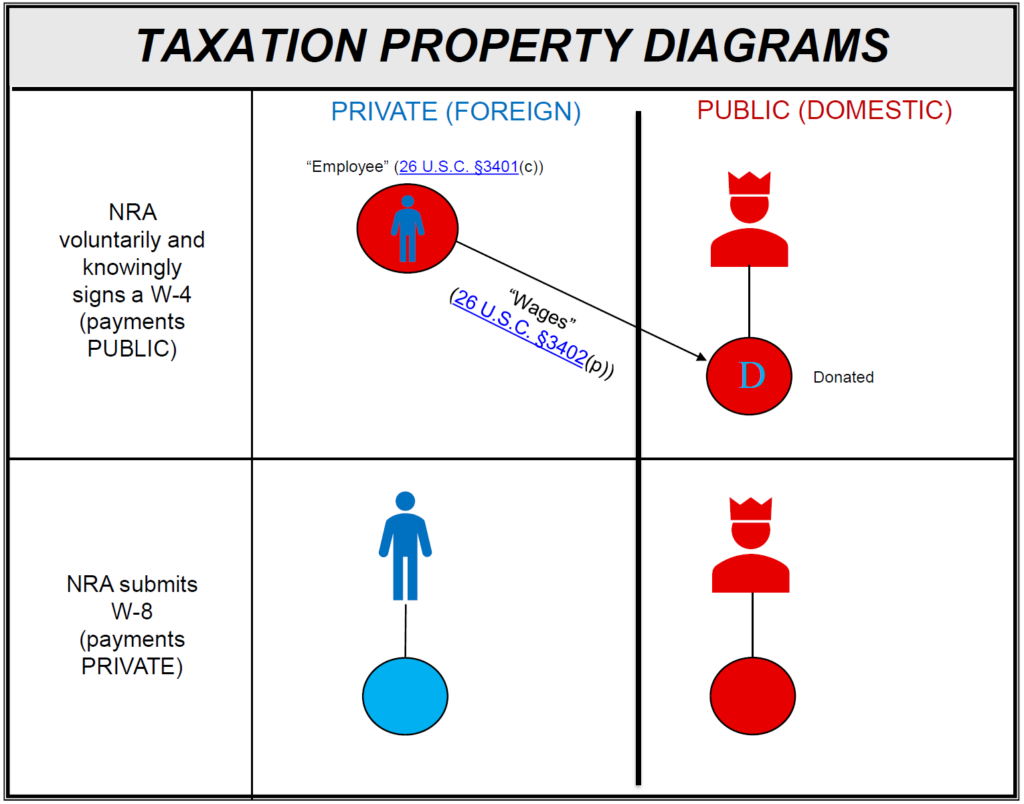

4. Diagrams

The following diagram from Property View of Income Taxation, Form #12.046 (OFFSITE LINK) shows how the exercise of your right to contract or associate can result in:

- The status of your PRIVATE earnings from labor to PUBLIC property that can be regulated and taxed.

- Your receipt of PUBLIC property that can give rise to an obligation on your part.

5. 26 U.S.C. 871(a): Not Effectively Connected (NEC)

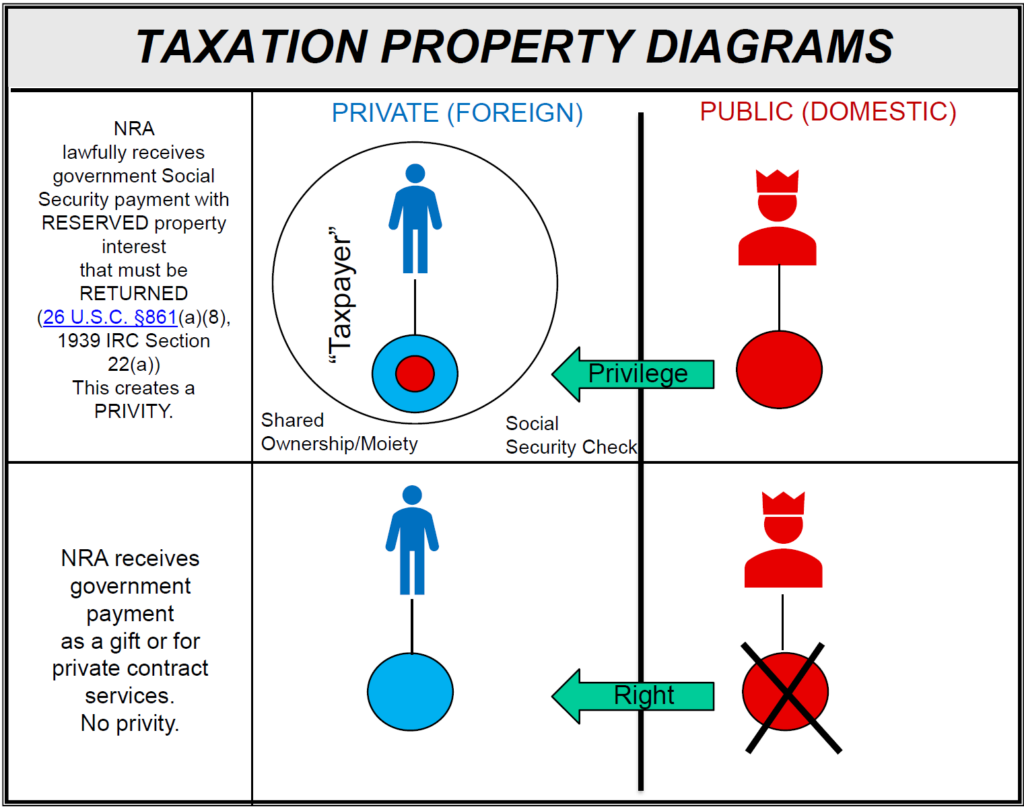

Income that is “Not Effectively Connected (N.E.C.)” under 26 U.S.C. §871(a) goes on Schedule NEC when one files a 1040-NR tax return. This has to be a government payment that the government reserves a PROPERTY interest in AFTER it is received, such as Social Security (26 U.S.C. §861(a)(8)) but which is NOT “effectively connected” by an ELECTION on your part. Social Security, for instance, goes on Schedule NEC instead of the “effectively connected” section of the 1040NR form.

Below is how the data entered on the Schedule NEC is characterized in a 1040-NR filing described SEDM Form #09.077, Section 7:

- This section contains earnings described in 26 U.S.C. §871(a) that are Not Effectively Connected to the “trade or business” franchise. According to 26 C.F.R. §1.871-1(b), this is a tax on gross receipts. Taxes on gross receipts are taxes on capital and not income derived from capital and thus are direct taxes in relation to American nationals such as me standing on land protected by the constitution. They can still apply, however, to privileged foreign persons, who are not protected by the constitution because they are on land not protected by the constitution such as a territory, possession, or abroad or because they are involved in the foreign affairs functions of Congress. Constitutional “income” in the context of American nationals limits itself to ONLY “profit”. Eisner v. Macomber, 252 U.S. 189, 205-207 (1920). I don’t elect to WAIVE the protections of the constitution or its definition of “income” by assigning my private earnings to this privileged category. See:

https://ftsig.org/faq-what-specific-provision-and-status-implements-16a/ - Earnings in this section come ONLY from the statutory geographical “United States” as defined in 26 U.S.C. §7701(a)(9) and (a)(10) and 4 U.S.C. §110(d) or the U.S. government as a federal corporation dispensing privileges to me. It is not within my authority as a private human to ELECT to EXPAND the statutory geographical “United States” to add states of the Union because that would usurp the legislative powers of Congress and the states and violate the separation of powers. Further, 26 C.F.R. §301.7701(b)-2 and 26 C.F.R. §301.7701-7 both recognize that even the “States” listed in 26 U.S.C. §7701(a)(10) and 4 U.S.C. §110(d) are “foreign” with respect to the jurisdiction of the Internal Revenue Code and therefore not within the geographical “United States”. 26 C.F.R. §31.3121(e)-1 and 26 C.F.R. §301.7701(b)-1(c)(2)(ii) concur with this by both recognizing constitutional states (“several states” of “states”) of the Union as legislatively foreign and outside the jurisdiction of Congress by using the lower case “state” in referring to them.

- 26 U.S.C. §871(a) limits itself only to physical “tangibles” and that “intangibles” are only taxed at the domicile of the owner per Union Refrigerator Transit Co. v. Kentucky, 199 U.S. 194, 205 (1905). Since my domicile is WITHOUT the statutory geographical “United States” and I am not representing an artificial entity domiciled there such as a “person”, “individual”, or “U.S. person” engaged in a “trade or business”, then all intangibles under this section are NOT TAXABLE or reportable to the national government. Thus, earnings from my human labor, stocks, bonds, notes, contracts, and even promissory notes such as fiat currency, are NOT taxable to the national government. See the following for proof: https://ftsig.org/meta-ai-proof-that-26-u-s-c-871a-earnings-are-profit-only-and-that-labor-are-not-taxable-under-this-statute/

- Earnings from any place OTHER than the statutory geographical “United States” or the U.S. government as a federal corporation are purposefully excluded under 26 U.S.C. §872, 26 C.F.R. §1.872-2(f). They don’t need to be exempt, because they are excluded from being listed in the schedule NEC. This means all earnings received from geographical sources outside the STATUTORY, but not CONSTITUTIONAL “United States” and not from the U.S. government as a federal corporation are purposefully not listed in this section. This includes all of my earnings, because I do not do business with the U.S. government as a federal corporation or in the statutory geographical “United States”.

- These types of earnings would normally be reported on IRS Form 1042s, which connects the earning to “gross income” per the form instructions. HOWEVER, the instructions for the form say to report “gross income” not “trade or business” income as required by 26 U.S.C. §6041(a) and thus exceed the authority of the statute so the form is ILLEGAL.

- All nonzero amounts contained in this section shall constitute a donation for the purpose of reimbursing the Recipient for the cost of processing this return. I want to avoid ever being a “public charge” upon any government. As a trustee, God commands me to be responsible for all the services and work that I create or demand from others, because if I don’t, I’ll injure them.

- Because a donation is involved here and because I owe you nothing that I didn’t donate for this time period, then I am the only one who can define the terms of our relationship as the Merchant/Seller under U.C.C. §2-104(1). On this subject, the U.S. Supreme Court held: “It is hardly lack of due process for the Government to regulate that which it subsidizes.” Wickard v. Filburn, 317 U.S. 111 (1942). This requirement goes BOTH ways under the concept of equal protection and equal treatment, so I am doing the subsidizing and regulating in this case. These considerations create the obligations described in Injury Defense Franchise and Agreement; https://sedm.org/Forms/06-AvoidingFranch/InjuryDefenseFranchise.pdf. These obligations merely ensure that you do not use any of my personal information for a commercial purpose that benefits anyone but me and that you leave me alone (justice) and stop trying to steal God’s property that I am in stewardship of through deception and words of art.

Earnings under 26 U.S.C. §871(a)(1)(A) are called FDAP. For IRS’ view on what is included in FDAP, see:

Fixed, determinable, annual, or periodical (FDAP) income, IRS

https://www.irs.gov/individuals/international-taxpayers/fixed-determinable-annual-or-periodical-fdap-income

The reader should be aware that the above article is NOT court admissible evidence of anything. Click here for the reason.

Also, FDAP is characterized in 26 U.S.C. §871(a)(1)(A) as:

“and other fixed or determinable annual or periodical gains, profits, and income,”

IRS interprets the above to mean GROSS RECEIPTS, even though the constitutional definition of “income” means PROFIT. A GROSS RECEIPTS tax is a DIRECT tax on PRIVATE PROPERTY that would be unconstitutional for those standing on land protected by the constitution. To be constitutional and properly characterizable as a lawful excise, the property must be EITHER:

- Earned by a privileged alien not standing on land protected by the constitution OR

- PUBLIC property. It would only be PUBLIC property if:

2.1. It was PAID (sourced from) the national government and a reserved statutory property interest was retained prior to payment. An example of this would be Social Security in 26 U.S.C. §871(a)(3). OR

2.2. It was RECEIVED by a CIVIL “U.S. person” as the OWNER of the payment, which is a creation and property of the national government.

Although 26 U.S.C. §871(a)(1)(A) lists “compensation” as FDAP, this is indicative of “compensation for services” found in 26 U.S.C. §61, which is services (not labor) provided by an artificial entity for profit. E.G. Kelly Girl. If the taxpayer is domestic, the owner of the labor is not private or constitutionally protected. The taxability of the human labor of the statutory “taxpayer” is further discussed in:

- Foreign Remedies->Involuntary Taxation of Your Own Labor, FTSIG

https://ftsig.org/category/foreign-remedies/government/involuntary-taxation-of-your-own-labor/ - PROOF OF FACTS: That my earnings from labor on a 1040-NR tax return are not taxable, FTSIG

https://ftsig.org/proof-of-facts-that-my-earnings-from-labor-on-a-1040-nr-tax-return-are-not-taxable/ - PROOF OF FACTS: Proof that Your Human Labor May Not Lawfully Appear as Income on Your 1040NR Tax Return Without Your Consent, FTSIG

https://ftsig.org/proof-of-facts-proof-that-your-human-labor-may-not-lawfully-appear-as-income-on-your-1040nr-tax-return/ - Proof that Involuntary Income Taxes on Your Labor are Slavery, Form #05.055

https://sedm.org/Forms/05-MemLaw/ProofIncomeTaxLaborSlavery.pdf

6. 26 U.S.C. 871(b) Effectively Connected (1040-NR main form)

6.1. Definition

“Effectively connected” is only used in the context of “nonresident aliens”. The only position this site takes is the Nonresident Alien Position. The definition of “effectively connected” is as follows:

26 U.S. Code § 864 – Definitions and special rules

(c)Effectively connected income, etc.

(1)General rule

For purposes of this title—

(A) In the case of a nonresident alien individual or a foreign corporation engaged in trade or business within the United States during the taxable year, the rules set forth in paragraphs (2), (3), (4), (6), (7), and (8) shall apply in determining the income, gain, or loss which shall be treated as effectively connected with the conduct of a trade or business within the United States.

(B) Except as provided in paragraph (6) [1] (7), or (8) or in section 871(d) or sections 882(d) and (e), in the case of a nonresident alien individual or a foreign corporation not engaged in trade or business within the United States during the taxable year, no income, gain, or loss shall be treated as effectively connected with the conduct of a trade or business within the United States.

The above is not really a definition, because it doesn’t explain the PURPOSE of “effectively connecting” and WHO actually DOES IT, which is YOU and not THEM if you are an American national. That purpose of “effectively connecting” is to donate PRIVATE property to a PUBLIC use, a PUBLIC office, and a PUBLIC purpose through an election. If they told you that was the purpose, you wouldn’t “effectively connect” ANYTHING called “income”! This remarkable fact is exhaustively analyzed in the following memorandum of law:

The Truth About “Effectively Connecting, Form #05.056

https://sedm.org/Forms/05-MemLaw/EffectivelyConnected.pdf

The reason you as an NRA50 American national are the ONLY one who can “effectively connect” is that the OWNER of the property has to give consent to do so if they are PRIVATE and protected by the Constitution. Note that under the laws of property, ownership and control are substantially synonymous. Any attempt to convert PRIVATE property AFTER IT IS RECEIVED from PRIVATE to PUBLIC is an attempt to exercise control and ownership over the property, which only the owner can do. Thus, the RECIPIENT and OWNER of a payment cannot be PRIVATE and constitutionally protected, and yet at the SAME time, be subject to third party attempts to change the status of the payment he or she owns from PRIVATE to PUBLIC. That would be a THEFT of property or rights to property.

So if anyone OTHER than YOU the NRA50 American national PRIVATE owner of the payment changes the status of the payment or assigns a PUBLIC status such as “effectively connected”, tries to control or regulate it, or takes or reserves a portion of it for themselves without your consent or knowledge, they are STEALING and violating the Fifth Amendment Takings Clause. A “nonresident alien” is NOT a public status GENERALLY or ALWAYS, but a the following SUBSETS of the “nonresident alien” status are ALWAYS PUBLIC by virtue ONLY of alienage and the foreign affairs functions of Congress under Article 1, Section 8, Clause 3:

- “Non-resident alien” in 26 U.S.C. §874. See:

1.1. DEFINITION: “non-resident alien”, FTSIG

https://ftsig.org/non-resident-alien/

1.2. META AI: “Nonresident Alien” v. “non-resident alien”, FTSIG

https://ftsig.org/meta-ai-nonresident-alien-v-non-resident-alien/ - An NRAAlien residing and domiciled outside United States* the country but doing business in the United States* the country and receiving revenue from said activities as a foreign affairs function under Article 1, Section 8, Clause 3 of the constitution and who makes a “closer connection election” associating with their constitutional state, territory, or possession instead of the United StatesGov under 26 C.F.R. §301.7701(b)-2(d) by filing a 1040NR and Form 8840.

The above PUBLIC statuses, however, are not true of an NRA50 American national because they are protected by the Constitution and have a PRIVATE civil status as PRIVATE property. Thus, Congress has no control or ownership over the status they invoke as a “nonresident alien” under 26 U.S.C. §7701(b)(1)(B) and it is not a PUBLIC status. Thus, NRA50 American national as a PRIVATE party CANNOT lawfully:

- Engage in a “trade or business” without a voluntary election.

- Render the “personal services” that are the basis of a “trade or business in the United States” in 26 U.S.C. §864(b). “personal services” are services as a privileged fictional “person” under 26 U.S.C. §6671(b) and 7343 rendered as as an agent and franchisee of the national government. Otherwise, said services would be private, constitutionally protected, and not subject to taxation or regulation. This is NOT the same “person” as that described in 26 U.S.C. §7701(a)(1), who can be anyone who files a tax form, whether they have a tax obligation or not.

The above considerations are why YOU as an NRA50 PRIVATE American national protected by the Constitution are ONLY one who can:

- Decide whether to enter “income” (which by default is PRIVATE PROPERTY) on the 1040-NR form and

- Decide whether you want to take “trade or business” deductions against it under 26 U.S.C. §162. You only need deductions if you were DUMB enough to convert your PRIVATE earnings from PRIVATE to PUBLIC by entering them on the 1040-NR “effectively connected” section to begin with.

- Claim a breach of constitutional/private rights under the constitution and common law INSTEAD of civil statutory law if Congress tries to control, tax, regulate, or change the status of you or your property from PRIVATE to PUBLIC.

The following regulation deals with what is connected to a “trade or business” in the case of a nonresident alien:

26 C.F.R. §1.871-8 – Taxation of nonresident alien individuals engaged in U.S. business or treated as having effectively connected income.

https://www.law.cornell.edu/cfr/text/26/1.871-8

“Effectively connecting” in 26 U.S.C. §864(c) implements the following provisions for converting PRIVATE to PUBLIC expressly identified by the U.S. Supreme Court:

“When Sir Matthew Hale, and the sages of the law in his day, spoke of property as affected by a public interest, and ceasing from that cause to be juris privati solely, that is, ceasing to be held merely in private right, they referred to

[1] property dedicated [DONATED] by the owner to public uses, or

[2] to property the use of which was granted by the government [e.g. Social Security Card], or

[3] in connection with which special privileges were conferred [licenses].

Unless the property was thus dedicated [by one of the above three mechanisms], or some right bestowed by the government was held with the property, either by specific grant or by prescription of so long a time as to imply a grant originally, the property was not affected by any public interest so as to be taken out of the category of property held in private right.”[. . .]

“The compensation which the owners of property, not having any special rights or privileges from the government in connection with it, may demand for its use, or for their own services in union with it, forms no element of consideration in prescribing regulations for that purpose.

[. . .]

“It is only where some right or privilege [which are GOVERNMENT PROPERTY] is conferred by the government or municipality upon the owner, which he can use in connection with his property, or by means of which the use of his property is rendered more valuable to him, or he thereby enjoys an advantage over others, that the compensation to be received by him becomes a legitimate matter of regulation. Submission to the regulation of compensation in such cases is an implied condition of the grant, and the State, in exercising its power of prescribing the compensation, only determines the conditions upon which its concession shall be enjoyed. When the privilege ends, the power of regulation ceases.”

[Munn v. Illinois, 94 U.S. 113, 139-140 (1876);

SOURCE: https://scholar.google.com/scholar_case?case=6419197193322400931]

In the case of “effectively connecting” under 26 U.S.C. §864(c), it converts at least a PORTION of the proceeds from PRIVATE to PUBLIC by associating it with some “benefit”/consideration so they can tax or regulate it.

- THIS is accomplished when you effectively connect things voluntarily when you don’t need to:

“[1] property dedicated [DONATED] by the owner to public uses, or “ - THIS is accomplished when you attach accept or use government benefits or property, such as a CIVIL status of “U.S. person”:

“[2] to property the use of which was granted by the government [e.g. Social Security Card or “U.S. person” status they created and own], “ - THIS is done with deductions as an NRA Alien only who already owed the tax as a privileged party:

“[3] in connection with which special privileges were conferred [licenses].” See 26 C.F.R. §301.6109-1(b), which creates a presumption that the item of income is “effectively connected” if you use it in connection with a Taxpayer Identification Number (TIN). The TIN is the functional equivalent of a LICENSE.

The reason the government wants you to connect your property or earnings to a “trade or business” (defined as “the functions of a public office” in 26 U.S.C. §7701(a)(26)) is because they are implementing a franchise, and all franchises are implemented with “excise taxes” and result in a “public office”:

“Is it a franchise? A franchise is said to be a right reserved to the people by the constitution, as the elective franchise. Again, it is said to be a privilege conferred by grant from government, and vested in one or more individuals, as a public office. Corporations, or bodies politic are the most usual franchises known to our laws.”

[People v. Ridgley, 21 Ill. 65, 1859 WL 6687, 11 Peck 65 (Ill., 1859)]

That “public office” is the “U.S. person” in 26 U.S.C. §7701(a)(30) OR the “person” in 26 U.S.C. §6671(b) (civil enforcement) and 26 U.S.C. §7343 (criminal enforcement). If you didn’t do a “U.S. person” election, then the “person” in 26 U.S.C. §6671(b) (civil enforcement) and 26 U.S.C. §7343 (criminal enforcement) was never lawfully created and the only thing they can reach is your property and not you.

6.2. THREE types of EC: Involuntary, Optional, and Mistaken

There are three methods of Effectively Connecting as indicated in the following subsections.

6.2.1. INVOLUNTARY:

This happens with nonresident aliens who:

1. Are currently receiving deferred payments that they previously effectively connected. 26 U.S.C. §864(c)(6). Note that such payments DO not include privileged retirement earnings, for instance, earned in previous years where you filed as a U.S. person.

2. Effectively connected their real property previously but stopped doing so and continue to receive income from it up to 10 years after they stopped. 26 U.S.C. §864(c)(7), 26 U.S.C. §871(d), and 26 U.S.C. §882(d).

3. Had income from sale of partnership interests by NRAAliens. 26 U.S.C. §864(c)(8)

4. Work for the U.S. government as a REAL public officer under Titles 5, 10, or 50. Earnings from these sources are “effectively connected” by law under 26 U.S.C. §864(c). See:

4.1. Foreign Tax Status will NOT eliminate income tax obligations for Government Employees, FTSIG

https://ftsig.org/foreign-tax-status-will-not-eliminate-income-tax-obligations-for-government-employees/

4.2. Microsoft Copilot: Do real “public officers” in Titles 5 and 10 of the U.S. Code always owe tax?, FTSIG

https://ftsig.org/microsoft-copilot-do-real-public-offices-in-titles-5-and-10-of-the-u-s-code-always-owe-tax/

6.2.2. OPTIONAL:

This happens with aliens abroad who have 26 U.S.C. §871(a) Schedule NEC income who want to reduce it by voluntarily EC’ing that income. The Schedule NEC rate is 30% but the rate is usually lower in the average income bracket for most Americans at 23%. See:

1040NR Attachment, Form #09.077, Section 2.2.10, Items 7 and 8

https://sedm.org/Forms/09-Procs/1040NR-Attachment.pdf

Aliens abroad are POLITICALLY foreign and CIVILLY foreign. They have no constitutional rights and are subject to the foreign affairs functions of Congress under Article 1, Section 8, Clause 3. Thus, they are privileged and “taxpayers” WITHOUT any kind of election merely by doing business in our country. They can’t AVOID income tax, but they can REDUCE the damage with an EC election.

Those who do business with these people in the states of the Union are LIABLE to withhold under 26 U.S.C. §1461 and 26 C.F.R. §1.1441-1. Thus, these NRAAliens have to file the 1040NR to get their withholdings back. They are also often subject to tariffs when doing business in our country.

6.2.3. MISTAKEN:

This happens with anyone:

- Standing on land protected by the Constitution. ..AND

- NOT already serving as a legitimate public officer under Titles 5, 10, or 50 of the U.S. Code. . . AND

- Who files as a nonresident alien. . .AND

- Who put any earnings on the 1040NR form or Schedule NEC at all.

They have a PRIVATE status by default and are not subject to federal civil statutory law unless they work directly for the government. Thus, federal preemption doesn’t operate on them or their property under the separation of powers unless they make an election. By mistakenly “effectively connecting”, they:

- Unknowingly engage in INVISIBLE consent as documented below through their ACTIONS without knowing it.

Invisible Consent, FTSIG

https://ftsig.org/how-you-volunteer/invisible-consent/ - Unwittingly volunteer to become lawful targets of IRS enforcement under 26 U.S.C. §6671(b) and 26 U.S.C. §7343 as someone engaging in “personal services” in 26 U.S.C. §864(b).

Why? Because “effectively connecting” connects them to a “trade or business within the United States” under 26 U.S.C. §864(b) as an officer of the national government engaged in “personal services”, meaning services as a privileged CIVIL “person” working FOR FREE for the national government handling PUBLIC property until it is “returned” to its rightful owner by filing a “return”. This amazing fact is further proven below:

Microsoft Copilot: Meaning of civil statutory “services”, FTSIG

https://ftsig.org/microsoft-copilot-meaning-of-civil-statutory-services/

The property they manage as an unwitting public officer volunteer is the property they DONATED to Uncle Sam by mistakenly “effectively connecting”. Government can’t make the donation and CONSENT EXPLICIT and INFORMED, because if you knew that’s what you were doing and the circumstances under which you did it, you would STOP volunteering in a HEARTBEAT.

YOUR PRIVATE/FOREIGN IDENTITY AS A CONSTITUTIONAL “PERSON”: Those who work for or do business with non-governmental people and businesses are protected by the Constitution still remain private and foreign without an election in the context of said commerce. The services (what we call “civil services” on this website) the income tax pays for are not expressly authorized by the constitution so they are being offered in a purely private capacity by the national government under the Clearfield Doctrine in which the government acts as a Merchant (U.C.C. §2-104(1)) and you act as a Buyer (U.C.C. §2-103(1)(a)) under the U.C.C. If you don’t join the corporation as an NRA50 in your PRIVATE life, you don’t owe the private dues. It would violate the separation of powers to force you to participate and contract with them, since the income tax is “quasi-contractual” and the IRS is acting in a purely private commercial capacity. That would be an impairment of your private right to contract or not contract in violation of Article 1, Section 10 and constitute IDENTITY THEFT.

YOUR PUBLIC/DOMESTIC/INTERNAL/GOVERNMENT IDENTITY AS A CIVIL “PERSON”: Your government paycheck or Social Security payment is paid to the PRIVILEGED PUBLIC OFFICE or STATUS you represent while ON DUTY and not you as a PRIVATE constitutional “person” you are when off duty. Thus, Uncle Sam remains the absolute PUBLIC owner of the paycheck AFTER you received it and can demand a “recapture” or portion of it be “returned” to him to settle accounts. That is how all excise taxes work: As a rental fee on the public office or status you consensually occupy. As such, they are outside the reality of constitutional taxation, because they are just a property rental fee for the civil statuses that Congress legislatively creates and therefore owns as public property under Article 4, Section 3, Clause 2 of the Constitution. We discuss this further in:

Journey to Sixteenth Amendment, Fed Reserve

Sixteenth Amendment is IRRELEVANT to the Current I.R.C. Subtitles A and C, Section 8

https://ftsig.org/history/journey-to-16a-fed-reserve-nnot/#8._Sixteenth

It is perfectly lawful as the ONLY real “tax” they can collect, because they do it CONSENSUALLY. You don’t HAVE to occupy a public office to survive, but if you decide you want to do so, you have to pay the “rent” on the office. This website does not challenge the obligation to pay taxes for those who work as public officers for the government for the reasons explained below:

- Foreign Tax Status will NOT eliminate income tax obligations for Government Employees, FTSIG

https://ftsig.org/foreign-tax-status-will-not-eliminate-income-tax-obligations-for-government-employees/ - Microsoft Copilot: Do real “public officers” in Titles 5 and 10 of the U.S. Code always owe tax?, FTSIG

https://ftsig.org/microsoft-copilot-do-real-public-offices-in-titles-5-and-10-of-the-u-s-code-always-owe-tax/

WHO CAN MAKE THIS MISTAKE?:

1. Most of these people are PRIVATE American nationals from anywhere in the COUNTRY who usually had tax illegally withheld that they must file to get back. They can’t put anything on the Schedule NEC, because its only for aliens. So they try to write some part of their earnings on the 1040NR mistakenly usually out of fear or legal ignorance.

2. It can also include aliens in states of the Union, territories, or possessions if they file as NRAAliens and include Form 8840 with their filing to have a closer connection with the locality they reside in than the national government under 26 C.F.R. §301.7701(b)-2.

| WARNING: If you DON”T indicate you are protected by the constitution in your tax return, the IRS will NOT infer it from your mailing address. They will exploit every possible opportunity to make presumptions about your status that favor them economically. Thus, by your omissions, you will lose: 1. The constitutional protections against direct taxes and gross receipts on your earnings under Article 1, Section 2, Clause 3 and Article 1, Section 9, Clause 4. See: https://ftsig.org/history/constitutional-provisions-123-194/ 2. The protections of the Unconstitutional Conditions Doctrine, which forbids extorting a KICKBACK of proceeds from government payments. See: Government Instituted Slavery Using Franchises, Form #05.030, Section 28.2 https://sedm.org/Forms/05-MemLaw/Franchises.pdf 3. The protections of the Fifth Amendment for private property. |

6.3. Why Involuntary Effectively Connected Income is a SCAM for American Nationals

We began this article in section 1 by discussing methods by which your earnings become INVOLUNTARILY Effectively Connected Income, and thus, are converted from PRIVATE to PUBLIC WITHOUT your express consent merely by some external circumstance you don’t control directly. We listed those provisions as follows:

- 26 U.S.C. §864(c)(6): Treatment of certain deferred payments.

- 26 U.S.C. §864(c)(7): Treatment of certain real property transactions. Requires you to ECI sale of property up to ten years after you stopped ECI’ing earnings from it.

- 26 U.S.C. §864(c)(8): Gain or loss of foreign persons from sale or exchange of certain partnership interests. Determines profit or loss from sale of partnership based on fair market value at time of sale as if it were Effectively Connected.

- Federal Investment in Real Property Transfer Act (FIRPTA)

4.1. 26 U.S.C. §871(d): Election to treat real property income as income connected with “trade or business”.

4.2. 26 U.S.C. §882(d): Election to treat real property income as income connected with “trade or business”. - 26 U.S.C. §882(e): Interest on United States Obligations Received by Banks Organized in Possessions.

The purpose of the above provisions are to take OUT OF YOUR HANDS the decision of whether you want to treat specific earnings as Effectively Connected Income and put it under the control of Uncle Sam as PUBLIC property. The underlying presumption in listing all the above is that everything listed constitutes a privilege and consideration that has commercial value, which happened in the past, and that you have a DUTY to “Effectively Connect” FUTURE earnings to pay for delivering the privilege. In other words, pursuing those privileges created a FUTURE debt that allegedly applies LONG AFTER you abandon “U.S. person” status. That obligation does not attach to the “nonresident alien” status, but to the “nonresident alien INDIVIDUAL” status under 26 U.S.C. §864(a), which you have a right not to adopt if you are not PRESENTLY pursuing privileges.

In reality, however, there is no NET or REAL CONSIDERATION or privilege involved that you should feel a duty to pay for as an American national because:

- There is no liability statute for anything but withholding agents on ALIENS in 26 U.S.C. §1461, which you are not, at least within a constitutional state.

- The entire Internal Revenue Code in actuality:

2.1. Delivers no “PRIVILEGES” but only OBLIGATIONS. Deductions reduce taxable income, but there is not such thing as income for an American national not receiving government payments.

2.2. Doesn’t apply within the exclusive jurisdiction of constitutional states to American nationals who make no “elections”.

2.3. Is implemented as a taxable franchise using the SSN as a de facto license, which the U.S. Supreme Court said cannot even lawfully be offered in a constitutional state per the License Tax Cases. - Even if you thought you had “taxable income”, nearly all of it was excluded and actually nontaxable anyway.

- Because you had no real taxable income, you didn’t need privileged “trade or business” deductions or Effectively Connected Income (ECI) anyway.

So the idea that you are receiving REAL, MEASURABLE consideration or commercial benefit from the government through the Internal Revenue Code that you must reimburse them for is all a ruse, at least in the case of American nationals who are nonresident aliens not receiving government payments.

For thus says the Lord: “You have sold yourselves for nothing [no real/tangible “benefit”], And you shall be redeemed without money.”

[Isaiah 52:3, Bible, NKJV]

In fact:

- If you put the government on the spot and MANDATED that they had the burden of proving that they IN ACTUALITY delivered REAL QUANTIFIABLE consideration of an EQUAL value to what you paid them, they would fail miserably if all things on this website were taken into account.

1.1. They avoid this burden of proof by shifting it to YOU to prove you DIDN’T receive consideration. They do this by calling the income tax a “quasi-contract”.

1.2. That puts YOU in the position of proving a NEGATIVE, which is that you DIDN’T receive consideration in order to prove that you are NOT a party to that “quasi-contract”. This is called “failure of consideration”. - The GOVERNMENT are therefore the only ones who in actuality are PRIVILEGED, because they deceived you out of donating your private property without providing EQUAL consideration as mandated by the Fifth Amendment. See:

Why Government is the Only Real Beneficiary of All Government Franchises, Form #05.051

https://sedm.org/product/why-the-government-is-the-only-real-beneficiary-of-all-government-franchises-form-05-051/ - Government is the only real beneficiary of everything they do. They pay money ONLY to their offices, and not to the private people occupying them. Paying private people would be an abuse of their taxing power in fact.

The Government “Benefits” Scam, Form #05.040** (Member Subscriptions)

https://sedm.org/product/the-government-benefits-scam-form-05-040/ - Income from “U.S. sources” includes only the government/PUBLIC/DOMESTIC/INTERNAL, and most people don’t earn this anyway. See:

PROOF OF FACTS: “U.S source” does NOT include anything but payments DIRECTLY from the government and excludes even payments from “taxpayers”, FTSIG

https://ftsig.org/proof-of-facts-u-s-source-does-not-include-anything-but-payments-directly-from-the-government-and-excludes-even-payments-from-taxpayers/

The way OUT of this Ponzi Scheme scam is simply to reject any and all privileges, and use your property to make them privileged like they do to you. If you don’t, they’ll just keep pretending they are helping you and charge as much as they want in the process and thereby eventually STEAL everything you have and give you nothing you really want in return. Below is an example of how to do that in a tax return filing:

How to Reject All Privileges in a Tax Return Filing, FTSIG

https://ftsig.org/how-to-reject-all-privileges-in-a-tax-return-filing/

Lastly, we aren’t suggesting that “effectively connecting” is NOT legitimate for EVERYONE, but only American nationals. For nonresident aliens who are aliens, for instance, they are the the only parties really liable for anything under 26 U.S.C. §1461 as a foreign affairs function under Article 1, Section 8, Clause 3. These people sometimes DO need to “effectively connect” in order to REDUCE their lawful tax liability through deductions under 26 U.S.C. §162.

6.4. Traps/Springes on the 1040-NR Effectively Connected Section

People filing the 1040NR naively think that by entering “income” in the “effectively connected” portion of the 1040NR, they are obtaining the ability to REDUCE their tax liability by taking “trade or business” deductions under 26 U.S.C. §162. However, something much more sinister is happening here.

The “effectively connected” section of the 1040NR is also used to list “income” such as “wages” from the W-2 in Block 1a of the 1040NR.

- The 1040NR Instructions say to ONLY enter as “wages” that which is “Effectively Connected” AND that you are the only one who can decide to do so.

- 26 U.S.C. §871(a), which is the Not Effectively Connected list of taxable items, does NOT include earnings from human labor, but only GROSS RECEIPTS of an alien from sales transactions.

Therefore, if you enter earnings from the W-2 on the 1040NR form in the “effectively connected” section, you are converting your PRIVATE labor to a PUBLIC use, and thus VOLUNTEERING to be an uncompensated civil statutory “employee” working for Uncle Sam for free! Putting your PRIVATE earnings from labor on the form makes the ENTIRE amount “income” even though it wouldn’t otherwise be, and thus, makes the income tax a “gross receipts” tax on PROPERTY, rather than merely on PROFIT. That is unconstitutional without at least your consent, unless you make an election to “effectively connect” it to make it taxable under 26 U.S.C. §864.

Why the HELL would anyone in their right mind ever want to enter ANYTHING having to do with their human labor on the 1040NR form block 1a under “wages” and thus VOLUNTARILY become a SLAVE? The only reason we can think of is that they are operating out of legal ignorance and the fear it produces. You as a user of this website are FORBIDDEN from doing this and violate our Member Agreement if you do it. It’s pure stupidity and no different than a lemming jumping off the cliff. And doing this is the ONLY reason most people would even believe they needed privileged “trade or business” deductions to begin with.

The regulations governing the submission of withholding agreements agree with these conclusions.

26 C.F.R. § 31.3402(p)-1 – Voluntary withholding agreements.

§ 31.3402(p)-1 Voluntary withholding agreements.

(a) Employer-employee agreement.

An employee and his employer may enter into an agreement under section 3402(p)(3)(A) to provide for the withholding of income tax upon payments of amounts described in paragraph (b)(1) of § 31.3401(a)-3, made after December 31, 1970. An agreement may be entered into under this section only with respect to amounts which are includible in the gross income of the employee under section 61, and must be applicable to all such amounts paid by the employer to the employee. The amount to be withheld pursuant to an agreement under section 3402(p)(3)(A) shall be determined under the rules contained in section 3402 and the regulations thereunder. See § 31.3405(c)-1, Q&A-3 concerning agreements to have more than 20-percent Federal income tax withheld from eligible rollover distributions within the meaning of section 402.

We must remember, however, that the above regulation is satisfied by merely submitting the W-4, even though it doesn’t identify itself as an “agreement”.

26 C.F.R. § 31.3402(p)-1 – Voluntary withholding agreements.

§ 31.3402(p)-1 Voluntary withholding agreements.

(b) Form and duration of employer-employee agreement.

(1)(i) Except as provided in subdivision (ii) of this subparagraph, an employee who desires to enter into an agreement under section 3402(p)(3)(A) shall furnish his employer with Form W-4 (withholding exemption certificate) executed in accordance with the provisions of section 3402(f) and the regulations thereunder. The furnishing of such Form W-4 shall constitute a request for withholding.

So you aren’t really getting the Constitutionally required “reasonable notice” that you in fact are VOLUNTEERING UNLESS you actually read the statutes and regulations that implement the W-4. If they notified you in the instructions that you were volunteering to make your entire earnings taxable and that you had the right to UNVOLUNTEER somewhere on the W-4, almost no one would do it!

Worst yet, if you decide NOT to “effectively connect” your earnings from labor by transferring W-2 amounts onto the 1040NR “effectively connected” section block 1a, you might ask whether IRS can then add that amount on the Schedule NEC (Not Effectively Connected) without your consent. An examination of that form reveals NO BLOCK for writing in earnings from your labor, because they are NOT subject to income tax if they are NOT “effectively connected”, meaning VOLUNTARILY DONATED by you to a PUBLIC use, PUBLIC office, and PUBLIC purpose by writing them into block 1a of the 1040NR return!

Note that amounts withheld under Subtitle C for “employment” withholding are merely CREDITS to income taxes owed in Subtitle A AFTER one files a tax return. They are not “taxes” or “treated AS IF” they are “taxes” under Subtitle A and we have found any evidence to support this. In fact, the IRS classifies “wages” and W-2 withholdings as Tax Class 5 GIFTS, not Subtitle A Income Taxes.

If you are compelled to submit a W-4 instead of the more proper W-8 for withholding purposes, upon later filing the 1040NR return, you can still get all the W-2 withholding back, including Social Security deductions. This is because the W-2 withholding is a credit against taxes owed under Subtitle A, and if you owe no taxes, you can get the credit back. You MUST, however, indicate in the refund claim that you were under duress in submitting the W-4 form to the company you work for. If you don’t do this, the amounts reported on the W-2 information return will be treated as government/PUBLIC property and a “federal payment” instead of PRIVATE property. The following form you can file with the 1040-NR allows you to do that:

W-2CC, Form #04.304

https://sedm.org/Forms/04-Tax/3-Reporting/FormW-2CC-Cust/FormW-2CC.pdf

6.5. Defense from the Traps

Note that YOU are the only one who can “effectively connect” your earnings to the privileged “trade or business” excise taxable franchise as indicated by the phrase “by that individual” in 26 C.F.R. §1.871-2(f). NO ONE ELSE can do that. The reason is that you are the owner of yourself and your property and therefore the ONLY one who can lawfully CONSENT to CONVERT or DONATE or DEROGATE that PRIVATE property to a PUBLIC USE, a PUBLIC OFFICE, and a PUBLIC PURPOSE by “effectively connecting” it. This was acknowledged by the U.S. Supreme Court when they held:

“Men are endowed by their Creator with certain unalienable rights,-‘life, liberty, and the pursuit of happiness;’ and to ‘secure,’ not grant or create, these rights, governments are instituted. That property [or income] which a man has honestly acquired he retains full control of, subject to these limitations:

[1] First, that he shall not use it to his neighbor’s injury, and that does not mean that he must use it for his neighbor’s benefit [e.g. SOCIAL SECURITY, Medicare, and every other public “benefit”];

[2] second, that if he devotes it to a public use, he gives to the public a right to control that use; and

[3] third, that whenever the public needs require, the public may take it upon payment of due compensation.”

More on the “trade or business” indirect excise taxable franchise that is the VEHICLE for making the donation at:

The “Trade or Business” Scam, Form #05.001 (OFFSITE LINK)

https://sedm.org/Forms/05-MemLaw/TradeOrBusScam.pdf

Donating your property to the government and thereby CONVERTING it from PRIVATE to PUBLIC is only one of many ways you are deceived into VOLUNTEERING to pay income tax. Other ways are documented in:

How American Nationals Volunteer to Pay Income Tax, Form #08.024 (OFFSITE LINK)

https://sedm.org/Forms/08-PolicyDocs/HowYouVolForIncomeTax.pdf

6.6. Sample Statement to Attach to 1040-NR return relating to “Effectively Connected” Blocks

The following narrative comes form the 1040-NR Attachment, Form #09.077, Section 5 relating to the “effectively connected” section of the 1040-NR form:

1. See definition of “effectively connected” later in section 11.

2. This section contains earnings described in 26 U.S.C. §871(b) from “sources within the United States” and is limited to earnings voluntarily associated with the “trade or business” excise taxable franchise defined as “the functions of a public office” in 26 U.S.C. §7701(a)(26). Everything listed in this section is subject to “trade or business” deductions under 26 U.S.C. §162. “United States” in this context means the government as a corporation, and not a geography. 26 C.F.R. §1.871-2(f) indicates that I am the only one who can “effectively connect” earnings in this section (“by that individual”). Thus, you have no authority to add ANYTHING to this section that I myself did not add, and certainly no type of “income”.

3. Values listed in this section are all zero, because:

3.1. The 1040NR Instructions relating to Block 1a (wages) state: “Don’t include any income on line 1a Form 1040-NR that isn’t treated as effectively connected”. Thus, I can’t include any earnings from labor that I don’t consent to donate to a public use in order to procure the “benefit” of deductions”.

3.2. There is no place on the Schedule NEC to enter earnings from my personal labor, thus recognizing that I can only put it on a tax return if I donate it to a public use by “effectively connecting” it.

3.3. Submitter does not consent and has no delegated authority or lawful authority to consent to “effectively connect” his/her earnings or him/her self to a statutory “trade or business” or public office either by entering it on the 1040NR form or associating it with a statutory SSN/TIN franchise mark. He/she as the absolute owner of both is the only one authorized by law to do so as required by 26 C.F.R. §1.872-2(f) and as required by the Bill of Rights protecting all his/her private property.

3.4. Earnings are therefore expressly excluded from “gross income” under 26 C.F.R. §1.871-7(a)(4) in this section. It would constitute fraud and possibly a violation of 18 U.S.C. §912 for me to claim otherwise, as proven by: The Trade or Business Scam, https://sedm.org/Forms/05-MemLaw/TradeOrBusScam.pdf.

3.5. I rely on the fact that as a non-privileged American national, no one but me can “effectively connect” my earnings to a “trade or business” and I DO NOT consent to do so per the following incorporated by reference: The Truth About “Effectively Connecting”, Form #05.056; https://sedm.org/Forms/05-MemLaw/EffectivelyConnected.pdf

4. Any amounts in this section connected with my personal labor are not listed, such as W-2 earnings, because:

4.1. Earnings from labor are expressly excluded from “wages” under 26 C.F.R. §31.3401(a)(6)-1(b) in the case of income tax and 26 C.F.R. §31.3121(b)-3(c)(1) in the case of Social Security because services were performed outside the statutory geographical “United States” under 26 U.S.C. §7701(a)(9) and (a)(10) and 4 U.S.C. §110(d) and outside the U.S. government (fictional “U.S. Inc. federal corporation”).

4.2 Human labor is property under the protections of the Fifth Amendment Takings Clause. I am filing as a HUMAN BEING protected by the Fifth and Thirteenth Amendment who has not surrendered constitutional protections in exchange for public privileges under the Constitutional Avoidance Doctrine or the Public Rights Doctrine. As the absolute owner of myself, I have the right to exclude any and all others from using or benefitting from the use of my body as private property. Thus, my labor is “EXCLUDED by law” from “gross income” under 26 C.F.R. §1.61-2(a)(1).

4.3. There is not now and never has been a statutory definition of “gross income” under 26 U.S.C. §61 or elsewhere that I have been able to locate which EXPRESSLY includes my private, constitutionally protected human labor that I have not converted to public ownership through some kind of voluntary express election, such as calling my earnings “wages” in 26 U.S.C. §3402(p) or electing any public status such as “U.S. person” under 26 U.S.C. §7701(a)(30), “taxpayer” under 26 U.S.C. §7701(a)(14), “employee” under 26 U.S.C. §3401(c), or “citizen or resident of the United States” in 26 C.F.R. §1.1-1(a). I consent to NOTHING and reject all privileges and benefits connected with these civil statuses and thus retain constitutional protections. Forcing these public civil statuses and the obligations associated with them upon me is an act of criminal identity theft (18 U.S.C. §912), involuntary servitude (Thirteenth Amendment), human trafficking, and a violation of the Fifth Amendment Takings Clause.

4.4. The Recipient therefore has the burden of proving consent to a public civil status that comes with the civil obligations you want to enforce. That burden of proof BEGINS by producing evidence of a EXPRESS voluntary change in the tax status of myself or my property and by reading and rebutting, line by line, the following document under PENALTY OF PERJURY with your full legal birthname as required by 26 U.S.C. §6065: Proof that Involuntary Income Taxes on Your Labor are Slavery, Form #05.055; https://sedm.org/Forms/05-MemLaw/ProofIncomeTaxLaborSlavery.pdf.