Brushaber (foreign status, dom source)

The case of Brushaber v. Union Pacific Railroad Company, 240 U.S. 1 (1916) is the seminal case heard by the U.S. Supreme Court which acknowledged the ability of a party born and domiciled within the exclusive jurisdiction of a Constitutional State to claim “nonresident alien” status. You can read the case at:

https://scholar.google.com/scholar_case?case=5893140094506516673

We also cover this case separately on our website under the Cases Explained->Major SCOTUS cases menu at the following link;

https://ftsig.org/brushaber-v-union-pacific-railroad-company-240-u-s-1-1916/

You can read filings from the docket below:

- Receipt

- SDNY Equity E11-121 part 1

- SDNY Equity E11-121 part 2

- SDNY Equity E11-121 part 3

- Brushaber v. Union Pacific R. Co., 240 U.S1 (1916) Transcripts, Exhibit #09.031

https://sedm.org/Exhibits/EX09.031.pdf - Brushaber Briefs

- Transcript

- United States

- UP Memo

- Petition

This was the first major tax case heard by the U.S. Supreme court after the Sixteenth Amendment ratification in 1913 and it was based on the Tarriff Act of 1913 enacted that year. Brushaber didn’t challenge his personal tax liability, but the ability of the Union Pacific Railroad corporation to pay the tax against THEMSELVES, which in turn reduced HIS dividends. They were also withholding on his dividends and he objected to the withholding. In modern terms, his case basically challenged the ability of the company to withhold on his earnings, which today is implemented by 26 U.S.C. §3406 and called “Backup withholding”. You can read more about that scenario below:

Lawfully Avoiding Backup Withholding under 26 U.S.C. §3406, FTSIG

https://ftsig.org/lawfully-avoiding-backup-withholding/

This case is one of the most frequently cited cases by the U.S. government and IRS in supporting its position that Subtitle A income taxes are constitutional. It occurred just after the passage of the Sixteenth Amendment in 1916 and became a popular case for the government to cite because it is written in such a confusing way. There is also a large amount of misinformation about this case promoted by the patriot community that we would like to eliminate. Because of this fact, we will spend an unusual degree of attention analyzing the case to remove all doubt about its true significance.

The Union Pacific Railroad

The Union Pacific Railroad was initially established with significant federal support through land grants and loans, as outlined in the Pacific Railway Act of 1862 and 1864. At the time it was formed, Utah was an incorporated Territory. Utah subsequently became a state in 1896 and was a state of the Union at the time the Brushaber case was heard.

The company faced financial difficulties in the 1890s and entered government receivership in 1893 due to the Panic of 1893. It remained under government receivership until the end of 1895.

The Staggers Rail Act of 1980 significantly deregulated the railroad industry, reducing federal oversight and control.

To further distance itself from federal regulation, Union Pacific transferred its non-rail assets to its holding company, Union Pacific Corporation, in 1971. This included properties like Rocky Mountain Energy Company, Upland Industries Corporation, and Champlain Petroleum Company.

In the late 1990s, the Union Pacific Corporation completed a merger with the Southern Pacific Transportation Company, creating the largest railroad network in the United States, as described by Cornerstone Research.

In essence, while Union Pacific began as a company with strong federal ties, it transitioned into a private, although still regulated, entity over time, with the Staggers Rail Act and the transfer of non-rail assets marking key milestones in this transition.

The Brushaber case has been a source of great misunderstanding in the freedom community because of the inaccurate assumption that the Union Pacific Railroad was a federal corporation at the time of the suite. Union Pacific was not a federal corporation in 1916. While the company was initially created and funded by the federal government through the Pacific Railroad Acts of 1862 and 1864, it operated as a private, for-profit company. The Supreme Court case Brushaber v. Union Pacific Railroad Co. in 1916 concerned the validity of a federal income tax, not the status of Union Pacific as a federal entity.

In order for the Union Pacific Railroad to abandon its domestic status, it would have had to make a dedicated effort to UN-DOMESTICATE itself and its successor entities once it was privatized. We have no evidence that it ever attempted to do so. Thus it remained DOMESTIC at the time of this case.

As this website demonstrates, a state corporation such as Union Pacific at the time of this suit, can STILL be DOMESTIC if it makes a domestication election under 26 U.S.C. §7701(a)(4) by filing a domestic tax return under 26 C.F.R. §301.6109-1(g)(2). Union Pacific most likely OUT OF IGNORANCE made this election and therefore behaved at the time just like most state corporations INCORRECTLY do today. In response, the only remedy available for those who deal with such self-defeating ignorance on the part of corporations (or any business for that matter) is to file as a nonresident alien to get the withheld monies back. Frank Brushaber clearly did not do that administratively, or he wouldn’t have filed his suit to begin with.

You can read about the history of the Union Pacific Railroad at:

- Union Pacific Website

https://www.up.com/ - Union Pacific Railroad-Wikipedia

https://en.wikipedia.org/wiki/Union_Pacific_Railroad

Frank Brushaber

Mr. Brushaber owned stock in the Union Pacific Railroad, a corporation chartered in the federal Territory of Utah before it became a Constitutional State. As a territory, Utah was part of the federal United States, and as such, was a “domestic corporation” or “federal corporation” at the time it was formed. Being a creation of Congress, the Union Pacific Railroad Company was found to be a “domestic” corporation under the law. In common, everyday language, the term “domestic” is often used to mean “inside the country”. For example, airports are divided into different areas for domestic and foreign flights, in order to allow Customs agents to inspect the baggage and passports of passengers arriving on flights from foreign countries. However, under federal tax law, the term “domestic” does not mean “inside the country”; it means “inside the United States Corporation” as its agent or officer. Accordingly, a “foreign” corporation is a corporation chartered by a government that OTHER than the “United States Inc.” federal corporation.

Mr. Brushaber filed suit in federal District Court in New York to enjoin the Union Pacific Railroad DOMESTIC corporation from volunteering to pay federal income tax on its profits because he didn’t want his stock dividends correspondingly reduced as a result of the tax. Note that the issue was not him personally paying income taxes on the stock, but the reduction of his dividends by the amount of taxes the corporation insisted on volunteering to pay prior to distributing the remaining profits to its shareholders.

The Case

Treasury Decision 2313 also used the term “domestic stock corporation” in association with Union Pacific Railroad.

The Brushaber case was taken up by SCOTUS to address Brushaber’s misunderstandings of what the effect of the 16th Amendment was.

The lower court’s decision against Brushaber was affirmed, but not on the basis of Union Pacific being a federal corporation.

The real basis was simply that no court could grant the relief Brushaber sought against Union Pacific.

It’s important to note that Union Pacific had voluntarily complied with the (then new) income tax withholding requirements in the 1913 tariff act, and withheld income tax from dividends paid out to Brushaber (a stockholder).

Brushaber sought to enjoin Union Pacific from voluntarily complying with those withholding provisions, on the basis of his many arguments about the unconstitutionality of the 16th Amendment and the new income tax laws.

The lower court had refused to stand in the way of Union Pacific’s voluntary choice to comply with the withholding provision of the new law.

An injunction is an equitable remedy and an extraordinary remedy—available only when the party can establish that irreparable harm would result if the injunction were not granted.

Since Brushaber could be made whole via a refund claim, he had no chance of enjoining Union Pacific from withholding income tax from his stock, even if he could prove they were wrong to do so.

The Brushaber decision ruled that the 16th Amendment did not amend or change the U.S. Constitution. It decided that the federal corporation could not be stopped from volunteering to pay the federal income tax, even though this damaged the interests of its stockholders by reducing their dividends. But don’t take our word for it. Here is what the U.S. Supreme Court, in Brushaber v. Union Pacific Railroad, said in the majority opinion:

“…the proposition and the contentions under [the 16th Amendment]…would cause one provision of the Constitution to destroy another;

That is, they would result in bringing the provisions of the Amendment exempting a direct tax from apportionment into irreconcilable conflict with the general requirement that all direct taxes be apportioned;

This result, instead of simplifying the situation and making clear the limitations of the taxing power, which obviously the Amendment must have intended to accomplish, would create radical and destructive changes in our constitutional system and multiply confusion…

…Moreover in addition the Conclusion reached in the Pollock Case did not in any degree involve holding that income taxes generically and necessarily came within the class of direct taxes on property, but on the contrary recognized the fact that taxation on income was in its nature an excise entitled to be enforced as such unless and until it was concluded that to enforce it would amount to accomplishing the result which the requirement as to apportionment of direct taxation was adopted to prevent, in which case the duty would arise to disregard form and consider substance alone and hence subject the tax to the regulation as to apportionment which otherwise as an excise would not apply to it.

…the Amendment demonstrates that no such purpose was intended and on the contrary shows that it was drawn with the object of maintaining the limitations of the Constitution and harmonizing their operation.”

…the [16th] Amendment contains nothing repudiating or challenging the ruling in the Pollock Case that the word direct had a broader significance since it embraced also taxes levied directly on personal property because of its ownership, and therefore the Amendment at least impliedly makes such wider significance a part of the Constitution — a condition which clearly demonstrates that the purpose was not to change the existing interpretation except to the extent necessary to accomplish the result intended, that is, the prevention of the resort to the sources from which a taxed income was derived in order to cause a direct tax on the income to be a direct tax on the source itself and thereby to take an income tax out of the class of excises, duties and imposts and place it in the class of direct taxes…

Indeed in the light of the history which we have given and of the decision in the Pollock Case and the ground upon which the ruling in that case was based, there is no escape from the Conclusion that the Amendment was drawn for the purpose of doing away for the future with the principle upon which the Pollock Case was decided, that is, of determining whether a tax on income was direct not by a consideration of the burden placed on the taxed income upon which it directly operated, but by taking into view the burden which resulted on the property from which the income was derived, since in express terms the Amendment provides that income taxes, from whatever source the income may be derived, shall not be subject to the regulation of apportionment…

[Brushaber v. Union Pacific Railroad, 240 U.S. 1, 12-18 (1916);

SOURCE: https://scholar.google.com/scholar_case?case=5893140094506516673]

And it further stated that taxes on income had been “sustained as excises in the past.” The ruling established that income tax is constitutional as an indirect excise tax on profit DERIVED from “domestic” property or affiliated enterprise, not as a direct tax on the property that PRODUCED the profit. The measure of whether it is a direct or an indirect/excise tax is determined by the burden the tax places is on the income/profit derived FROM the “domestic” PROPERTY or affiliated enterprise, rather than the CLASS that property falls within.

Later cases confirmed this interpretation by noting that it in essence EXPANDED the definition of property that excise taxes upon the PROFIT from such property can be imposed upon, since the original Pollock case was only a tax on “real estate” that did not include personal property:

“In 1895, we expanded our interpretation to include taxes on personal property and income from personal property, in the course of striking down aspects of the federal income tax. Pollock v. Farmers’ Loan & Trust Co., 158 U.S. 601, 618, 15 S.Ct. 912, 39 L.Ed. 1108 (1895). That result was overturned by the Sixteenth Amendment, although we continued to consider taxes on personal property to be direct taxes. See Eisner v. Macomber, 252 U.S. 189, 218–219, 40 S.Ct. 189, 64 L.Ed. 521 (1920).”

[Nat’l Fed’n of Indep. Bus. v. Sebelius, 567 U.S. 519, 571 (2012);

SOURCE: https://scholar.google.com/scholar_case?case=12815172896965834886]

NOTE: A tax on “gross receipts” is a tax on PROPERTY and not PROFIT DERIVED from property. Thus it is STILL an unconstitutional direct tax. This was confirmed by cases after Brushaber, such as this one two years later:

“We must reject in this case, as we have rejected in cases arising under the Corporation Excise Tax Act of 1909 (Doyle, Collector, v. Mitchell Brothers Co., 247 U.S. 179, 38 Sup. Ct. 467, 62 L. Ed.–), the broad contention submitted on behalf of the government that all receipts—everything that comes in-are income within the proper definition of the term ‘gross income,’ and that the entire proceeds of a conversion of capital assets, in whatever form and under whatever circumstances accomplished, should be treated as gross income. Certainly the term “income’ has no broader meaning in the 1913 act than in that of 1909 (see Stratton’s Independence v. Howbert, 231 U.S. 399, 416, 417 S., 34 Sup. Ct. 136), and for the present purpose we assume there is not difference in its meaning as used in the two acts.”

[Southern Pacific Co., v. Lowe, 247 U.S. 330, 335, 38 S.Ct. 540 (1918);

SOURCE: https://scholar.google.com/scholar_case?case=9702563774965412467]

Application of the case

The IRS relies on the Brushaber decision to prove the constitutionality of the income tax on natural persons, but ignores the Court’s ruling in that case that the income tax is an excise tax and that the “person” paying the tax in this case was a federal corporation rather than a natural person. The government and the IRS like to cite this case because the case was written in an especially confusing way.

This case provides an essential lesson in how to aver your status as a Fourteenth Amendment citizen to be recognized by the courts as a “nonresident alien”. This was the SECOND case where a state citizen properly averred their status as a nonresident alien. The first was Pollock v. Farmers Loan and Trust, 157 U.S. 429 (1895). We explain how to properly aver your status as a state political citizen in the following article:

How to Aver Your Status as a Fourteenth Amendment “nonresident alien”, FTSIG

https://ftsig.org/how-to-aver-your-status-as-a-fourteenth-amendment-nonresident-alien/

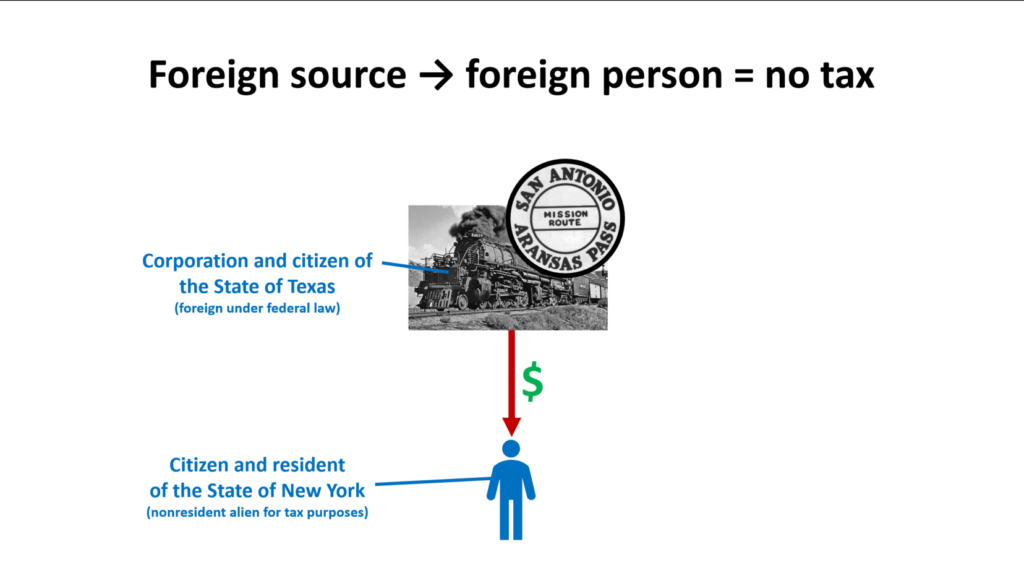

This case also explains the applicability of income taxation to “U.S. source” payments under 26 U.S.C. §871(b), where Frank Brushaber had invested in the stock of a privileged state corporation in Utah that made a domestic election. The corporation was deducting taxes on the dividends paid to his nonresident alien investors. Since the Union Pacific Railroad was a privileged domestic corporation, it was WITHIN the United States government as an instrumentality of said government.

This case was heard by Justice Edward Douglas White, who also served on the U.S. Supreme Court at the time the famous case of Pollock v. Farmers Loan and Trust, 157 U.S. 429 (1895) was also heard. He was a dissenting justice in that case and finally got his way in this case.

The main takeaways of the case are that:

- If you as a Fourteenth Amendment “citizen of the United States**” want to be recognized as a “nonresident alien” by the courts, you must aver your status in the following form:

Citizen of the State of Florida residing in Volusa County” - Earnings from federal instrumentalities such as federally chartered corporations count as a “source within the United States**” under 26 U.S.C. §871.

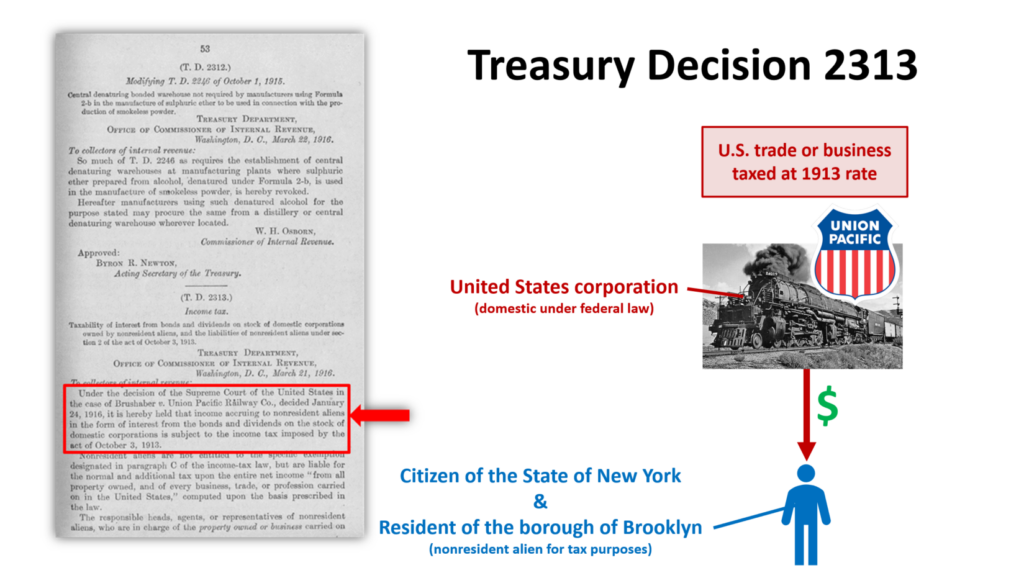

The output of this case was the publication of Treasury Decision 2313 identifying Mr. Brushaber, a Fourteenth Amendment political citizen domiciled in New York at the time, as a “nonresident alien”. You can read the entire text of Treasury Decision 2313 below:

Treasury Decision Under Internal Revenue Laws of the United States

Vol. 18 January-December 1916

W. G. McAdoo Secretary of the Treasury

Washington Government Printing Office 1917

T.D. 2313 Income Tax

Taxability of interest from bonds and dividends on stock of domestic corporations owned by nonresident aliens, and the liabilities of nonresident aliens under section 2 of the act of October 3, 1913.

Treasury Department Office of Commissioner of Internal Revenue Washington, D.C., March 21, 1916

To collectors of internal revenue:

Under the decision of the Supreme Court of the United States in the case of Brushaber v. Union Pacific Railway [sic] Co., decided January 24, 1916, it is hereby held that income accruing to nonresident aliens in the form of interest from the bonds and dividends on the stock of domestic corporations is subject to the income tax imposed by the act of October 3, 1913.

Nonresident aliens are not entitled to the specific exemption designated in paragraph C of the income-tax law, but are liable for the normal and additional tax upon the entire net income “from all property owned, and of every business, trade, or profession carried on in the United States,” computed upon the basis prescribed in the law.

The responsible heads, agents, or representatives of nonresident aliens, who are in charge of the property owned or business carried on within the United States, shall make a full and complete return of the income therefrom on Form 1040, revised, and shall pay any and all tax, normal and additional, assessed upon the income received by them in behalf of their nonresident alien principals.

The person, firm, company, copartnership, corporation, joint-stock company, or association, and insurance company in the United States, citizen or resident alien, in whatever capacity acting, having the control, receipt, disposal, or payment of fixed or determinable annual or periodic gains, profits, and income of whatever kind, to a nonresident alien, under any contract or otherwise, which payment shall represent income of a nonresident alien from the exercise of any trade or profession within the United States, shall deduct and withhold from such annual or periodic gains, profits, and income, regardless of amount, and pay to the officer of the United States Government authorized to receive the same such sum as will be sufficient to pay the normal tax of 1 per cent imposed by law, and shall make an annual return on Form 1042.

The normal tax shall be withheld at the source from income accrued to nonresident aliens from corporate obligations and shall be returned and paid to the Government by debtor corporations and withholding agents as in the case of citizens and resident aliens, but without benefit of the specific exemption designated in paragraph C of the law.

Form 1008, revised, claiming the benefit of such deductions as may be applicable to income arising within the United States and for refund of excess tax withheld, as provided by paragraphs B and P of the income-tax law, may be filed by nonresident aliens, their agents or representatives, with the debtor corporation, withholding agent, or collector of internal revenue for the district in which the withholding return is required to

be made.That part of paragraph E of the law which provides that “if such person is absent from the United States the return and application may be made for him or her by the person required to withhold and pay the tax ” is held to be applicable to the return and application on Form 1008, revised, of nonresident aliens.

A fiduciary acting in the capacity of trustee, executor, or administrator, when there is only one beneficiary and that beneficiary a nonresident alien, shall render a return on Form 1040, revised; but when there are two or more beneficiaries, one or all of whom are nonresident aliens, the fiduciary shall render a return on Form 1041, revised, and a personal return on Form 1040, revised, for each nonresident alien beneficiary.

The liability, under the provisions of the law, to render personal returns, on or before March 1 next succeeding the tax year, of annual net income accrued to them from sources within the United States during the preceding calendar year, attaches to nonresident aliens as in the case of returns required from citizens and resident aliens. Therefore, a return on Form 1040, revised, is required except in cases where the total tax liability has been or is to be satisfied at the source by withholding or has been or is to be satisfied by personal return on Form 1040, revised, rendered in their behalf. Returns shall be rendered to the collector of internal revenue for the district in which a nonresident alien carries on his principal business within the United States or, in the absence of a principal business within the United States and in all cases of doubt, the collector of internal revenue at Baltimore, Md., in whose district Washington is situated.

Nonresident aliens are held to be subject to the liabilities and requirements of all administrative, special, and general provisions of law in relation to the assessment, remission, collection, and refund of the income tax imposed by the act of October 3, 1913, and collectors of internal revenue will make collection of the tax by distraint, garnishment, execution, or other appropriate process provided by law.

So much of T.D. 1976 as relates to ownership certificate 1004, T.D. 1977 (certificate Form 1060), 1988 (certificate Form 1060), T.D. 2017 (nontaxability of interest from bonds and dividends on stock), T.D. 2030 (certificate Form 1071), T.D. 2162 (nontaxability of interest from bonds and dividends on stock) and all rulings heretofore made which are in conflict herewith are hereby superseded and repealed.

This decision will be held effective as of January 1, 1916.

W. H. Osborn Commissioner of Internal Revenue

Approved, March 30, 1916:

Byron R. Newton, Acting Secretary of the Treasury

For a PDF version of the above, see:

Frank R. Brushaber Genealogical Records, SEDM Exhibit #09.034. Contains Treasury Decision 2313 recognizing Brushaber as a nonresident alien.

https://sedm.org/Exhibits/EX09.034.pdf