Which “United States”?: HOW to discern meaning between GEOGRAPHICAL and CORPORATE based on statutory context

TABLE OF CONTENTS

- Introduction

- THREE contexts: Civil, Political, Corporate

2.1. Political Context

2.2. Civil Context

2.3. Corporate/Government Context - Geographical v. Corporate Confusion in the I.R.C.

- Identity Laundering Results when “United States” is misconstrued

- Key to Discerning Geographical v. Corporate: Owner and Type of Property/Right involved

5.1. Tangible v. Intangible Property

5.2. Domicile of the Owner of the Property

5.3. Tax Home - Purely GEOGRAPHICAL scenarios

- Purely CORPORATE/GOVERNMENTAL scenarios

- Application to “source within the United States” scenarios in I.R.C. 861 and 862

- Burden of Proof When there is Doubt About the Meaning of “United States”

- Conclusions

- Further reading

1. Introduction

For a brief, one page summary of this page, see:

HOW TO: Understanding the meaning of the term “United States”

https://ftsig.org/how-to-understanding-the-meaning-of-the-term-united-states/

When reading statutes and regulations, it is VERY important to be able to distinguish WHICH “United States” is used within a specific context so that the reader can discern what the proper audience is for the person or property being referenced.

In reference to the term “United States”, the GOVERNMENT has an interest in making you believe that:

- “United States” is ALWAYS used in its GEOGRAPHICAL sense as defined in 26 U.S.C. §7701(a)(9) and (a)(10).

- The term “State” defined in 26 U.S.C. §7701(a)(10) includes states of the Union even though they are never expressly included in any I.R.C. definition applying specifically to Subtitle A income tax.

- There is NO SUCH THING as “federal States”, meaning states operating as non-geographical agents of the national government in handling the community property of the national government, such as “taxpayer” offices that it legislatively creates. Federalist Paper #36 talks about “revenue officers” which today are nothing but “taxpayers”, for instance.

- There is NO DIFFERENCE between the sovereign and independent POLITICAL “States” mentioned in the Constitution and the CIVIL “States” mentioned in 26 U.S.C. §7701(a)(10) and 4 U.S.C. §110(d).

- EVERYONE in the COUNTRY “United States*” is subject to the Internal Revenue Code whether they want to be or not, and thus is a “taxpayer”.

The above are examples of what we call “equivocation”, where the government wants you to believe that all contexts for the words “State” and “United States” apply to the singular geographical context and that there is no difference between the CIVIL context and the POLITICAL/CONSTITUTIONAL context for these words. The following two definitions are provided for comparison to demonstrate such equivocation:

26 U.S.C. §7701– Definitions

(a)When used in this title, where not otherwise distinctly expressed or manifestly incompatible with the intent thereof—

(9)United States

The term “United States” when used in a geographical sense includes only the States and the District of Columbia.

The term “State” shall be construed to include the District of Columbia, where such construction is necessary to carry out provisions of this title.

_________________________

26 U.S.C. §4612– Definitions and special rules

(a) Definitions

For purposes of this subchapter [subchapter A]–

(4) United States

(A) In general

The term ”United States” means the 50 States, the District of Columbia, the Commonwealth of Puerto Rico, any possession of the United States, the Commonwealth of the Northern Mariana Islands, and the Trust Territory of the Pacific Islands.

They want to do this to illegally and unconstitutionally expand the application of tax franchise codes to increase their revenue while destroying the separation of powers built into the constitution. For a detailed explanation of the many reasons why just about EVERYTHING that any government does involves this kind of unscrupulous equivocation, see:

FAQ: Why does just about EVERYTHING the government does involve EQUIVOCATION?, FTSIG

https://ftsig.org/faq-why-does-just-about-everything-the-government-does-involve-equivocation/

2. THREE contexts: Civil, Political, Corporate

2.1. Political Context

The constitution is a POLITICAL document which is tied geographically to specific LAND. That is why it calls itself “the LAW of the LAND”. That land is within the exterior boundaries of:

- States of the Union:

1.1. A political subdivision called a “State” within the Constitution mentioned in Article IV.

1.2. These areas are protected by the Bill of Rights and protected by states of the Union for internal affairs purposes.

1.3. Political citizens born or naturalized here are described in the Fourteenth Amendment, 26 C.F.R. §1.1-1(c) and 8 U.S.C. §1401. - Territories, possessions, and enclaves within the Constitutional “States” under exclusive jurisdiction of Congress:

2.1. Not expressly identified in the Constitution under Article 1, Section 8, Clause 17 and Article 4, Section 3, Clause 2.

2.2. These areas are not protected by the Bill of Rights unless by express Act of Congress. Those so protected are called Organized Territories.

2.3. Political context of people who live here is described in Title 8 of the U.S. Code.

2.4. POLITICAL “citizens” born or naturalized here are described in 8 U.S.C. §§1402-1407

Congress ALWAYS legislates for ONE or the OTHER of the above two jurisdictions separately, as admitted in the famous case of Cohens v. Virginia:

Congress, as a legislative body, exercise two species of legislative power: the one, limited as to its objects, but extending all over the Union: the other, an absolute, exclusive legislative power over the District of Columbia. The preliminary inquiry in the case now before the Court, is, by virtue of which of these authorities was the law in question passed? When this is ascertained, we shall be able to determine its extent and application. In this country, we are trying the novel experiment of a divided sovereignty, between the national government and the States. The precise line of division between these is not always distinctly marked. Government is a moral not a mathematical science; and the powers of such a government especially, cannot be defined with mathematical [*435] accuracy and precision. There is a competition of opposite analogies. We arrive at a just conclusion by reasoning from these analogies, and by a general regard to the objects and purposes of this scheme of government. With a view to the present question, it may, perhaps, be [***223] safely admitted, that there are certain acts of legislation passed by Congress, with a local reference to this District, which proceed from the general powers with which Congress are invested. They are local in their immediate operation and effect, but they are passed in virtue of general legislative powers.

[Cohens. v. Virginia, 19 U.S. 264 (1821)]

Which of the above two jurisdiction applies is determined by how you aver your status in court pleadings. It is VERY important to correctly aver your status. If you don’t, you will be PRESUMED to be domiciled in Item 2 above subject to the exclusive civil jurisdiction of Congress. See:

How to Aver Your Status as a Fourteenth Amendment “nonresident alien”, FTSIG

https://ftsig.org/how-to-aver-your-status-as-a-fourteenth-amendment-nonresident-alien/

On this site, the POLITICAL context is synonymous with United StatesP political/nation. The POLITICAL sense is the DEFAULT sense in most acts of Congress per Texas v. White, 74 U.S. 700 (1869); SOURCE: https://scholar.google.com/scholar_case?case=1134912565671891096.

When one has a POLITICAL citizen status but CIVIL non-citizen status, they are PRIVATE. The act of pursuing a benefit or privilege turns an exclusively POLITICAL citizen into a CIVIL citizen and makes you PUBLIC and an agent or servant of the state.

2.2. Civil Context

CIVIL context encompasses the reach of CIVIL legislative power of Congress to manage its federal offices, privileges, territories, possessions, and enclaves under item 2 in the previous section. Civil jurisdiction:

- Is always GEOGRAPHICAL because it is BASED on DOMICILE within that geography.

- Is determined by the VOLUNTARY GEOGRAPHICAL DOMICILE of the parties to a lawsuit, based on Federal Rule of Civil Procedure 17.

- Applies to the geography identified by the exterior limits of a specific political body.

- Relates to PERSONS and TANGIBLE PROPERTY physically within the exterior limits of the political body tied to the domicile of the owner.

- Does NOT apply to TANGIBLE property physically situated OUTSIDE the territorial limits of the taxing power.

The CIVIL context is the only audience for obligations found in the Internal Revenue Code. Because it depends on Domicile, it can apply only to CIVIL “PERSONS” either:

- VOLUNTARILY domiciled within the exclusive jurisdiction of Congress or

- REPRESENTING a fiction that is domiciled within the exclusive jurisdiction of Congress.

The above two methods of acquiring civil statutory jurisdiction are recognized in Federal Rule of Civil Procedure 17. The obligations and privileges (public rights) attached to CIVIL STATUTORY “persons”, “citizens”, and “residents” represent a fictional office and PUBLIC property of Congress or legislatively granted to those who elect to become surety for said office by invoking the status on a government form such as a 1040. That grant of PUBLIC property r privileges, in fact, CREATES the OFFICE of “person”, “citizen”, and “resident” of those pursuing the status because a “public officer” is legally defined as someone in charge of the PROPERTY of the public.

“Public office. The right, authority, and duty created and conferred by law, by which for a given period, either fixed by law or enduring at the pleasure of the creating power, an individual is invested with some portion of the sovereign functions of government for the benefit of the public. Walker v. Rich, 79 Cal.App. 139, 249 P. 56, 58. An agency for the state, the duties of which involve in their performance the exercise of some portion of the sovereign power, either great or small. Yaselli v. Goff, C.C.A., 12 F.2d. 396, 403, 56 A.L.R. 1239; Lacey v. State, 13 Ala.App. 212, 68 So. 706, 710; Curtin v. State, 61 Cal.App. 377, 214 P. 1030, 1035; Shelmadine v. City of Elkhart, 75 Ind.App. 493, 129 N.E. 878. State ex rel. Colorado River Commission v. Frohmiller, 46 Ariz. 413, 52 P.2d. 483, 486. Where, by virtue of law, a person is clothed, not as an incidental or transient authority, but for such time as de- notes duration and continuance, with Independent power to control the property of the public, or with public functions to be exercised in the supposed interest of the people, the service to be compensated by a stated yearly salary, and the occupant having a designation or title, the position so created is a public office. State v. Brennan, 49 Ohio.St. 33, 29 N.E. 593.

[Black’s Law Dictionary, Fourth Edition, p. 1235]

2.3. Corporate/Government Context

The corporate or government context is the main legal vehicle the I.R.C. uses to reach private personsPRI like you. Elections in the I.R.C. are the method of recruiting you INTO this corporation through CIVIL statutes. Upon voluntary recruitment you are called an “officer” in a legal sense but the courts NEVER refer to you as a “PUBLIC officer” mainly because they the want the “benefits” of your servitude and voluntary surety but absolutely refuse the OBLIGATIONS that also go with those benefits. This SCAM is explained in:

Copilot: Why courts refuse to call those voluntarily subject to civil statutory law “public officers”, FTSIG

https://ftsig.org/copilot-why-courts-refuse-to-call-those-voluntarily-subject-to-civil-statutory-law-public-officers/

A corporation, in turn, is not physical but virtual. It is a fiction of law that has no geography, but it can still have a geographical corporate headquarters which the courts call a SITUS. The SITUS of a corporation is the effective DOMICILE of the corporation for the purposes of determining taxation mainly of INTANGIBLE property. TANGIBLE property is always taxed at the geographical location that it is physically located. This situation was described by the U.S. Supreme Court as follows:

“Since the corporate personality is a fiction, although a fiction intended to be acted upon as though it were a fact, Klein v. Board of Supervisors, 282 U.S. 19, 24, it is clear that unlike an individual its “presence” without, as well as within, the state of its origin can be manifested only by activities carried on in its behalf by those who are authorized to act [AGENTS and OFFICERS such as “taxpayers” and “persons”] for it. To say that the corporation is so far “present” there as to satisfy due process requirements, for purposes of taxation or the maintenance of suits against it in the courts of the state, is to beg the question to be decided. For the terms “present” or “presence” are used merely to symbolize those activities of the corporation’s agent [OFFICER] within the state which courts will deem to be sufficient to satisfy the demands of due process. L. Hand, J., in Hutchinson v. Chase & Gilbert, 45 F.2d 139, 141. Those demands may be met by such contacts [or FRANCHISES, which are ALSO contracts] of the corporation with the state of the forum as make it reasonable, in the context of our federal system of government, to require the corporation to defend the particular suit which is brought there. An “estimate of the inconveniences” which would result to the corporation from a trial away from its “home” or principal place of business [tax home, 26 C.F.R. §301.7701(b)-2(c)] is relevant in this connection. Hutchinson v. Chase & Gilbert, supra, 141.”

[International Shoe Co. v. Washington, 326 U.S. 310, 316-317 (1945); SOURCE: https://scholar.google.com/scholar_case?case=5514563780081607825]

Corporations can own both TANGIBLE (physical) and INTANGIBLE (non-physical or incorporeal) property. A corporation itself is simply a collection of two great classes of property:

- Offices: These are the officers, agents, and contractors who RUN the corporation. Since Governmental OFFICES are legislatively created by Congress, they are PROPERTY of Congress.

- Property: This includes TANGIBLE and INTANGIBLE of every description.

Since offices are a type of property, then you could truthfully say that “government” is just a collection of public/shared property owned by those who created it. The constitution is a political document that CREATED the government, and it is a trust indenture. The purpose of all trusts is to manage PROPERTY. The “trustees” within the Constitution as a trust indenture are the people called “government”, which collectively is a great corporation. The “government” works for “the State” who are defined as a collection of people, territory, and laws. Those PEOPLE are the sovereigns, and not the government that SERVES them.

“State. A people permanently occupying a fixed territory bound together by common-law habits and custom into one body politic exercising, through the medium of an organized government, independent sovereignty and control over all persons and things within its boundaries, capable of making war and peace and of entering into international relations with other communities of the globe. United States v. Kusche, D.C.Cal., 56 F.Supp. 201 207, 208. The organization of social life which exercises sovereign power in behalf of the people. Delany v. Moralitis, C.C.A.Md., 136 F.2d 129, 130. In its largest sense, a “state” is a body politic or a society of men. Beagle v. Motor Vehicle Acc. Indemnification Corp., 44 Misc.2d 636, 254 N.Y.S.2d 763, 765. A body of people occupying a definite territory and politically organized under one government. State ex re. Maisano v. Mitchell, 155 Conn. 256, 231 A.2d 539, 542. A territorial unit with a distinct general body of law. Restatement, Second, Conflicts, §3. Term may refer either to body politic of a nation (e.g. United States) or to an individual government unit of such nation (e.g. California).

[…]

The people of a state, in their collective capacity, considered as the party wronged by a criminal deed; the public; as in the title of a cause, “The State vs. A.B.”

[Black’s Law Dictionary, Sixth Edition, p. 1407]

On this site, the CORPORATE/GOVERNMENT context is synonymous with United StatesJ , meaning all federal property, offices, agents, contracts, etc. Federal supremacy applies to this collection of property.

“Domestic” (26 U.S.C. §7701(a)(4))= Government Sourced AND within the Geographical jurisdiction. The term “domestic” has the following contexts on this site:

- DomesticC=Civilly Domestic, meaning activity WITHIN the government corporation.

- DomesticS=DomesticC Sourced government payment originating from government created and owned civil statutory entity or status=USPI=United StatesJ.

- DomesticG = Geographically DomesticS and earned within the Federal locality (50 States & D.C. geographically) where said subject matter is relevant=“United StatesG” per under I.R.C. Subtitle A, Chapter 1, Subchapter N.

- DomesticGOV=Domestic Government. The jurisdiction linked to United StatesJ operating within DomesticG.

- DomesticJ=within the civil jurisdiction of the DomesticGOV by virtue of using, asking for, or receiving public property including civil Domestic Statutory Capacity (DSC) recognized in Federal Rule of Civil Procedure 17(b) as the origin of civil jurisdiction.

DomesticC describes the nature of government. United StatesG describes the locality of government. But Neither domesticC nor United StatesG means government. DomesticS above is nested inside of domesticC, leading the unwitting person to believe that it’s $$$ earned upon the land that is taxed, rather than Federal activity within or without its local taxing jurisdiction.

But it’s the Federal nexus (public property) that is taxed. And that nexus may occur in either a domestic locality (within the United StatesG) or in a non-domestic locality (without the United StatesG). The underlying government source is always domestic —domesticS. But it can occur within or without the United StatesG —domesticG.

We know domesticC is government, because it’s tied to corporations and partnerships created under the laws of the United States. Once they establish that throughout the IRC implicitly, they subdivide such domesticC activity as taking place either within or without United StatesG, where:

- Within United StatesG = domesticC activity occurring within the domesticG locality; or

- Without the United StatesG = domesticC activity occurring without the domesticG locality.

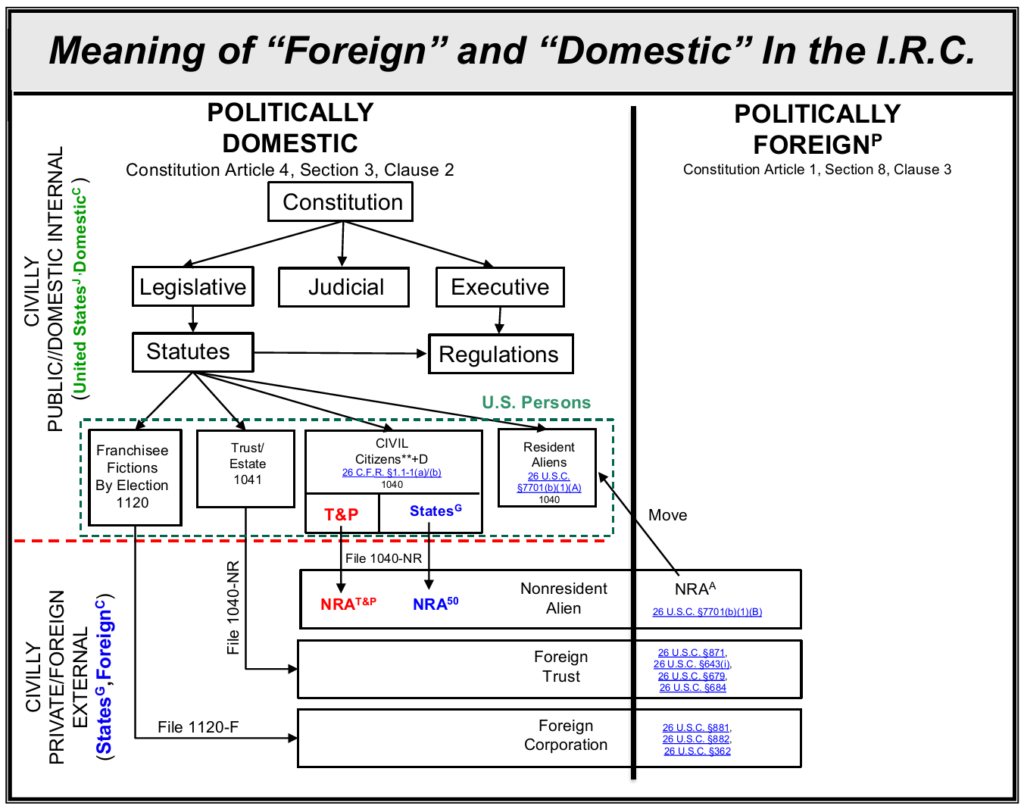

But domesticC is the unspoken default scenario throughout the IRC. This confusion is deliberate. So we’re over the target. This is why pictures and diagrams are helpful—critical in fact. In the diagram below:

- domesticC relates to ALL government-connected subject matter=USPI=USPI=United StatesJ

- domesticG relates to the Federal locality (50 States & D.C. geographically) where said subject matter is relevant.=United StatesG

3. Geographical v. Corporate Confusion in the I.R.C.

The geographical context of “United States” is the one most familiar to most Americans, but even their understanding of THAT is wrong because they think it means the entire COUNTRY and that the jurisdiction of the national government extends throughout the Country on all subject matters.

The Internal Revenue Code is deliberately obfuscated to make it difficult for the average American to discern whether the context implied is GEOGRAPHCAL or CORPORATE, and WHICH geography is implied:

- United StatesP: Political/nation.

- United States50: 50 bodies politic. No USPI. Private and foreign and constitutionally protected.

- United StatesG: 50 States + DC in their geographical senses. DomesticG locality with respect to United StatesJ

- United StatesJ: All federal property, offices, agents, contracts, etc. Federal supremacy applies. USPI involved.

- United StatesGOV: United States government as a public corporation.

| Category | Definition | Legal Character | Jurisdictional Status | Relationship to Individuals |

|---|---|---|---|---|

| United Statesᴾ | The political nation — the sovereign political entity recognized internationally. | A political/national construct; not a geographical or statutory jurisdiction. | Sovereign in the international sense; not a taxing jurisdiction. | One may be a national or citizen of the political United States, but this does not determine federal statutory status. |

| United States50 | The 50 bodies politic (the States) in their sovereign, constitutional capacities. | Private, foreign, and constitutionally protected relative to federal agencies; no USPI involvement. | Outside federal statutory jurisdiction unless a federal nexus is created. | Individuals domiciled here are private personsPRI, not automatically federal persons. |

| United StatesG | The geographical 50 States + DC. A territorial description, not a political or statutory jurisdiction. | A geographical locality used for territorial reference. | Domesticᴳ relative to United Statesᴶ; does not itself create federal authority. | Individuals physically present here are geographically domestic, but not automatically statutory persons. |

| United StatesJ | The federal jurisdictional zone: federal property, federal offices, federal contracts, federal agencies, federal instrumentalities. | A statutory, administrative, proprietary jurisdiction. USPI is involved. | Federal supremacy applies; this is the actual domain of federal statutes and tax obligations. | Individuals connected to federal property, contracts, or offices may be treated as personsPUB for statutory purposes. |

| United StatesGOV | The federal government as a legal person — the public corporation / sovereign entity created by the Constitution and statutes. | A public corporation (USPI) with legal personality; can own property, sue, be sued, and act through officers. | The source of federal statutory authority; the principal in all federal administrative relationships. | Individuals interacting with United StatesGOV (employment, contracts, benefits, offices) may be treated as agents, officers, or franchise participants, triggering statutory personhood. |

4. Identity Laundering Results when “United States” is misconstrued

Identity laundering occurs in a statutory context when you misconstrue United StatesG (the geography) when the context actually calls for United StatesJ (the corporation). This causes you to be unknowingly assimilated in the the United StatesGOV, as the legal origin of United StatesJ. The most important example of that is found in 26 U.S.C. § 864(b), as described below:

PROOF OF FACTS: “United States” in I.R.C. 871(b), 864(b), and 6671(b) is the United StatesGOV, not a geography, FTSIG

https://ftsig.org/proof-of-facts-united-states-in-i-r-c-871b-864b-and-6671b-is-the-united-statesgov-not-a-geography/

In recognition of the identity laundering that occurs by misconstruing the term “United States”, this site implements symbology to represent the various types of identity laundering that can occur. These operators describe the mechanism by which courts and agencies confuse, substitute, or collapse the two legally distinct meanings of “United States”:

- United Statesᴶ — the legal or consent‑based jurisdiction

- United Statesᴳ — the geographical territory

This distinction is essential for analyzing statutes such as 26 U.S.C. § 871(b), where ECI (a United Statesᴶ concept) is treated as if it were sourced from United Statesᴳ.

| Operator | Symbol | Description |

|---|---|---|

| JI₁ — J→G Substitution | JI₁(UnitedStatesᴶ) | Treats legal/consent‑based presence as geographical presence. |

| JI₂ — G→J Substitution | JI₂(UnitedStatesᴳ) | Treats geographical presence as legal/sovereign presence. |

| JI₃ — Jurisdictional Collapse | JI₃(UnitedStatesᴶ, UnitedStatesᴳ) | Collapses the distinction into an undifferentiated hybrid. |

| JI₄ — Jurisdictional Laundering | JI₄(JURIS[consent]) | Converts consent‑based jurisdiction into geography‑based jurisdiction without acknowledging the conversion. |

The above operators are also described in:

Writing Conventions On This Website, Section 11.7: Jurisdictional‑Identity Operators (JI‑family)

https://ftsig.org/introduction/writing-conventions-on-this-website/#11.7._Jurisdictional

5. Key to Discerning Geographical v. Corporate: Owner and Type of Property/Right involved

When reading the Internal Revenue Code and Treasury Regulations, the key to discerning whether the thing described is GEOGRAPHICAL or CORPORATE comes down to:

- The LEGAL CLASSIFICATION of the property involved as either TANGIBLE or INTANGIBLE.

- The domicile of the CREATOR/OWNER of the property as either DOMESTIC or FOREIGN. Domicile is the origin of “civil status“.

5.1. Tangible v. Intangible Property

Tangible property includes land, buildings, and equipment.

Intangible property includes contracts, franchises, stock, bonds, debt, human labor, services, fiat currency, patents, goodwill, civil obligations, etc.

5.2. Domicile of the Owner of the Property

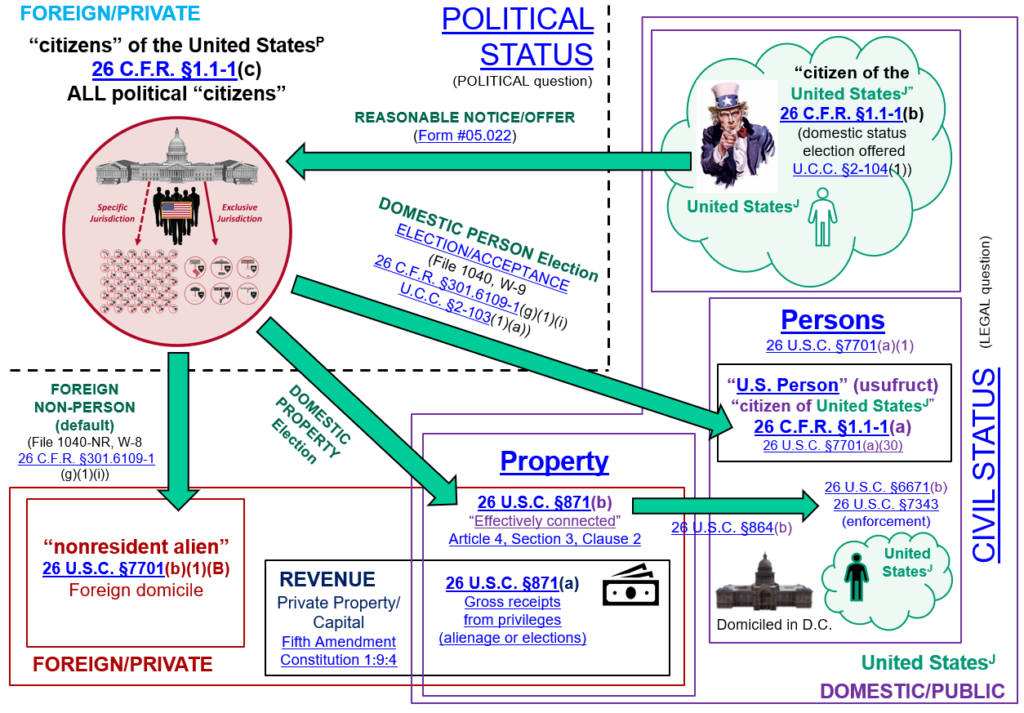

Anything Congress legislatively creates it OWNS. The domicile of the national government as owner of the property is the physical District of Columbia per 4 U.S.C. §72. Every civil legal “person” MUST have a domicile. There cannot be a CIVIL person WITHOUT a DOMICILE.

“It is a settled principle that every person [CIVIL statutory “person”, not human being] must have a domicile somewhere.3 The law permits no individual to be without a domicile,42 and an individual is never without a domicile somewhere.13 Domicile is a continuing thing, and from the moment a person is born he must, at all times, have a domicile .”

[28 Corpus Juris Secundum (C.J.S.), Domicile, §5 Necessity and Number (2003)]

This is NOT to say, however, that a HUMAN BEING MUST have a domicile. Civil domicile must be a voluntary act of civil association in fulfillment of the First Amendment. Those who associate are called CIVIL “citizens” or “residents” and the civil statutory law then becomes the “social compact” you consent to. The civil statutory law, in turn, represents a Private Membership Association (PMA) for those so associated. Those who don’t associate are called foreign, nonresident, and transient foreigners. The result is that you acquire the CIVIL STATUTORY CAPACITY/STATUS (civil status) of “person” and either “citizen” or “resident” and thereby accept the BENEFIT of the civil statutory laws and protection in exchange for the CIVIL obligations that pay for the delivery of those protections.

God, on the other hand, created and therefore literally owns the Heaven and the Earth, and even YOU. As such, all humans are but trustees over His absolutely owned property under the Bible, which, like the Constitution, is a delegation of authority order and trust indenture directing how His property is to be managed by as as his temporary trustees. See:

Delegation of Authority Order from God to Christians, Form #13.007

https://sedm.org/Forms/13-SelfFamilyChurchGovnce/DelOfAuthority.pdf

CIVIL legal taxation:

- Is based exclusively on the legal classification of the property as TANGIBLE or INTANGIBLE

1.1 Taxation of tangible property is based on the physical locality of the property.

1.2. Taxation of intangible property is always at the domicile of the OWNER of the property. - Becomes what the U.S. Supreme Court calls an “extortion” when it:

2.1. Taxes INTANGIBLE property OUTSIDE the domicile of the owner or

2.2. Taxes TANGIBLE property OUTSIDE its physical location.

5.3. Tax Home

26 C.F.R. §301.7701(b)-2(c)(1) defines “tax home” as follows. It is equivalent to “situs” in the context of artificial entities that are businesses, but relates only to “individuals” who are fictions usually:

26 C.F.R. § 301.7701(b)-2 – Closer connection exception

(c) Tax home—

(1) Definition.

For purposes of section 7701 (b) and the regulations under that section, the term “tax home” has the same meaning that it has for purposes of section 162(a)(2) (relating to travel expenses while away from home). Thus, an individual’s tax home is considered to be located at the individual’s regular or principal (if more than one regular) place of business. If the individual has no regular or principal place of business because of the nature of the business, or because the individual is not engaged in carrying on any trade or business within the meaning of section 162(a), then the individual’s tax home is the individual’s regular place of abode in a real and substantial sense.

The “place of business” is the domicile of the OFFICE of “individual” not that of the OFFICER. That would be in the District of Columbia. It establishes that if you don’t occupy said office because you refuse to make any elections. the “tax home” reverts to that of the OFFICER rather than the District of Columbia.

26 U.S.C. §865(g) is an example of the use of “tax home” as a method to ensure that “United States” is used in its geographical context. That 26 U.S.C. §865(g) provision is how you PROVE “United StatesG” is jurisdictional and not simply land we live, work, and walk upon. This argument can also be used to prove this was the concept at work from the beginning (1862)—even before the “U.S. person” status was created in 1962.

26 U.S.C. §865(g)(1)(A)(i)(I) proves that “United StatesG” is representative of a jurisdictional layer (NOT simply a “geographical location within the country” as the general population would have you believe) connected to the domesticC corporate franchise under the principle of federal pre-emption. We know it is, but this proves it.

Here’s why:

- If “United StatesG” was truly representative of simply a geographical LOCATION (i.e., 50 States & D.C. as 51 localities under the Federal Constitution), then having a tax home in a foreign country would convert the “citizen” into a nonresident alien. But it doesn’t—HIS foreign “tax home” (like Cook’s in Cook v. Tait, 265 U.S. 47 (1924)) is IRRELEVANT. That’s because the “United StatesG” represents a domestic jurisdiction appurtenant to LOCAL federal pre-emption associated with the LOCALLY domestic franchise status and not the individual filling it, and why the individual is simply still regarded as a U.S. agent residing abroad and not a nonresident alien.

- Notice the individual’s “tax home” is irrelevant under 26 U.S.C. §911(d)(3), also proving no nexus is associated with the term “individual” by itself. It’s ONLY when the “individual” is VOLUNTARILY connected with the “trade or business” excise taxable franchise through an election of some kind that he becomes a “person” under 26 U.S.C. §6671(b) and 26 U.S.C. §7343.

- The “tax home” (as so defined) relates to the “individual” (not the office—it’s in DC) and can be short in duration and doesn’t constitute a domicile, but a hotel room stay (for example) in the “United StatesG” (because of a stay in a location under Constitution I:8:17).

- It appears that “tax home” relates to the actual person (natural or juristic) and is irrelevant if the U.S. person status is elected. They NEVER discuss the “tax home” of the U.S. person (always in D.C., and therefore domesticC within “United StatesG”), but rather, the officer or entity occupying said status. Thus, take General Electric (GE) for example. They have a “tax home” in Delaware. But unless they establish the foreign status with the IRS, they are still simply functioning as a U.S. agent in Delaware.

- This also explains how a “nonresident alien” under 26 U.S.C. §865(g)(1)(A)(i)(II) can have a “tax home” (as so defined) in the United States and still remain a nonresident alien. It’s because the nonresident alien “foreign person” isn’t, by definition, associated with the franchise.

This EXPLICITLY proves the “individual” is the office and not the officer. Wow! That would be challenging for an unlearned judge to see. But the truth of that analysis is disclosed with sound interpretation of the text and can be used to prove the meaning of “United StatesG” as used IRC-wide.

Thus, Title 26 is a “U.S.-ification scheme under the planks of Marxism. What a TOTAL Mind Fuck!

6. Purely GEOGRAPHICAL scenarios

Throughout the I.R.C. other than 26 U.S.C. §7701(a)(9) and (a)(10) the phrase “geographical United StatesG” is never purely and exclusively expressly invoked so it is purposefully excluded from every invocation of the term “United States” when used. The only scenarios when the geographical “United StatesG” might even be reasonably presumed in the case of Subtitles A (income tax) and Subtitle C (employment tax) are:

- In the context of the GEOGRAPHY that POLITICAL “citizens” are physically BORN within. This is found, for instance, in 26 C.F.R. §1.1-1(c).

- In the context of domicile, which is an VOLUNTARY, First Amendment act of POLITICAL and LEGAL affiliation with people (the “state”) occupying an area within specific geographical boundaries. The Internal Revenue Code only invokes the term “domicile” in subtitle B relating to estate taxes, and never to income taxes in Subtitle A.

- In the context of the physical “presence test” in 26 U.S.C. §7701(b) relating only to “alien individuals”. American nationals are not aliens so they wouldn’t be governed by this provision. In this context, the regulation at 26 C.F.R. §301.7701(b)-1(c)(2)(ii) EXPANDS the DEFAULT geographical definition of “United StatesG” at 26 U.S.C. §7701(a)(9) and (a)(10) to ADD the LEGISLATIVELY FOREIGN states of the Union mentioned in the Constitution ONLY for the purposes of the presence text but not tax liability generally.

- In the context of income NOT connected with the “trade or business”/public office franchise in 26 U.S.C. §871(a). That “United StatesG” is territorial as confirmed by 26 C.F.R. §1.45R-1(a)(23) in the case of real property located in the statutory geographical “United StatesG” subject to depreciation under 26 U.S.C. §871(a).

- In connection with the taxation of what the U.S. Supreme Court calls TANGIBLES, which are always PHYSICAL objects such as land, equipment, chattel, and buildings.

- In connection with “U.S. persons” abroad in reference to whether they are in a “foreign country”. See 26 C.F.R. §1.911-2(g) and (h) and Arnett v. Comm’r, 473 F.3d. 790 (2007).

7. Purely CORPORATE/GOVERNMENTAL scenarios

As we previously said, taxation of INTANGIBLES depends on the DOMICILE of the OWNER. Since domicile is voluntary, then taxation based on domicile is voluntary. To avoid the tax, one:

- Avoids having a civil domicile within the civil geographical jurisdiction of the taxing authority if they are the owner.

- Avoids WORKING for the owner as an AGENT if they are NOT the owner. If the owner is the national government, then such agents would be:

2.1. “U.S. persons” under 26 U.S.C. §7701(a)(30) or

2.2. “Employees” under 26 U.S.C. §3401(c).

Examples of intangibles subject to taxation in the Internal Revenue Code:

- “trade or business”: Defined as “the functions of a public office” in 26 U.S.C. §7701(a)(26).

1.1. Since a public office is a non-physical fiction of law, then taxation of the office is unavoidably imposed upon the CREATOR and therefore OWNER of the office.

1.2. “in the United States” in this context means INSIDE the corporation, not inside any GEOGRAPHY. - Services or labor: Services and labor involve the USE of either TANGIBLE or INTANGIBLE property to accomplish a result desired by those PAYING for the services or labor. Since the property affected by the service can be TANGIBLE or INTANGIBLE, the service or labor need not always be performed at the LOCATION of the property. This is because INTANGIBLE property has no LOCATION per se. Taxation of this type of property is imposed upon the OWNER of the service or labor performed.

2.1. If you performed the labor by yourself and for yourself, you would be the “taxpayer”.

2.2. If you performed services or labor for someone else for profit, taxation would fall on the company you were acting as an AGENT of at the time the service was performed. This type of labor would then be performed “in the United States” federal corporation rather than a geography. - Stock or investment transactions: These always involve INTANGIBLE property that has no physical location. Taxation is usually upon the GAIN from the investment by the OWNER of the stock or investment.

The Internal Revenue Code tries to gloss over these nuances by NEVER mentioning “domicile” in the context of Subtitle A and C. This deliberate obfuscation is designed to HIDE the origin of the taxing power of Congress so that you can be deceived into paying taxes that you usually do not owe.

The TYPE of property that is the SUBJECT of a specific tax identified in 26 U.S.C. §61 and §861 can tell us:

- Who the OWNER must be in the context of the tax.

- Whether either WE or the GOVERNMENT is the owner.

- Whether we are acting as an AGENT of the government if the tax is on INTANGIBLE property.

8. Application to “source within the United States” scenarios in I.R.C. 861 and 862

For the purposes of income sourcing rules, 26 U.S.C. §2(d) dictates that 26 U.S.C. §871 is the sole rule for sourcing in the case of nonresident aliens and NOT 26 U.S.C. §861 or 26 U.S.C. §862. There are occasions when the regulations for 26 U.S.C. §871 such as 26 C.F.R. §1.871-7(a)(1) point back to 26 U.S.C. §861/862 but they are rare and they limit themselves to aliens. Note that for 26 C.F.R. §1.871-7, a “nonresident alien individual” is an alien unless notice is given otherwise. An American national only becomes a “nonresident alien individual” when they pursue privileged deductions under 26 U.S.C. §873(b)(3). Otherwise, they remain civil “non-persons” and nonresidents everywhere in the world under the presence test in 26 U.S.C. §7701(b).

Within 26 U.S.C. §7701(a)(9), the geographical “United States” means:

- The political sense—which is the principal sense per Texas v. White, 74 U.S. 700 (1869); SOURCE: https://scholar.google.com/scholar_case?case=1134912565671891096. This is why no explicit definition is needed. Without a definition, the principal sense is regarded. . . .AND

- The geographical sense—the 50 states + D.C. collectively, which circumscribes a domestic and local taxing jurisdiction per Great Cruz Bay, Inc., St. John v. Wheatley, 495 F.2d. 301 (1974); SOURCE: https://scholar.google.com/scholar_case?case=18118242110028613875.

Government/corporate is embraced by “domestic”—not “United States.” And it makes sense that they would do it that way—they camouflage the most important truths!

The government/corporate source is embraced by the meaning of “domestic” in 26 U.S.C. §7701(a)(4)—that is, “domestic” is used in:

- The geographical sense CONJOINED WITH

- The governmental sense

The above are consistent with Article 1, Section 8, Clause 1 power of excise taxation of Congress found in the Constitution. 26 U.S.C. §7701(a)(4), when applied to a corporation, would certainly embrace the Federal government, since the Federal government is a corporation. There are 208 instances of the term “domestic” in Title 26 of the U.S. Code, and they are all consistent with the above. The government/domestic sense IN TURN always becomes connected to a transaction by an election of some kind, such as an “effectively connected” (26 U.S.C. §864) election or “domestic” election (U.S. person).

But they *NEVER* use the term “United States” to mean solely and exclusively “the government” or the corporation. To do so would make the scheme too obvious. They hide it behind the non-geographical sense of the term “domestic.” and conjoin it WITH the geographical “United States” so you think the tax is PURELY geographical and has NOTHING to do with elections of any sort.

We will now apply these concepts to the term “United States” as used in 26 U.S.C. §§861 and 862 when describing income from WITHIN and WITHOUT the “United States” for the purposes of those mainly who have a DOMESTIC and not FOREIGN status, such as “U.S. persons” in 26 U.S.C. §7701(a)(30). These two sections determine “sources within and without the United States” for both DOMESTICC “U.S. persons” and RARELY FOREIGNC “nonresident aliens”:

- 26 U.S.C. §861 sources *WITHIN* the United States= government/corporate source (domestic) obtained *WITHIN* the domestic United StatesG.

- 26 U.S.C. §862 sources *WITHOUT” the United States= government/corporate source (domestic) obtained *WITHOUT* the domestic United StatesG (i.e., territories and possessions or foreign countries).

NEVER do the above two include PRIVATE sources, no matter WHERE they come from or by whom they are earned, because they are all FOREIGN rather than DOMESTIC. Interfering with, regulating, or taxing in that scenario would be an interference in the private right to contract and associate. So to summarize:

- We don’t believe the political sense is used in either 26 U.S.C. §861 or 26 U.S.C. §862.

- “United States” = Political OR Geographical sense. When they use “United StatesG“, there is ALWAYS an understood or underlying Federal government nexus. But it is by virtue of the “domestic” (governmental source) via a “domestic” geographical jurisdiction. This provides maximum camouflage.

- The government/corporate nexus is NEVER explicitly revealed. Rather, it is done implicitly within 26 U.S.C. §861 or 26 U.S.C. §862.

- What’s so tricky about the scheme is they blur the lines between “United States” (2 meanings) and domestic (2 contexts). But they never call the government the “United States”—rather, they obliquely refer to the taxable government property as being domesticC, and categorize it as being either within the “United StatesG” (domesticG), or without “United StatesG” (non-domesticG).

The only thing the government can manage, tax, or regulate per the Constitution as a trust indenture is PUBLIC property that is the corpus of the trust. This is consistent with 44 U.S.C. §1505(a) and 5 U.S.C. §553a(a)(2), which say that implementing regulations are required where PRIVATE property is involved. There are not enforcement implementing regulations for I.R.C. Subtitle A. Justice itself REQUIRES that PRIVATE property must be LEFT ALONE, meaning NOT taxed or regulated. The FIRST step in protecting PRIVATE property is to LEAVE IT ALONE. If government won’t do that, then there IS no government, but a mafia presiding in its place. See:

Challenging Jurisdiction Workbook, Form #09.082

https://sedm.org/Forms/09-Procs/ChalJurWorkbook.pdf

Everybody—including IRS & DOJ employees, as well as judges are bamboozled by the IRC! That’s its MAIN purpose, of course. That’s why it works so well. The subject of this section is also expanded in the following article:

PROOF OF FACTS: “U.S source” does NOT include anything but payments DIRECTLY from the government and excludes even payments from “taxpayers”, FTSIG

https://ftsig.org/proof-of-facts-u-s-source-does-not-include-anything-but-payments-directly-from-the-government-and-excludes-even-payments-from-taxpayers/

9. Burden of Proof When there is Doubt About the Meaning of “United States”

The U.S. Supreme Court has declared that when there is doubt about the meaning of a statutory term, the doubt MUST be resolve in favor of the party who is the target of obligations affected by the definition:

“In the interpretation of statutes levying taxes it is the established rule not to extend their provisions, by implication, beyond the clear import of the language used, or to enlarge their operations so as to embrace matters not specifically pointed out. In case of doubt they are construed most strongly against the Government, and in favor of the citizen. United States v. Wigglesworth, 2 Story, 369; American Net & Twine Co. v. Worthington, 141 U.S. 468, 474; Benziger v. United States, 192 U.S. 38, 55.”

[Gould v. Gould, 245 U.S. 151, 153 (1917);

SOURCE: https://scholar.google.com/scholar_case?case=10517878702666744364]

For more authorities like the above, see:

PROOF OF FACTS: Ambiguous tax statutes are to be construed against the government, FTSIG

https://ftsig.org/proof-of-facts-ambiguous-tax-statutes-are-to-be-construed-against-the-government/

10. Conclusions

As you read through the code, it’s stunning to see what lengths they go to to use United States in its geographical sense (domesticG) as much as possible, whereas domesticC is always implied through words like income, gains, profit, trade or business, wages, USRPI, ECTI, etc. That’s all domesticC (Federal nexus) stuff.

The voracious attempt to confuse the issue really underscores what it is they are trying to hide! They are hell bent on making the taxable activity appear to be income generation in the 50 States.

They’re doing the same thing that is prohibited in the License Tax Cases, but they found a word salad game they could play to make it legal all of the sudden. It’s all in the methodology!

We have prepared a detailed process you can use in any statutory or regulatory context for applying the the contents of this article to determine the meaning and context of “United States” below:

HOW TO: Techniques for discerning the context for statutory “United States” as either United StatesG (Geographical) or United StatesJ (Legal), FTSIG-12 tests you can apply to discern which context of “United States” is implied

https://ftsig.org/how-to-techniques-for-discerning-the-context-for-statutory-united-states/

You can also point your favorite AI at the above article and to the context you want to analyize to simplify the analysis.

11. Further reading

If you want proof that you can be within the GEOGRAPHICAL “United StatesG” WITHOUT being within the LEGAL/CORPORATE “United StatesJ“, see:

- HOW TO: Techniques for discerning the context for statutory “United States” as either United StatesG (Geographical) or United StatesJ (Legal), FTSIG-12 tests you can apply to discern which context of “United States” is implied

https://ftsig.org/how-to-techniques-for-discerning-the-context-for-statutory-united-states/ - Definitions: “United States”, FTSIG

https://ftsig.org/united-states/ - Definitions: “in the United States”, FTSIG

https://ftsig.org/in-the-united-states/ - Website Definitions, Section 32: “United States”, FTSIG

https://ftsig.org/advanced/definitions/#32._United - Copilot: History of definitions for the word “domestic” and “United States” in the Internal Revenue Code, FTSIG

https://ftsig.org/copilot-history-of-definitions-for-the-word-domestic-in-the-internal-revenue-code/ - Acquiring a Civil Status, FTSIG

https://ftsig.org/civil-political-jurisdiction/acquiring-a-civil-status/ - Proof That There Is a “Straw Man”, Form #05.042-those “in the United States” are public officers/agents

https://sedm.org/Forms/05-MemLaw/StrawMan.pdf - PROOFS:

8.1. PROOF OF FACTS: “individual” is a public officer fiction and “U.S. source” means GOVERNMENT source, FTSIG

https://ftsig.org/proof-of-facts-individual-is-a-public-officer-fiction-and-u-s-source-means-government-source/

8.2. PROOF OF FACTS: “INTERNAL” within “IRS” name means inside the government and “taxpayers” work for the Treasury, FTSIG

https://ftsig.org/proof-of-facts-internal-within-irs-name-means-inside-the-government-and-taxpayers-work-for-the-treasury/

8.3. PROOF OF FACTS: What the geographical “United States” means in 26 U.S.C. §7701(a)(9) and (a)(10), FTSIG

https://ftsig.org/proof-of-facts-what-the-geographical-united-states-means-in-26-u-s-c-7701a9-and-a10/ - Authorities on “includes”, Form #10.004, Cites by Topic, SEDM- the definition of GEOGRAPHICAL “United States” in 26 U.S.C. §7701(a)(9) and (a)(10) uses the word “includes”.

https://famguardian.org/TaxFreedom/CitesByTopic/includes.htm - Legal Deception, Propaganda, and Fraud, Form #05.014, Section 18.2: Abuse of “includes” and “including” in statutory definitions. -The definition of GEOGRAPHICAL “United States” in 26 U.S.C. §7701(a)(9) and (a)(10) uses the word “includes”

https://sedm.org/Forms/05-MemLaw/LegalDecPropFraud.pdf - META AI: Can a privilege not expressly authorized by statute be granted purely by judicial discretion if the judges pay derives from fees connected to paying for the delivery of the privilege?, FTSIG

https://ftsig.org/meta-ai-can-a-privilege-not-expressly-authorized-by-statute-be-granted-purely-by-judicial-discretion-if-the-judges-pay-derives-from-fees-connected-to-paying-for-the-delivery-of-the-privilege/