Establishing USPI thru laws of property

TABLE OF CONTENTS

- Introduction

- The ORIGIN of PUBLIC/GOVERNMENT Property: “Domestic”/”trade or business within the United States”/”personal services”

- How Congress Lawfully Acquires a PUBLIC/Ownership Interest in Your Private Property: YOUR Consent to Privileges

- An Offer of Privileges/USPI is a Merchant/Buyer Relationship

- Status Elections, Deeming Provisions, and Equivocation: Tools of choice in converting PRIVATE to PUBLIC without your knowledge

- Process to Determine Specific Types of taxable “gross income” in 26 U.S.C. §861

- AVOIDING donating your property to the government and thereby converting it from PRIVATE to PUBLIC

7.1. Summary of All the Methods of Converting from PRIVATE to PUBLIC

7.2. Specific Methods of To Prevent USPI - Relationship between PERSONS and PROPERTY and how they interact

- Comparison of tax terminology of Article 1, Section 8, Clause 3 Taxation to Article 4, Section 3, Clause 2 franchise property rental taxation

1. Introduction

For the purposes of this site, “USPI” stands for United States (government) Property Interest. That interest represents a GOVERNMENT ownership interest in your otherwise PRIVATE property consisting of one or more of the following:

- Qualified: Ownership that is time limited or restricted in its use.

- Moiety: If 50% or more of a thing is owned by one of the owner where ownership is shared.

- Lease or rental: One owner retains the right to exclude others while the lessee has the right to possess and use the property subject to conditions specified in the rental agreement.

- Usufruct: Allows a person to use and enjoy the benefits of someone else’s property without owning it.

The essence of that governmental USPI property interest in your otherwise PRIVATE property is represented by the CIVIL OBLIGATIONS that attach to you or your property. Since the Fifth Amendment forbids the taking of private property for public use without compensation, it stands to reason that whenever CIVIL obligations DO attach to your otherwise private property:

- They attached to the property through a CIVIL legal tax status or civil status by your consent or election, whether implied or explicit. That status comes with BOTH privileges AND obligations inseparably bundled TOGETHER. . . .AND

- You either CONSENTED to those obligations or were at least REIMBURSED for the value of those obligations with some form of PRIVILEGE that has an equal economic value. . . AND

- That the COMPENSATION for the OBLIGATIONS consists of the PRIVILEGES that also attach to the property.

Any approach to taxation that DISREGARDS the above considerations is THEFT, as Judge Andrew Napolitano has correctly claimed. Government HAS to deliver SPECIFIC, PROVABLE EVIDENCE of CONSIDERATION to you in the form of PRIVILEGES that you ASK for and actually RECEIVE in order to have a lawfully enforceable claim and standing in court to recover the cost of delivering those PRIVILEGES to you. They can’t charge you for privileges you DID NOT ask for. That COST of delivery is called OBLIGATIONS above. The following court cases CONFIRM this view:

“A person is ordinarily not required to pay for benefits which were thrust upon him with no opportunity to refuse them. The fact that he is enriched is not enough, if he cannot avoid the enrichment.” Wade, Restitution for Benefits Conferred Without Request, 19 Vand. L. Rev. at 1198 (1966).

[Siskron v. Temel-Peck Enterprises, 26 N.C.App. 387, 390 (N.C. Ct. App. 1975);

SOURCE: https://scholar.google.com/scholar_case?case=12399792881635606458]

“As was said in Wisconsin v. J. C. Penney Co., 311 U.S. 435, 444 (1940), “[t]he simple but controlling question is whether the state has given anything for which it can ask return.”

[Colonial Pipeline Co v Traigle, 421 U.S. 100, 109 (1975);

SOURCE: https://scholar.google.com/scholar_case?case=16559630216409245512]

Thus, EVERY interaction you have with GOVERNMENT must ALWAYS devolve into a equitable exchange of consideration by BOTH parties. WITHOUT that equitable exchange, there can be no valid, enforceable contract or quasi-contract. Recall that the U.S. Supreme Court identifies taxation as “quasi-contractual”. You don’t just BLINDLY PAY money to some fiction of law on the mere PRESUMPTION of a “benefit”. All such presumptions are a violation of due process. Government has to PROVE they delivered real consideration before they have standing to sue you for reimbursement or administratively collect. And you have to ASK for the consideration just like you would from any private business. Recall that government is just a business corporation that delivers only TWO things: CRIMINAL protection and CIVIL protection. CRIMINAL is mandatory, CIVIL is optional and you have to ask for and consent to it either IMPLIEDLY or EXPLICITLY. This is because the CIVIL STATUTORY CODE is a civil protection franchise, just like the income tax. See:

Why Civil Statutory Law is Law for Government and Not Private Persons, Form #05.037

https://sedm.org/Forms/05-MemLaw/StatLawGovt.pdf

Further, if in fact you are in an equitable exchange of CONSIDERATION of equal value on both sides, there can be no “profit or gain”, and thus, no “income” in a constitutional sense. Recall that “income” within the meaning of the constitution means “profit or gain”, and not GROSS RECEIPTS. Thus, you can owe NO TAX on the exchange, even if it is a government payment paid from what the I.R.C. calls a “U.S. source”!

The purpose of establishing government, according to the Declaration of Independence, is the “pursuit of Happiness”, which the U.S. Supreme Court has interpreted to mean the right to absolutely own PRIVATE property.

“We hold these truths to be self-evident, that all men are created equal, that they are endowed by their Creator with certain unalienable Rights, that among these are Life, Liberty and the pursuit of Happiness.[PRIVATE PROPERTY]–That to secure these rights, Governments are instituted among Men, deriving their just powers from the consent of the governed, “

[Declaration of Independence;

SOURCE: http://www.archives.gov/national-archives-experience/charters/declaration.html]

“The provision [Fourteenth Amendment, Section 1], it is to be observed, places property under the same protection as life and liberty. Except by due process of law, no State can deprive any person of either. The provision has been supposed to secure to every individual the essential conditions for the pursuit of happiness; and for that reason has not been heretofore, and should never be, construed in any narrow or restricted sense.”

[Munn v. Illinois, 94 U.S. 113 (1877);

SOURCE: http://scholar.google.com/scholar_case?case=6419197193322400931]

The “pursuit of Happiness” BEGINS with LEAVING THE PROPERTY ALONE and not taxing or regulating its use unless that use demonstrably injures someone. The right to be “left alone”, in fact, is the legal definition of “justice” itself. Therefore, any attempt to disturb you of your property, to tax or regulate it works an INJUSTICE. See:

“The makers of our Constitution undertook to secure conditions favorable to the pursuit of happiness. They recognized the significance of man’s spiritual nature, of his feelings and of his intellect. They knew that only a part of the pain, pleasure and satisfactions of life are to be found in material things. They sought to protect Americans in their beliefs, their thoughts, their emotions and their sensations. They conferred, as against the Government, the right to be let alone – the most comprehensive of rights and the right most valued by civilized men.“

[Olmstead v. United States, 277 U.S. 438, 478 (1928) (Brandeis, J., dissenting);

SOURCE: http://caselaw.lp.findlaw.com/cgi-bin/getcase.pl?court=us&vol=277&invol=438#478; See also Washington v. Harper, 494 U.S. 210 (1990)]

“Justice is the end of government. It is the end of civil society. It ever has been, and ever will be pursued, until it be obtained, or until liberty be lost in the pursuit.”

[The Federalist No. 51 (1788), James Madison;

SOURCE: http://thomas.loc.gov/home/histdox/fed_51.html]

Justice, as a moral habit, is that tendency of the will and mode of conduct which refrains from disturbing the lives and interests of others, and, as far as possible, hinders such interference on the part of others. This virtue springs from the individual’s respect for his fellows as ends in themselves and as his co equals.

[Readings on the History and System of the Common Law, Second Edition, 1925, Roscoe Pound, p. 2;

SOURCE: http://books.google.com/books?id=FrY0AAAAIAAJ&printsec=frontcover]

Any attempt to cause you to give up absolute ownership of your BODY or any part of your private property or control of its use therefore amounts to a conspiracy to make you UNHAPPY if you didn’t EXPRESSLY and KNOWINGLY consent to it. Mere ignorant, indifferent, or even TIMID ACQUIESCENCE is not real, informed consent:

“SUB SILENTIO. Under silence; without any notice being taken. Passing a thing sub silentio may be evidence of consent”

[Black’s Law Dictionary, Fourth Edition, p. 1593]“Qui tacet consentire videtur.

He who is silent appears to consent. Jenk. Cent. 32.”[Bouvier’s Maxims of Law, 1856;

SOURCE: http://famguardian.org/Publications/BouvierMaximsOfLaw/BouviersMaxims.htm]

Consent by mere acquiescence is also called “tacit procuration”:

“Procuration.. Agency; proxy; the act of constituting another one’s attorney in fact. The act by which one person gives power to another to act in his place, as he could do himself. Action under a power of attorney or other constitution of agency. Indorsing a bill or note “by procuration” is doing it as proxy for another or by his authority. The use of the word procuration (usually, per procuratione, or abbreviated to per proc. or p. p.) on a promissory note by an agent is notice that the agent has but a limited authority to sign.

An express procuration is one made by the express consent of the parties. An implied or tacit procuration takes place when an individual sees another managing his affairs and does not interfere to prevent it. Procurations are also divided into those which contain absolute power, or a general authority, and those which give only a limited power. Also, the act or offence of procuring women for lewd purposes. See also Proctor.”

[Black’s Law Dictionary, Fifth Edition, pp. 1086-1087]

The GOVERNMENT defends itself from people imputing “tacit procuration” against them by enacting legislation which MANDATES that all agreements must be in WRITING signed by both parties. YOU should insist on the SAME treatment every time you communicate with THEM:

“Every man is supposed to know the law. A party who makes a contract [or enters into a franchise, which is also a contract] with an officer [of the government] without having it reduced to writing is knowingly accessory to a violation of duty on his part. Such a party aids in the violation of the law.”

[Clark v. United States, 95 U.S. 539, 542 (1877);

SOURCE: https://scholar.google.com/scholar_case?case=17192538030759550245]

The four methods of sharing ownership or control over your private property with the government at the beginning of this article are therefore the methods to:

- IMPLEMENT such UNHAPPINESS and

- VIOLATE the purpose of establishing government according to the Declaration of Independence and

- Turn the government into an ANTI-GOVERNMENT, meaning a government that does the OPPOSITE of what it was created to do.

Former President Taft who proposed the Sixteenth Amendment, got it FRAUDULENTLY ratified, and later as U.S. Supreme Court Chief Justice made it INTERNATIONAL in scope said in the case that did that the following:

“In other words, the principle was declared that the government, by its very nature, benefits the [person who ELECTS the CIVIL STATUTORY FRANCHISE STATUS OF] citizen [on a 1040 Tax form like Cook did] and his property wherever found and, therefore, has the power to make the benefit complete. Or to express it another way, the basis of the power to tax was not and cannot be made dependent upon the situs of the property in all cases, it being in or out of the United States, and was not and cannot be made dependent upon the domicile of the citizen, that being in or out of the United States, but upon his relation [CIVIL FRANCHISE STATUS ELECTION] as citizen to the United States and the relation of the latter to him as citizen. The consequence of the relations is that the native citizen who is taxed may have domicile, and the property from which his income is derived may have situs, in a foreign country and the tax be legal — the government having power to impose the tax.

[Cook v. Tait, 265 U.S. 47, 56 (1924);

SOURCE: https://scholar.google.com/scholar_case?case=10657110310496192378]

Notice that civil status, property, and VOLUNTARY franchises (“trade or business”, benefits, or domicile) are the ONLY things he discussed here as the basis for whether the tax was lawful. Those are the KEY so we focus on these things on this site. But he (Taft, the SCOUNDREL who made the tax INTERNATIONAL in scope AFTER he fraudulently ratified the Sixteenth Amendment) HID how the election/consent takes place. That is discussed in:

- Invisible Consent, FTSIG

https://ftsig.org/how-you-volunteer/invisible-consent/ - Catalog of Elections and Entity Types in the Internal Revenue Code, FTSIG

https://ftsig.org/catalog-of-elections-in-the-internal-revenue-code/

2. The ORIGIN of PUBLIC/GOVERNMENT Property: “Domestic”/”trade or business within the United States”/”personal services”

Quasi in rem jurisdiction. Type of jurisdiction of a court based on a person’s interest in property within the jurisdiction of the court. Refers to proceedings that are brought against the defendant personally; yet it is the defendant’s interest in the property that serves as the basis of the jurisdiction. There must be a connection involving minimum contact between the property and the subject matter of the action for a state to exercise quasi in rem jurisdiction. Shaffer v. Heitner, 433 U.S. 186, 97 S.Ct. 2569, 53 L.Ed.2d 683. Quasi in rem proceedings is generally defined as affecting only interest of particular persons in specific property and is distinguished from proceedings in rem which determine interests in specific property as against the whole world. Avery v. Bender, 124 Vt. 309, 204 A.2d 314, 317. See also Jurisdiction.

[Black’s Law Dictionary, Sixth Edition, p. 1258]

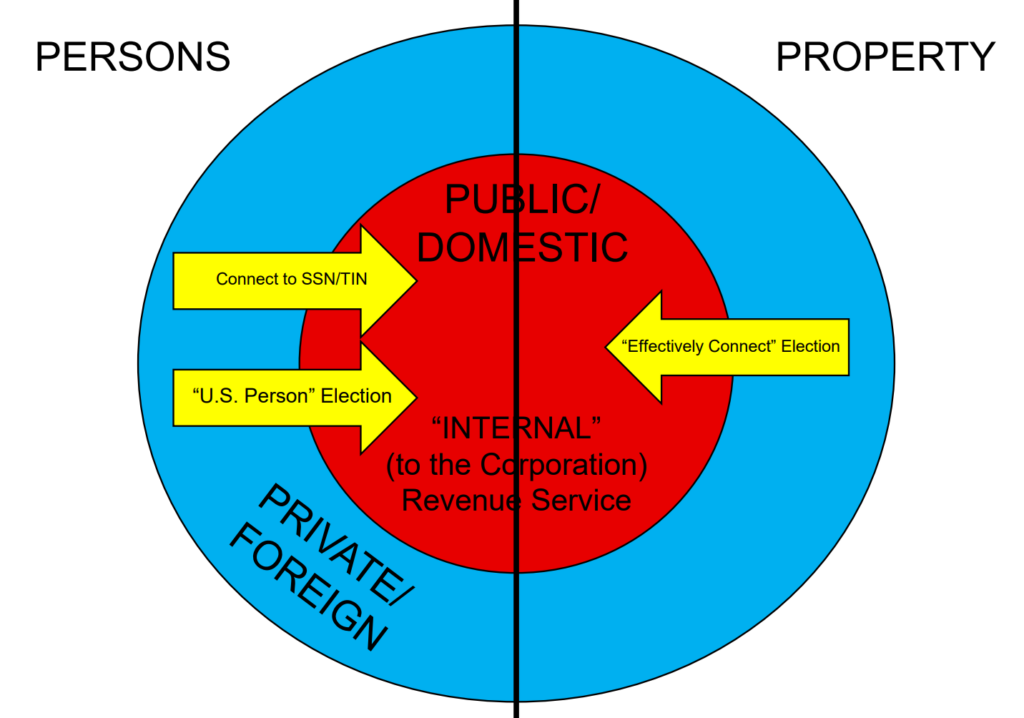

Your desire and covetousness for public property in the form of public status such as CIVIL “citizen” or CIVIL “person” is the lure that draws you into the statutory trap and the jurisdiction of the court. The “res” is the status itself and all tax proceedings in court are “in rem” to vindicate privileges attached to the status and the voluntary surety for the status. The collection of all such property is classified as “domestic”:

“Domestic” in the context of this website means PUBLIC property. It is defined as follows:

26 U.S. Code § 7701 – Definitions

(a)When used in this title, where not otherwise distinctly expressed or manifestly incompatible with the intent thereof—

(4)Domestic

The term “domestic” when applied to a corporation or partnership means created or organized in the United States or under the law of the United States or of any State unless, in the case of a partnership, the Secretary provides otherwise by regulations.

First, notice the definition says, “…when applied to a corporation or partnership means created or organized in the United States or under the law of the United States….” This “when applied” phrase indicates there are instances when the term can be applied differently. This can be very confusing without a proper understanding of the term “United States” as defined in 26 U.S.C. §7701(a)(9).

To that end, the proper application of the two meanings for the term “domestic” when deployed in the IRC is as follows:

- domesticGOV – The overarching jurisdictional attribute of United StatesGOV property interests (“USPI”) worldwide; or

- domesticG – The geographical attribute relating to United StatesG, which represents a local (50 States & D.C. collectively) subclass of worldwide domesticGOV USPI.

CAUTION: The term “United States” as used in the phrase “in the United States” is an area of tremendous equivocation in the IRC. It can be deployed in its principal / “political sense”—United StatesP (i.e., as in 26 C.F.R. §1.1-1(c)). Many wrongly presume the term “United States” always means the country or the nation, that is, the “political sense.” But it rarely has that meaning in the IRC. Additionally, most regard the geographical sense as representative of the country or nation, not realizing that a country/nation is a political association and not simply a geographical entity. This typically leads to uneducated conclusions that what is presented in the IRC applies to them and their activities. This typically results in unfavorable “elections” and so-called “voluntary compliance.”

However, the “United States” is most frequently encountered in the IRC in its so-called “geographical sense” (United StatesG), or its governmental sense (United StatesGOV). United StatesG describes a local jurisdictional subclass of worldwide United StatesGOV interests. Realize that when United StatesG is encountered, a United StatesGOV nexus is still implied in the larger context. When the United StatesGOV context is encountered, there is no geographical limitation. When United StatesG is encountered, a narrower geographical class is being applied to what otherwise is the broader United StatesGOV worldwide context. In other words, United StatesG is a domesticG subclass (50 States & D.C.) of United StatesGOV property interests (“USPI”) worldwide.

The United StatesGOV is an extensive collection of USPI comprising both tangible (land, buildings, hardware, etc.) and intangible property (contracts, securities, labor, offices, etc.) and the laws enacted to well and faithfully administer the fiduciary responsibilities over that USPI per the U.S. Constitution. The CIVIL law is simply an organization of that property for constitutional purposes. The constitution creates a trust:

- The corpus of the trust is USPI.

- The trust separates USPI (public interests) from private interests.

- The beneficiaries of the trust are “We the People and our posterity”.

- The grantor of the trust is the Founding Fathers collectively.

The term “trade or business” is an ACTIVITY involving the USE of “domestic” property. Article 4, Section 3, Clause 2 of the constitution is the authority to REGULATE and by implication TAX such a use.

26 U.S. Code § 7701 – Definitions

(a)When used in this title, where not otherwise distinctly expressed or manifestly incompatible with the intent thereof—

(4) Trade or business

(26)Trade or business

The term “trade or business” includes the performance of the functions of a public office.

The term “personal services” describes PEOPLE involved in the ACTIVITY of using or receiving the BENEFIT of public property. There is NO DIRECT definition anywhere of the term “personal services” in I.R.C. Subtitle A. The closest thing to a definition is found below:

26 U.S. Code § 864 – Definitions and special rules

(b)Trade or business within the United States

For purposes of this part, part II, and chapter 3, the term “trade or business within the United States” includes the performance of personal services within the United States at any time within the taxable year, but does not include—

The words “personal services” appearing in the above definition—either individually or collectively—are not defined anywhere in the IRC. The courts interpret those words in the broadest sense possible. However, their limited scope can accurately be ascertained in 26 U.S.C. §864(b) through proper understanding of the foregoing tangible and intangible property concepts, and how they relate to a proper understanding of the different meanings for the term “United States.”

The “performance of personal services” describes an ACTIVITY. An activity is an intangible thing—not a tangible thing. Tangible property (land, buildings, hardware) is regarded to be legally located in the jurisdiction of its actual situs or physical geographical location. Whereas intangible property is regarded to be legally located in the jurisdiction of its owner, even though the intangible property may be realized elsewhere.

For example, if tangible USPI is encountered in TexasG, it would more appropriately be regarded as located within the United StatesG because USPI constitutes a domesticGOV United StatesGOV property interest. In this example, the jurisdiction of TexasG would be federally preempted in favor of the domesticG United StatesG location. However, if the tangible property was not USPI, but private, not only would it be regarded as located in TexasG, but it would also be regarded as without the United StatesG and both non-domesticG and non-domesticGOV. In other words—foreign. Not “foreign” politically, but jurisdictionally.

Conversely, intangible property is legally located in the jurisdiction of the owner. In the case of excise taxable activity within the domesticGOV jurisdiction of the United StatesGOV, federal preemption again takes place, and the District of ColumbiaG (the seat of the United StatesGOV) is regarded as within the United StatesG and domesticG. The “performance of personal services” is the excise taxable activity contemplated under IRC Subtitles A and C. But BEFORE they can regulate you in the performance of said excise taxable activity, YOU HAVE TO VOLUNTEER. The act of volunteering is constructively an “election.”

With all of that said, how can we know what is meant by the phrase, “the performance of personal services within the United States”?

- BOTH “trade or business” and “personal services” always go together. You can’t have one without the other. They can’t reach the property without attaching it to a PERSON they created and own. We know this because tax cases are filed “in personam” instead of “in rem”. They proceed against the name of the HUMAN CUSTODIAN who originally held title as a personPRI who elected themself into a personPUB status through an effectively connected election.

- “trade or business” and “personal services” are both intangible fictions. Both of them are nongeographical because they are intangible.

- Thus, the only proper meaning for “trade or business within the United States” is within the corporation in connection with intangible “personal services”. That way, all terms mix because all are intangible. Otherwise, it would mix TANGIBLE and INTANGIBLE property

- “trade or business within the United States” in 26 U.S.C. §864(b) is a NEW TERM. They put the entire term in quote so its a NEW term: “trade or business within the United States”. The ONLY thing within the NEW term definition is “personal services”.

- They use the word “includes” in the definition of “trade or business within the United States” in 26 U.S.C. §864(b) because it encompasses “personal services” in connection with “nonresident aliens” who “effectively connect” in 26 U.S.C. §864(c). THEY are the ones who are therefore “included”.

- They are therefore talking about an ACTIVITY executed within the FICTIONAL “United States” corporation that is NONGEOGRAPHICAL.

In the case of 26 U.S.C. §864(b), “trade or business within the United StatesGOV” the phrase “within the United States” does NOT mean within United StatesG, but within the United StatesGOV corporation. How do we know this? Because:

- Judicially, “services” and “personal services” are treated as “INTANGIBLE” property, meaning that they are NONGEOGRAPHCAL and are often rendered by INTANGIBLE fictions such as businesses and corporations. See:

PROOF OF FACTS: Taxation of Intangibles is at the domicile of the owner by default, FTSIG

https://ftsig.org/proof-of-facts-taxation-of-intangibles-is-at-the-domicile-of-the-owner/ - INTANGIBLE property has no fixed geographical locality, but it can AFFECT people WITHIN a geography.

- You can’t mix GEOGRAPHICAL terms with FICTIONAL terms. It is NOT the same thing as “trade or business” in 26 U.S.C. §7701(a)(26) PLUS “within the United States” in 26 U.S.C. §7701(a)(9) and (a)(10).

- INTANGIBLE property such as FICTIONAL positions that include CIVIL “persons”, “taxpayers”, etc. are ALWAYS taxed at the domicile of the owner. The OWNER of these fictions is their CREATOR, the United States federal corporation domicile and seated in the District of Columbia under Article 1, Section 8, Clause 17 of the constitution and 4 U.S.C. §72.

Below is a description of this phenomenon, keeping in mind that the United States federal corporation is an intangible fiction:

“Since the corporate personality is a fiction, although a fiction intended to be acted upon as though it were a fact, Klein v. Board of Supervisors, 282 U.S. 19, 24, it is clear that unlike an individual its “presence” without, as well as within, the state of its origin can be manifested only by activities carried on in its behalf by those who are authorized to act [AGENTS and OFFICERS such as “taxpayers” and “persons”] for it. To say that the corporation is so far “present” there as to satisfy due process requirements, for purposes of taxation or the maintenance of suits against it in the courts of the state, is to beg the question to be decided. For the terms “present” or “presence” are used merely to symbolize those activities of the corporation’s agent [OFFICER] within the state which courts will deem to be sufficient to satisfy the demands of due process. L. Hand, J., in Hutchinson v. Chase & Gilbert, 45 F.2d 139, 141. Those demands may be met by such contacts [or FRANCHISES, which are ALSO contracts] of the corporation with the state of the forum as make it reasonable, in the context of our federal system of government, to require the corporation to defend the particular suit which is brought there. An “estimate of the inconveniences” which would result to the corporation from a trial away from its “home” or principal place of business [tax home, 26 C.F.R. §301.7701(b)-2(c)] is relevant in this connection. Hutchinson v. Chase & Gilbert, supra, 141.”

[International Shoe Co. v. Washington, 326 U.S. 310, 316-317 (1945); SOURCE: https://scholar.google.com/scholar_case?case=5514563780081607825]

Under the rule of taxing INTANGIBLES at the domicile of the owner, if in fact, you and the “taxpayer” fiction were synonymous, the taxation of YOU would have to occur at YOUR domicile rather than that of the FICTIONAL office you occupy. For the purposes of the federal income tax, that’s simply NOT the case. The EFFECTIVE domicile of the “taxpayer” fiction is the District of Columbia and not the human animating the fiction.

26 U.S. Code § 7701 – Definitions

(39) Persons residing outside United States

If any citizen or resident of the United States does not reside in (and is not found in) any United States judicial district, such citizen or resident shall be treated as residing in the District of Columbia for purposes of any provision of this title relating to—

(A) jurisdiction of courts, or

(B) enforcement of summons.

(d)Citizens and residents outside the United States

If any citizen or resident of the United States does not reside in, and does not have his principal place of business in, any United States judicial district, such citizen or resident shall be treated for purposes of this section as residing in the District of Columbia.

This mechanism of litigating ONLY at the CIVIL DOMICILE of the OWNER of the fiction is recognized under Federal Rule of Civil Procedure 17:

Rule 17. Plaintiff and Defendant; Capacity; Public Officers

(b) Capacity to Sue or Be Sued. Capacity to sue or be sued is determined as follows:

(1) for an individual who is not acting in a representative capacity, by the law of the individual’s domicile;

(2) for a corporation, by the law under which it was organized; and

(3) for all other parties, by the law of the state where the court is located, except that:

(A) a partnership or other unincorporated association with no such capacity under that state’s law may sue or be sued in its common name to enforce a substantive right existing under the United States Constitution or laws; and

(B) 28 U.S.C. §§754 and 959(a) govern the capacity of a receiver appointed by a United States court to sue or be sued in a United States court.

Paragraph (2) is the venue that all federal income tax disputes are litigated, which means the District of Columbia. They essentially are litigated “in rem”, which means a proceeding over PROPERTY. The STATUS is the subject of property and YOU are the object.

Since the term “personal services” can also be used in a PRIVATE context, the following evidence proves how that is done:

26 U.S. Code § 864 – Definitions and special rules

(1)Performance of personal services for foreign employer

The performance of personal services—

(A) for a nonresident alien individual, foreign partnership, or foreign corporation, not engaged in trade or business within the United States, or

(B) for an office or place of business maintained in a foreign country or in a possession of the United States by an individual who is a citizen or resident of the United States or by a domestic partnership or a domestic corporation,

by a nonresident alien individual temporarily present in the United States for a period or periods not exceeding a total of 90 days during the taxable year and whose compensation for such services does not exceed in the aggregate $3,000.

THIS is the ONLY example anywhere that we have found in which “personal services” isn’t linked to “trade or business within the United States”. Note that it has to be QUALIFIED with a connection to “foreign”, meaning PRIVATE and ForeignS or ForeignP. In other words, NON-DOMESTIC “personal services” by PRIVATE people. You can verify this further by looking at several authorities citing “personal services” below:

Authorities on “personal services”, Family Guardian Fellowship

https://famguardian.org/TaxFreedom/CitesByTopic/PersonalServices.htm

Other than 26 U.S.C. §864(b), “personal services” is never defined BY ITSELF, and the reason is because they don’t want to inform you of WHO you are serving as an agent, which is the United StatesGOV and not the people you do business with:

Microsoft Copilot: Meaning of civil statutory “services”, FTSIG

https://ftsig.org/microsoft-copilot-meaning-of-civil-statutory-services/

The reason we show you what “personal services” is NOT, is to deal with sophists who start arguments or try to discredit you by using undefined words and switching the context to discredit you or debate you. That’s their favorite tactic. Sophists equivocators are EASY to defeat if you ALWAYS:

- Begin the debate with definitions.

- Never stray from the definitions.

- Define what the term IS and all the contexts for the term that apply.

- Also define what it is NOT, meaning all the contexts that do not apply.

The above strategy is described below:

HOW TO: Successful Strategy for Litigation and Administrative Correspondence, FTSIG

https://ftsig.org/how-to-successful-strategy-for-litigation-and-administrative-correspondence/

SO, the DEFAULT context for “personal services” is ALWAYS “domestic”, which is synonymous with “trade or business within the United States”, but ONLY in the context of I.R.C. Subtitles A and C. We are not speaking here about ANY OTHER CONTEXT. Equivocators who want to discredit us should note that fact.

THE most important subject of all is EXACTLY how the straw man is created, which can only be by consent. THIS is that proof.

Proof That There is a “Straw Man”, Form #05.042

https://sedm.org/Forms/05-MemLaw/StrawMan.pdf

You can be sure that this is the BIGGEST third rail issue there is. Sophists in the District of Columbia will NEVER admit this is the case. Here’s why:

Microsoft Copilot: Meaning of civil statutory “services”, FTSIG

https://ftsig.org/microsoft-copilot-meaning-of-civil-statutory-services/

Some people would say it’s UNNECESSARY to make the points in this section, but that would censor the WHOLE truth and conceal the main weapon of some sophists in the government and legal profession. If you censor or discredit or disagree with the truths in this section, you lose the ability to prove that consent is invisible or is being hidden AND you help conceal the fact that the income tax is NOT mandatory but voluntary for most people.

The content of this section explains the reason behind publishing the following two articles on this site:

- Invisible Consent, FTSIG

https://ftsig.org/how-you-volunteer/invisible-consent/ - Process to “Invisibly” join the Matrix: Electing a CIVIL STATUTORY STATUS, FTSIG

https://ftsig.org/how-you-volunteer/process-to-invisibly-join-the-matrix-electing-a-civil-statutory-status/

3. How Congress Lawfully Acquires a PUBLIC/Ownership Interest in Your Private Property: YOUR Implied Consent to Privileges

The basis of the income tax is what the U.S. Supreme Court calls the Public Rights Doctrine. That court doctrine states that when the government creates a civil statutory rightPUB as PUBLIC property against itself, it has exclusive authority to define and regulate the right, create presumptions, and prescribe all remedies, INCLUDING no remedies, if it wants.

“These general rules are well settled:

(1) That the United States, when it creates rights in individuals against itself, is under no obligation to provide a remedy through the courts. United States ex rel. Dunlap v. Black, 128 U.S. 40; Ex parte Atocha, 17 Wall. 439; Gordon v. United States, 7 Wall. 188, 195; De Groot v. United States, 5 Wall. 419, 431-433; Comegys v. Vasse, 1 Pet. 193, 212.

(2) That, where a statute creates a right and provides a special remedy, that remedy is exclusive. Wilder Manufacturing Co. v. Corn Products Co., 236 U.S. 165, 174-175; Arnson v. Murphy, 109 U.S. 238; Barnet v. National Bank, 98 U.S. 555, 558; Farmers’ & Mechanics’ National Bank v. Dearing, 91 U.S. 29, 35.

Still, the fact that the right and the remedy are thus intertwined might not, if the provision stood alone, require us to hold that the remedy expressly given excludes a right of review by the Court of Claims, where the decision of the special tribunal involved no disputed question of fact and the denial of compensation was rested wholly upon the construction of the act. See Medbury v. United States, 173 U.S. 492, 198; Parish v. MacVeagh, 214 U.S. 124; McLean v. United States, 226 U.S. 374; United States v. Laughlin, 249 U.S. 440. “[United States v. Babcock, 250 U.S. 328, 331 (1919);

SOURCE: https://scholar.google.com/scholar_case?case=13911914425951042261]

That EXCLUSIVE power over public rightsPUB as PUBLIC PROPERTY OWNERSHIP, functions as a loan of public propertyPUB with CIVIL LEGAL conditions or strings attached. Hence, USPI is always involved. Note the phrase above “creates a right”, which is synonymous with the phrase “created or organized” in the definition of “Domestic” in 26 U.S.C. §7701(a)(4). This is NO ACCIDENT. Whatever Congress legislatively creates it absolutely owns as PUBLIC/GOVERNMENT property. “Domestic” within the Internal Revenue Code, in turn, is therefore synonymous with the government itself, because the government itself is just a collection of property and offices as a public trust. That property is the CORPUS of a public trust called the Constitution. Since the offices are legislatively created as property, the the government in turn is just a collection of public property as described below:

What is “Government”?, FTSIG

https://ftsig.org/special-language/what-is-government/

Since the power to tax always involves public propertyPUB, then the origin of the authority to tax is Article 4, Section 3, Clause 2 and not Article 1, Section 8, Clause 1. We examine this aspect in the following fascinating AI discovery for your edification:

Microsoft Copilot: Public Interest Doctrine v. Public Rights Doctrine, FTSIG

https://ftsig.org/microsoft-copilot-public-interest-doctrine-v-public-rights-doctrine/

The power to tax is therefore an extension of the power to regulate, because both require a government/PUBLIC property interest in the property so regulated or taxed. Congress can only regulate, and by implication tax, property that it has some degree of ownership interest in, whether absolute or qualified. This was confirmed by SCOTUS as follows in a related court doctrine called the Public Interest Doctrine, which is also mentioned in the above AI discovery:

“The compensation which the owners of property, not having any special rights or privileges from the government in connection with it, may demand for its use, or for their own services in union with it, forms no element of consideration in prescribing regulations for that purpose.

[. . .]

“It is only where some right or privilege [which are GOVERNMENT PROPERTY] is conferred by the government or municipality upon the owner, which he can use in connection with his property, or by means of which the use of his property is rendered more valuable to him, or he thereby enjoys an advantage over others, that the compensation to be received by him becomes a legitimate matter of regulation. Submission to the regulation of compensation in such cases is an implied condition of the grant, and the State, in exercising its power of prescribing the compensation, only determines the conditions upon which its concession shall be enjoyed. When the privilege ends, the power of regulation ceases.”

[Munn v. Illinois, 94 U.S. 113 (1877);

SOURCE: https://scholar.google.com/scholar_case?case=6419197193322400931]

The use of the word “privilege” above is synonymous with PUBLIC property. They are saying that if you receive public property in any form, there is an implied, equitable, quid pro quo, “quantum meruit”, or “quasi-contractual” obligation to RETURN the economic value of the PUBLIC consideration you received from the government in some form. That is the origin of the power to tax. Below is an example of this quid pro quo relationship always involved in the power to tax, in this case also involving the Minimum Contacts Doctrine of the U.S. Supreme Court, which we discuss in our Acquiring a Civil Status article:

Clearly, this is not a case where a state reaches beyond its borders and fastens its tax talons upon an event having no factual connection with transactions within its borders whereby it is unable to confer anything in return for the exaction. Here instead the taxpayer is present through its extensive localized activities and enjoys, in return for any taxes exacted, the opportunities, protection, and benefits of a modern community serviced by a state government which maintains courts, police, roads, and other services of distinct advantage to the building and maintenance of the taxpayer’s tremendous sales volume (48 percent of its total sales volume) through business outlets within the state. It is not amiss to observe that the taxpayer, or its immediate predecessor under a prior incorporation, has already had occasion to seek the benefit and protection of our courts.

[State v. Northwestern States Portland Cement Co., 250 Minn. 32 (1957);

SOURCE: https://scholar.google.com/scholar_case?case=9259450114651710414]

So long as you REFUSE all public property, public rights, “benefits”, and privileges, there can be no civil or tax obligation on your part or ability to enforce against you on the government’s part.

“A person is ordinarily not required to pay for benefits which were thrust upon him with no opportunity to refuse them. The fact that he is enriched is not enough, if he cannot avoid the enrichment.” Wade, Restitution for Benefits Conferred Without Request, 19 Vand. L. Rev. at 1198 (1966).

[Siskron v. Temel-Peck Enterprises, 26 N.C.App. 387, 390 (N.C. Ct. App. 1975)]

“As was said in Wisconsin v. J. C. Penney Co., 311 U.S. 435, 444 (1940), “[t]he simple but controlling question is whether the state has given anything for which it can ask return.”

[Colonial Pipeline Co v Traigle, 421 U.S. 100, 109 (1975)]

It is a maxim of law that you have a right to REFUSE all such “benefits” and property:

“Cujus est commodum ejus debet esse incommodum. He who receives the benefit should also bear the disadvantage.”

Hominum caus jus constitutum est. Law is established for the benefit of man.

Injuria propria non cadet in beneficium facientis. One’s own wrong shall not benefit the person doing it.

Invito beneficium non datur. No one is obliged to accept a benefit against his consent. Dig. 50, 17, 69. But if he does not dissent he will be considered as assenting. Vide Assent.

Potest quis renunciare pro se, et suis, juri quod pro se introductum est. A man may relinquish, for himself and his heirs, a right which was introduced for his own benefit. See 1 Bouv. Inst. n. 83.

Privatum incommodum publico bono peusatur. Private inconvenience is made up for by public benefit.

Privilegium est beneficium personale et extinguitur cum person. A privilege is a personal benefit and dies with the person. 3 Buls. 8.

Que sentit commodum, sentire debet et onus. He who derives a benefit from a thing, ought to feel the disadvantages attending it. 2 Bouv. Inst. n. 1433.

Quilibet potest renunciare juri pro se inducto. Any one may renounce a law introduced for his own benefit. To this rule there are some exceptions. See 1 Bouv. Inst. n. 83.

[Bouvier’s Maxims of Law, 1856; https://famguardian.org/Publications/BouvierMaximsOfLaw/BouviersMaxims.htm]

It is usurpation to:

- Treat you AS IF you accepted a benefit without actually having to satisfy the burden of proving the exact economic value of the “benefit” and your EXPRESS informed consent to receive it.

- FORCE you to accept a “benefit” or public property.

- Interfere with your right to REJECT the benefit.

- Refuse to offer forms or procedures or HIDE forms or procedures to REJECT the “benefit”.

- Refuse to identify exactly how you VOLUNTEERED to become eligible for the benefit.

All the above defeat the purpose indicated in the Declaration of Independence, which states that all JUST powers of government derive from CONSENT of the governed. The implication is that you have the right to WITHDRAW consent and any attempt to interfere with that withdrawal makes the government INHERENTLY UNJUST.

In the context of income taxation, an act of consenting to receive PUBLIC property or a “benefit” is called an “election”. There are TWO primary methods dealing with your private property that constitute such an “election”:

- Change your OWN CIVIL STATUS from PRIVATE to PUBLIC. This is typically done by electing a “U.S. person” status under 26 U.S.C. §7701(a)(30). This makes ALL earnings taxable worldwide for those who make such an election.

- Change the STATUS of your PRIVATE PROPERTY from PRIVATE to PUBLIC. This is typically done by:

2.1. “effectively connecting” your otherwise PRIVATE earnings on a a 1040NR return in order to take deductions against the property.

2.2. Connecting an SSN or TIN to the property, which implicates a connection to a “trade or business” under 26 C.F.R. §301.6109-1(b) in the case of nonresident aliens who are private.

The following case recognizes the above list:

“In the case of the federal government where the individual is either a United States citizen or an alien residing in the taxing jurisdiction, the tax under section 1 of the Code is based upon jurisdiction over the person; where the individual is an alien not residing in the taxing jurisdiction, the tax under section 871 of the Code is based upon jurisdiction over the property or income of the nonresident individual located or earned in the taxing jurisdiction”

[Great Cruz Bay, Inc., St. John v. Wheatley, 495 F.2d. 301, 307 (3d Cir. 1974);

SOURCE: https://scholar.google.com/scholar_case?case=18118242110028613875]

What BOTH methods above have in common is that they connect either YOU or your PROPERTY to the “trade or business” excise taxable franchise. That franchise is defined as follows:

26 U.S. Code § 7701 – Definitions

(a)When used in this title, where not otherwise distinctly expressed or manifestly incompatible with the intent thereof—

(26)Trade or business

The term “trade or business” includes the performance of the functions of a public office.

In most cases there is no real or actual net economic “benefit” to connecting YOU or your PROPERTY to the “trade or business” franchise because:

- The Internal Revenue Code itself doesn’t deliver any substantial “benefits” at all. Those benefits are delivered by OTHER titles of the U.S. Code. According to the rules of statutory construction, you ALSO can’t look outside Title 26 to FIND that benefit. The title must be self-contained, because it is a stand-alone franchise all its own.

- If you claim nonresident alien status, most of your earnings are excluded and don’t need to be entered on the tax return. 26 U.S.C. §162 permits PRIVILEGED “trade or business” deductions to be used to reduce your tax liability on the tax return, but if all your earnings are lawfully excluded as a nonresident alien, which is the default status for all American nationals, there is no need for such deductions to begin with.

It is beyond the scope of this website to go into all the details surrounding the “trade or business” franchise. Suffice it to say that it is an invention designed to permit you to donate your PROPERTY property to a PUBLIC use, a PUBLIC purpose, and a corresponding PUBLIC office to procure a specific privilege or benefit. You pursue the privilege by associating either YOURSELF or YOUR PROPERTY with a civil statutory status created and owned by the national government. Corresponding tax obligations inevitably “come along for the ride” by also being attached to the privileged civil statutory status. That is why we often say that OBLIGATIONS and PRIVILEGES (RIGHTS) are two sides of the same coin. You can’t have ONE without the OTHER.

The easy way to AVOID the benefit or privilege is just don’t seek or accept the status that CONVEYS the privileges and property and terminate all eligibility to do so. This is usually done by filing a tax return that connects you to a FOREIGN status and not entering anything into the “Effectively Connected” block on the return. For details on the “trade or business” franchise and franchises generally, see:

- The “Trade or Business” Scam, Form #05.001

https://sedm.org/Forms/05-MemLaw/TradeOrBusScam.pdf - Government Franchises Course, Form #12.012

https://sedm.org/LibertyU/GovFranchises.pdf - Government Instituted Slavery Using Franchises, Form #05.030

https://sedm.org/Forms/05-MemLaw/Franchises.pdf

Lastly, there are OTHER means of making an election as well. For a catalogue of all such elections, see:

Catalog of Elections in the Internal Revenue Code

https://ftsig.org/catalog-of-elections-in-the-internal-revenue-code/

4. An Offer of Privileges/USPI is a Merchant/Buyer Relationship

In commercial terms under the Uniform Commercial Code (U.C.C.), a government offer of privileges as USPI is described as a Merchant/Buyer relationship:

- Government is the Merchant under U.C.C. §2-104(1) offering PUBLIC property.

- You are the Buyer under U.C.C. §2-103(1)(a) accepting the offer and obligations associated with the offer.

- The terms of the Merchant/Buyer proposed relationship are codified in I.R.C. Subtitles A and C as CIVIL statutory law and a commercial franchise agreement. See:

Government Franchises Course, Form #12.012

Slides: https://sedm.org/LibertyU/GovFranchises.pdf

Video: http://youtu.be/vnDcauqlbTQ - Everyone covered by the franchise agreement is referred to as “domestic”, which 26 U.S.C. §7701(a)(4) refers to as “created or organized” by the United StatesGOV federal corporation and therefore WITHIN that corporation.

- Like every valid contract, the franchise contract or agreement has:

5.1. An offer of property/consideration.

5.2. An acceptance, which can be IMPLIED (through actions) or EXPRESS (through explicit written or verbal consent).

5.3. Mutual consideration (property).

5.4. Mutual obligation. - You as Buyer manifest acceptance of commercial offer by the Merchant by:

6.1. Invoking a civil status created, codified, and owned by the national government in the franchise agreement. In FTC terms, the civil status of “U.S. person” or “person” are the “franchise mark”.

6.2. Availing yourself of privileges offered through the franchise agreement, such as deductions, benefits, etc.

6.3. Using forms or processes “created or organized” by Uncle Sam to “service” franchise participants. The IRS calls themself the “INTERNAL (to the government) Revenue Service”. See:

Avoiding Traps in Government Forms Course, Form #12.023

https://sedm.org/LibertyU/AvoidingTrapsGovForms.pdf - Once accepted by any of the above methods of usually IMPLIED consent, no liability statute is necessary. Merely accepting the privileges or USPI or benefits of the franchise agreement creates a “quasi-contractual” obligation on your part to obey the franchise agreement.

- Beyond the point of constructive IMPLIED consent, the property conferred by the Merchant to the Buyer constitutes what is called a “grant” conveys the power to regulate all participants. Said regulation, in fact, is PART of the “consideration” of the franchise.

- Regulation of the participants beyond the point of consent is done through the “administrative state”:

Administrative State: Tactics and Defenses Course, Form #12.041

https://sedm.org/LibertyU/AdminState.pdf

The above relationships are confirmed by the U.S. Supreme Court, when it refers to the above process as a “concession”, which is defined as a SALES process:

“Submission to the regulation of compensation in such cases is an implied condition 147*147 of the grant, and the State, in exercising its power of prescribing the compensation, only determines the conditions upon which its concession shall be enjoyed. When the privilege ends, the power of regulation ceases.”

[Munn v. Illinois, 94 U.S. 113, 146-147 (1877);

SOURCE: https://scholar.google.com/scholar_case?case=6419197193322400931]

NOTICE, however, that in the case of the government’s I.R.C. Subtitles A and C franchise agreement:

- DEDUCTIONS are the ONLY real “consideration” under 26 U.S.C. §162, 26 U.S.C. §864(b) (“U.S. persons” and “nonresident aliens” who effectively connect), and 26 U.S.C. §873 (nonresident aliens only).

- “GROSS INCOME” under 26 U.S.C. §61 is NOT the consideration or the origin of the obligation or right to regulate or tax. It would have to be PAID by and from the government to in fact BE “consideration”, USPI, or PUBLIC property that could lawfully be origin of the authority to regulate or tax.

- You only need PRIVILEGED “deductions” under 26 U.S.C. §162 if and only if you in fact HAVE “gross income” under:

3.1. 26 U.S.C. §61 in the case of “U.S. persons” under under 26 U.S.C. §7701(a)(30).

3.2. 26 U.S.C. §872 in the case of “nonresident aliens” under under 26 U.S.C. §7701(b)(1)(B). - You must FIRST volunteer INTO the franchise as a “U.S. person” under 26 U.S.C. §7701(a)(30) or “nonresident alien” who “effectively connects” or “person” under 26 U.S.C. §6671(b) and 26 U.S.C. §7343 to even EARN “gross income”. Making YOU the OWNER of the payment “domestic” must precede your PROPERTY or the payment itself becoming “domestic”. By “domestic” we mean owned or controlled by the government as 26 U.S.C. §7701(a)(4) demonstrates.

- Once the privilege is elected:

5.1. You become a “nonresident alien individualPUB” under 26 U.S.C. §864(b) engaged in “personal services” within the United StatesGOV as a franchisee.

5.2. Every type of “gross income” you write on the 1040NR is subject to said privileged deductions under the deeming provisions in 26 U.S.C. §864(c)(3), which in effect CREATES “gross income” subject to tax BY VIRTUE of the election of the deduction privilege. - Privileged deductions are NOT necessary for those who are not aliens because they are American nationals and may avoid the tax by avoiding the deduction privilege 26 U.S.C. §873(b)(3).

- Information returns filed against you create a usually FALSE presumption that you have “gross income”. These are usually filed by mistake. See:

Correcting Erroneous Information Returns, Form #04.001

https://sedm.org/Forms/04-Tax/0-CorrErrInfoRtns/CorrErrInfoRtns.pdf - Information returns are usually mistaken usually because:

8.1. They report as fact an amount of payment and the parties to the payment.

8.2. They do not establish the LEGAL STATUS of the payment, including whether it is a “U.S. source”.

8.3. The legal status of the payment is a LEGAL determination, not a FACT.

8.4. Only you as the absolute owner of the payment can establish the LEGAL STATUS of the payment. Government must have an ownership interest in the payment to determine its legal status and they usually don’t have that. - As long as YOU the recipient of the payment and the target of the false information return understand the above and resist the usually false presumption that the payment is “gross income”, you will not be tempted to elect yourself into the franchise by declaring EITHER “U.S. person” or “nonresident alien” engaged in “trade or business” civil status.

- American nationals by default are “nonresident alien” non-persons.

10.1. They don’t earn “gross income” because it is “excluded” under 26 U.S.C. §872.

10.2. They only BECOME “persons” through pursuing deductions, which usually originates in the FALSE presumption that they earn “gross income”.

10.3. Pursuing deductions under 26 U.S.C. §873(b)(3) in order to REDUCE “gross income” you don’t actually have is the origin of how most American nationals become “taxpayers”.

You could thus say that in the case of American nationals, the current income tax is a tax on deductions you don’t need intended to reduce “gross income” you aren’t actually earning. The following tax return filing proves this:

1040NR Attachment, Form# 09.077

https://sedm.org/Forms/09-Procs/1040NR-Attachment.pdf

In biblical terms, God describes the above deception as follows:

“For thus says the Lord: “You have sold yourselves for nothing, And you shall be redeemed without money.”

[Isaiah 52:3, Bible, NKJV;

SOURCE: https://www.biblegateway.com/passage/?search=Isaiah%2052%3A3&version=NKJV]

By “nothing”, God means “no consideration”. “gross income” would have to be paid by the national government for there to be “consideration”. The U.S. Supreme Court has also held that in the absence of “consideration”, which it calls “benefits”, taxation is extortion:

The power of taxation, indispensable to the existence of every civilized government, is exercised upon the assumption of an equivalent rendered to the taxpayer in the protection of his person and property, in adding to the value of such property, or in the creation and maintenance of public conveniences in which he shares, such, for instance, as roads, bridges, sidewalks, pavements, and schools for the education of his children. If the taxing power be in no position to render these services, or otherwise to benefit the person or property taxed, and such property be wholly within the taxing power of another State, to which it may be said to owe an allegiance and to which it looks for protection, the taxation of such property within the domicil of the owner partakes rather of the nature of an extortion than a tax, and has been repeatedly held by this court to be beyond the power of the legislature and a taking of property without due process of law. Railroad Company v. Jackson, 7 Wall. 262; State Tax on Foreign-held Bonds, 15 Wall. 300; Tappan v. Merchants’ National Bank, 19 Wall. 490, 499; Delaware &c. R.R. Co. v. Pennsylvania, 198 U.S. 341, 358. In Chicago &c. R.R. Co. v. Chicago, 166 U.S. 226, it was held, after full consideration, that the taking of private property 203*203 without compensation was a denial of due process within the Fourteenth Amendment. See also Davidson v. New Orleans, 96 U.S. 97, 102; Missouri Pacific Railway v. Nebraska, 164 U.S. 403, 417; Mount Hope Cemetery v. Boston, 158 Massachusetts, 509, 519.

[Union Refrigerator Transit Company v. Kentucky, 199 U.S. 194, 202-203 (1905);

SOURCE: https://scholar.google.com/scholar_case?case=14163786757633929654]

The notion that the government doesn’t have to provide consideration or property that you both ASK for and RECEIVED in order to avoid the label of “extortion” above is firmly established as follows:

“A person is ordinarily not required to pay for benefits which were thrust upon him with no opportunity to refuse them. The fact that he is enriched is not enough, if he cannot avoid the enrichment.” Wade, Restitution for Benefits Conferred Without Request, 19 Vand. L. Rev. at 1198 (1966).

[Siskron v. Temel-Peck Enterprises, 26 N.C.App. 387, 390 (N.C. Ct. App. 1975)]

It is YOUR RIGHT to refuse all privileges and benefits and the obligations that originate from them. Taxation of “benefits” or “privileges” that you DO NOT want and do not need or have no opportunity to refuse is extortion. Refusing the privilege or benefit and thus the “consideration” avoids the following curse direct from God for those who ignorantly ACCEPT said benefit:

“The rich rules over the poor,

And the borrower is servant to the lender.”

[Prov. 22:7, Bible, NKJV]“The State in such cases exercises no greater right than an individual may exercise over the use of his own property when leased or loaned to others. The conditions upon which the privilege shall be enjoyed being stated or implied in the legislation authorizing its grant, no right is, of course, impaired by their enforcement. The recipient of the privilege, in effect, stipulates to comply with the conditions. It matters not how limited the privilege conferred, its acceptance implies an assent to the regulation of its use and the compensation for it.”

[Munn v. Illinois, 94 U.S. 113 (1876) ]_______________________________________________________________________________________

Curses of Disobedience [to God’s Laws]

“The alien [Washington, D.C. is legislatively “foreign” in relation to states of the Union] who is among you shall rise higher and higher above you, and you shall come down lower and lower [malicious destruction of EQUAL PROTECTION and EQUAL TREATMENT by abusing FRANCHISES]. He shall lend to you [Federal Reserve counterfeiting franchise], but you shall not lend to him; he shall be the head, and you shall be the tail.

“Moreover all these curses shall come upon you and pursue and overtake you, until you are destroyed, because you did not obey the voice of the Lord your God, to keep His commandments and His statutes which He commanded you. And they shall be upon you for a sign and a wonder, and on your descendants forever.

“Because you did not serve [ONLY] the Lord your God with joy and gladness of heart, for the abundance of everything, therefore you shall serve your [covetous thieving lawyer] enemies, whom the Lord will send against you, in hunger, in thirst, in nakedness, and in need of everything; and He will put a yoke of iron [franchise codes] on your neck until He has destroyed you. The Lord will bring a nation against you from afar [the District of CRIMINALS], from the end of the earth, as swift as the eagle flies [the American Eagle], a nation whose language [LEGALESE] you will not understand, a nation of fierce [coercive and fascist] countenance, which does not respect the elderly [assassinates them by denying them healthcare through bureaucratic delays on an Obamacare waiting list] nor show favor to the young [destroying their ability to learn in the public FOOL system]. And they shall eat the increase of your livestock and the produce of your land [with “trade or business” franchise taxes], until you [and all your property] are destroyed [or STOLEN/CONFISCATED]; they shall not leave you grain or new wine or oil, or the increase of your cattle or the offspring of your flocks, until they have destroyed you.

[Deut. 28:43-51, Bible, NKJV]

More on the content of this section at:

How Scoundrels Corrupted Our Republican Form of Government, Family Guardian Fellowship

https://famguardian.org/Subjects/Taxes/Evidence/HowScCorruptOurRepubGovt.htm

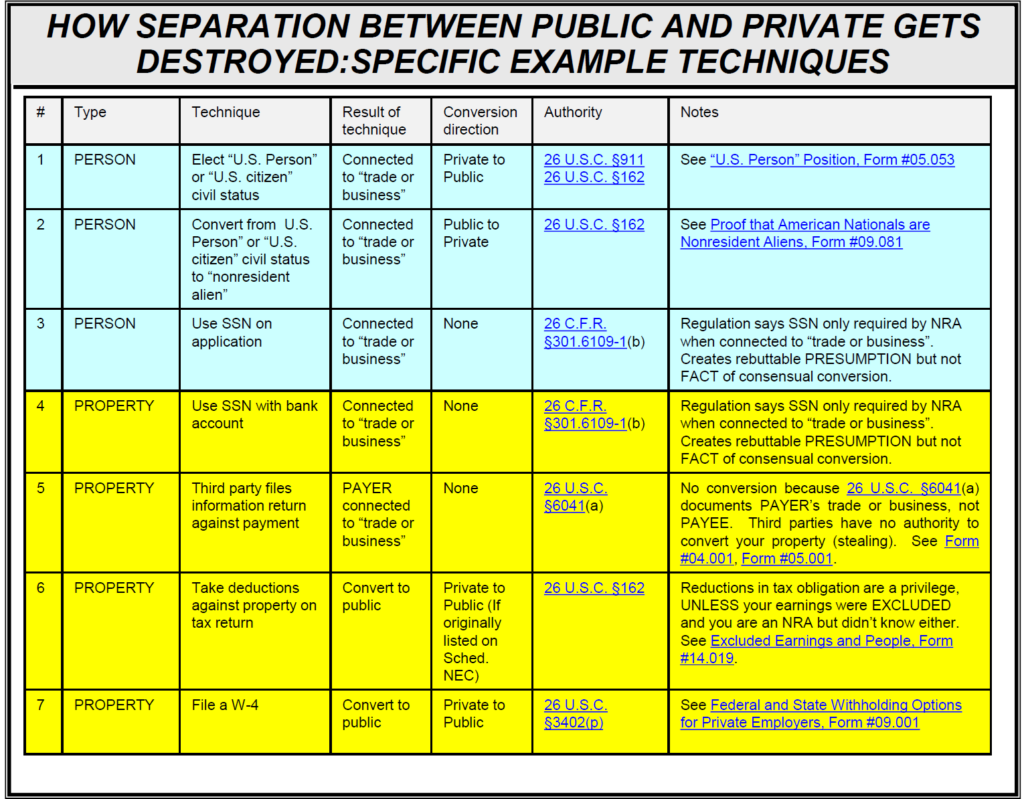

5. Status Elections, Deeming Provisions, and Equivocation: Tools of choice in converting PRIVATE to PUBLIC without your knowledge

When it comes to fooling you into unknowingly donating your property to the government and thus converting it from PRIVATE propertyPRI to PUBLIC propertyPUB, three primary tools are abused that you need to be VERY familiar with to avoid being victimized by the deception and sophistry:

- Status Elections: Accomplished by you electing to convert your PRIVATE/FOREIGN/POLITICAL status into a PUBLIC/DOMESTIC/CIVIL status by filing a 1040 instead of 1040-NR. See:

Catalog of Elections and Entity Types in the Internal Revenue Code, FTSIG

https://ftsig.org/catalog-of-elections-in-the-internal-revenue-code/ - Deeming provisions: Convert PRIVATE status to PUBLIC civil statutory status. A deeming provision uses the phrase “treated as”. An example is 26 U.S.C. §864(c)(3) relating to “effectively connecting” and 26 U.S.C. §3402(p) relating to your election to the status as a PUBLIC “employee”. Deeming provisions always use the phrase “treated as” instead of “IS”. They are telling they will TREAT private property as PUBLIC property because you consent to it.

- Equivocation: About the nature of the thing subject to taxation as either PRIVATE or PUBLIC. Equivocation is a type of logical fallacy designed to make you believe that two things are the same. Those two things in this case are PUBLIC and PRIVATE.

The Constitution as a trust indenture confers upon Congress the ability to regulate and tax mainly its own tangible PUBLIC propertyPUB as part of the trust corpus. That property includes:

- EXTERNAL TAXATION: “SOVEREIGNPUB POWERPUB” over foreign affairs under Article 1, Section 8, Clause 3 for taxation of aliens and foreign corporations who are not standing on land protected by the Constitution.

- INTERNAL TAXATION: PROPRIETARYPRI POWERPRI over PUBLIC/GOVERNMENT propertyPUB for the purposes of its interactions with political citizens* a political nationals of the United States* (country) standing on land protected by the Constitution. Sometimes deceptively referred to as SOVEREIGNPRI POWERPRI.

You can learn the difference between the above two categories in the following article:

HOW TO: How to distinguish “sovereign power” from “proprietary power” in the context of taxation, FTSIG

https://ftsig.org/how-to-how-to-distinguish-sovereign-power-from-proprietary-power-in-the-context-of-taxation/

For the purposes of INTERNAL taxation above effected through “PROPRIETARY POWERS”, the main type of property that it has chosen to tax using the income tax are civil statuses that it creates and owns and then “rents out” to you as a privilege for a franchise fee called a “tax”. We call this mechanism a “rent-an-identity” service. In order to convert your private property to public property in this scenario it must:

- Your default status is “U.S. person” in 26 U.S.C. §7701(a)(30)(A), not “nonresident alien”.

- The income tax is a tax on PRIVATE property.

- All “gross income” is PRIVATE property subject to tax. Thus, “gross income” in 26 U.S.C. §61 and 26 U.S.C. §872 are PRIVATE property, which in fact is NOT true in the case of American nationals protected by the constitution.

- No consensual conversion from PRIVATE to PUBLIC is necessary in order to tax.

- Income tax is not based on “consent” to convert property because the government in effect OWNS, or at least CONTROLS all property, including everything mentioned in the Bill of Rights. In other words: Socialism, meaning state ownership or control of all property and no PRIVATE property.

- The Fifth Amendment protection of PRIVATE property is irrelevant to the taxation of said PRIVATE property.

- INTERNAL taxation is a SOVEREIGN POWER rather than a PROPRIETARY POWER for American nationals.

- Government doesn’t have to equitably deliver any consideration or “benefit” to have the power to tax any amount they want. The result of this is that you and your property are mere CHATTEL and the Bill of Rights are IRRELEVANT when it comes to taxation.

In fact, NONE of the above are true in the case of American nationals standing on land protected by the Constitution. Every one of the above types of deception are implemented with either EQUIVOCATION, DEEMING PROVISIONS, or STATUS ELECTIONS. Below is a table itemizing all the above and the preferred method of deception:

| # | Description | Method of deception | The Truth |

| 1 | Your default status is “U.S. person” in 26 U.S.C. §7701(a)(30)(A), not “nonresident alien”. | Status Election | The citizen**+D subject to tax in 26 C.F.R. §1.1-1(a) and (b) starts out as a “nonresident alien” and has to volunteer for the status. If they DON’T, they remain a “national of the United States”. |

| 2 | The income tax is a tax on PRIVATE property. | Deeming provisions | Article 1, Section 8, Clause 1 documents a tax on PRIVATE property. The current income tax for INTERNAL purposes against American nationals is one on PUBLIC property. All excise taxes are taxes on PUBLIC property that became PUBLIC by you volunteering for a consensual activity and thereby becoming enfranchised using a “deeming provision” such as 26 U.S.C. §3402(p) or 26 U.S.C. §864(c)(3). |

| 3 | All “gross income” is PRIVATE property subject to tax. | Deeming provisions | For NRA50, deeming provisions in 26 U.S.C. §864(c)(3) CONVERT PRIVATE earnings to PUBLIC “gross income” |

| 4 | No consensual conversion from PRIVATE to PUBLIC is necessary in order to tax. | Equivocation | “Gross income” in 26 U.S.C. §61 and 26 U.S.C. §872 is PUBLIC property connected to a PRIVILEGE. That privilege is EITHER alienage in 26 U.S.C. §871(a) or “deductions” in 26 U.S.C. §871(b) in the case of aliens or nationals. |

| 5 | Income tax is not based on “consent” to convert property because the government in effect OWNS, or at least CONTROLS all property | Equivocation | Why the HELL do we need a Bill of Rights if there is NO private property? The entire PURPOSE of the Constitution is to protect ONLY PRIVATE property from INTERNAL regulation or taxation without consent. Anything not consensual is UNJUST from a CIVIL perspective. |

| 6 | The Fifth Amendment protection of PRIVATE property is irrelevant to the taxation of said PRIVATE property. | Equivocation | See: Microsoft Copilot: Does the Fifth Amendment still protect people not voluntarily engaged in excise taxable activities and who make no elections?, FTSIG https://ftsig.org/microsoft-copilot-does-the-fifth-amendment-still-protect-people-not-voluntarily-engaged-in-excise-taxable-activities-and-who-make-no-elections/ |

| 7 | INTERNAL taxation is a SOVEREIGN POWER rather than a PROPRIETARY POWER for American nationals. | Equivocation | Internal taxation of American nationals is a PROPERIETARY power mislabeled as a SovereignPRI PowerPRI derived from public property and Merchant/Buyer relationship. They just take the suffixes off so you don’t know WHICH “sovereign power” they are referring to: FOREIGN affairs or PUBLIC property. |

| 8 | Government doesn’t have to equitably deliver any consideration or “benefit” to have the power to tax any amount they want. | Equivocation | They don’t for “taxpayers” AFTER they volunteer, but not everyone is a “taxpayer”. See: Taxpayer v. Nontaxpayer, FTSIG https://ftsig.org/introduction/taxpayer-v-nontaxpayer/ |

More on the above types of sophistry, deception, and equivocation at:

HOW TO: Catalog of Deception Techniques, Third Rail Avoidance Tactics, and Defenses, FTSIG

https://ftsig.org/how-to-catalog-of-deception-techniques-third-rail-avoidance-tactics-and-defenses/

6. Process to determine Specific Types of taxable “gross income” in 26 U.S.C. §861

It’s helpful at this point to define a PROCESS to decide when and how your property as a “nonresident alien” became taxable as “gross income”.

We know that in the case of “nonresident aliens”:

- Not Effective Connected (NEC) under 26 U.S.C. §871(a): All “gross income” from WITHOUT the United StatesG that is not effectively connected with the “trade or business” excise taxable franchise is excluded under 26 U.S.C. §872 .

- Effectively Connected under 26 U.S.C. §871(b): Income “effectively connected” is taxed worldwide just like a “U.S. person” if it originates from activities in the U.S. under 26 U.S.C. §864(c)(4). This is because you can’t “effectively connect” without a “Person” election as well under 26 U.S.C. §864(b).

The process for calculating the above is documented in the following article:

Tax Computation Process for Nonresident Aliens, FTSIG

https://ftsig.org/tax-computation-process-for-nonresident-alien/

There is no “PERSONAL jurisdiction” over “nonresident aliens” by default without an election/consent, meaning no direct CIVIL statutory jurisdiction over them. This was the conclusion of the U.S. Supreme Court in Pennoyer v. Neff, 95 U.S. 714 (1878). Because there is no PERSONAL jurisdiction over non-consenting “nonresident aliens” and the only lawful jurisdiction exercised is PROPERTY jurisdiction, it must then be CONCLUSIVELY presumed that:

- Every type of “gross income” listed in 26 U.S.C. §861 derives from USPI as EITHER:

1.1. Elections: “effectively connected” by election as described in 26 U.S.C. §864(c). Congress by default doesn’t have civil jurisdiction over your property in a state so you have to make an election to CREATE that jurisdiction by your consent.

1.2. Privileged Alien Commerce within the COUNTRY United States*: Connected with the privileges of alienage by virtue of the foreign affairs functions of Congress under Article, 1, Section 8, Clause 3. This too is a type of election, because the choice by an alien residing abroad to do business in our country automatically comes with international obligations enforced by the Law of Nations. These international obligations CANNOT and DO NOT apply within the country to nationals of that country. - If you are an American national standing on land protected by the constitution and not an alien, at some point you had to VOLUNTARILY “effectively connect” the earnings/PROPERTY specified 26 U.S.C. §861 through the process documented in 26 U.S.C. §864(c), since otherwise, the PRIVATE property affected is protected by STATE law and not FEDERAL law. That process of volunteering is called an “election” by the IRS and it is exhaustively described in:

The Truth About “Effectively Connecting”, Form #05.056

https://sedm.org/Forms/05-MemLaw/EffectivelyConnected.pdf - By “effectively connecting” the property, federal preemption kicks in to remove the applicability of state law and thereby make federal jurisdiction “plenary” or “exclusive” over the property.

- No surrender or waiver of constitutional rights or conversion from PRIVATE to PUBLIC was involved if you are an American national standing on land protected by the constitution, because Congress cannot by legislation compel a waiver of constitutional rights as a condition of receiving any government service, benefit, or privilege. This restriction is called the Unconstitutional Conditions Doctrine by the U.S. Supreme Court. We discuss this restriction in:

USPI thru Changing the Status of Your PROPERTY to Domestic

Section 3: Consequences of making ALL government payments PUBLIC property AFTER they are received without your consent or permission, FTSIG

https://ftsig.org/how-you-volunteer/uspi-thru-domestic-source/#3._Consequences

That last item above, item 4, doesn’t fully apply to any of the following geographies not protected by the Constitution:

- Unincorporated territories.

- Some federal enclaves within the states.

- Abroad in a POLITICALLY foreign country.

It is true, however, that the U.S. Supreme Court recognizes some constitutional rights in items 1 and 2 above under what is called “The Fundamental Rights Doctrine”. To wit:

The Constitution of the United States is in force in Porto Rico as it is wherever and whenever the sovereign power of that government is exerted. This has not only been admitted but emphasized by this court in all its authoritative expressions upon the issues arising in the Insular Cases, especially in the Downes v. Bidwell and the Dorr Cases. The Constitution, however, contains grants of power and limitations which in the nature of things are not always and everywhere applicable, and the real issue in the Insular Cases was not whether the Constitution extended to the Philippines or Porto Rico when we went there, but which of its provisions were applicable by way of limitation upon the exercise of executive and legislative power in dealing with new conditions and requirements. The guaranties of certain fundamental personal rights declared in the Constitution, as for instance 313*313 that no person could be deprived of life, liberty or property without due process of law, had from the beginning full application in the Philippines and Porto Rico, and, as this guaranty is one of the most fruitful in causing litigation in our own country, provision was naturally made for similar controversy in Porto Rico.

[Balzac v. Puerto Rico, 258 U.S. 298, 312-313 (1922);

SOURCE: https://scholar.google.com/scholar_case?case=8956361016270671048]

The above process for analyzing whether an earning is “gross income” is helpful in how to determine what specific act triggered the “effectively connected” status. You can use it in analyzing each item listed in 26 U.S.C. §861 to decide for yourself where, when, and HOW it became taxable “gross income”.

Taxation, after all, is just the institutionalized process of converting PRIVATE to PUBLIC property and rights through voluntary consent of the original owner. The legal constraints applicable to that process are documented in:

Separation Between Public and Private Course, Form #12.025

https://sedm.org/LibertyU/SeparatingPublicPrivate.pdf

Government cannot tax or regulate PRIVATE property. It has to be converted from PRIVATE to PUBLIC before that can lawfully happen. And, it can only happen with your consent/election, whether EXPRESS or IMPLIED, according to maxims of the common law:

“Quod meum est sine me auferri non potest. What is mine cannot be taken away without my consent. Jenk. Cent. 251. Sed vide Eminent Domain.”

[Bouvier’s Maxims of Law, 1856; SOURCE: https://famguardian.org/Publications/BouvierMaximsOfLaw/BouviersMaxims.htm]

The burden of proof on the government in exercising tax enforcement authority is to demonstrate:

- OWNERSHIP: Government asserts ownership over the property. MAKE THEM PROVE IT!

1.1. That they own the property before they can determine the laws that protect or exercise control or protect the property. This is an outgrowth of the right to exclude aspect of ownership. By saying the I.R.C. relates to your earnings, they are pretending to be the owner.

1.2. That if they try to change the legal status of the property from PRIVATE to PUBLIC or NONTAXABLE to TAXABLE, they are claiming ownership over the property. Control and ownership are synonymous. If the government pretends you are the owner and yet tries to change it from PRIVATE to PUBLIC without your consent, they are STEALING. - PROPERTY:

2.1. That if the property is INTANGIBLE (not physical), that your domicile as the owner is within the exclusive CIVIL jurisdiction of Congress, since intangible property is almost always taxed at the domicile of the owner. See:

PROOF OF FACTS: Taxation of Intangibles is at the domicile of the owner by default, FTSIG

https://ftsig.org/proof-of-facts-taxation-of-intangibles-is-at-the-domicile-of-the-owner/

2.2. That if the property is TANGIBLE (physical), it is physically located within the exclusive jurisdiction of the national government.

2.3. That if you are in a state of the Union and protected by the constitution, “gross income” or “income” entered on the tax return SHOULD mean only PROFIT ONLY and not GROSS RECEIPTS. If they define it as “gross receipts”, they are both exercising ownership and control over the PRIVATE property and violating the Sixteenth Amendment. A tax on “gross receipts” is a tax on capital instead of income/profit that violates Article 1, Section 2, Clause 3 and Article 1, Section 9, Clause 4 of the constitution as a “direct tax”. The only way the government can get around this limitation is for you to FORGET claiming you are in a state of the Union on your tax return so they don’t have to address the issue or for them to claim that you are a consenting franchisee, which they will never do. Deductions are on the tax return mainly to make the tax LOOK like a tax on “profit”, but its NOT. This is because deductions under 26 U.S.C. §162 are privileged and if Congress gets to define them instead of the common (PRIVATE) law, then the income they go against is also privileged and not private, so they are just a trap to suck you in.